When logging in to perform a business transaction, consumers prefer modern authentication approaches. They often consider the username and password method and knowledge-based authentication (KBA) measures to be clunky.

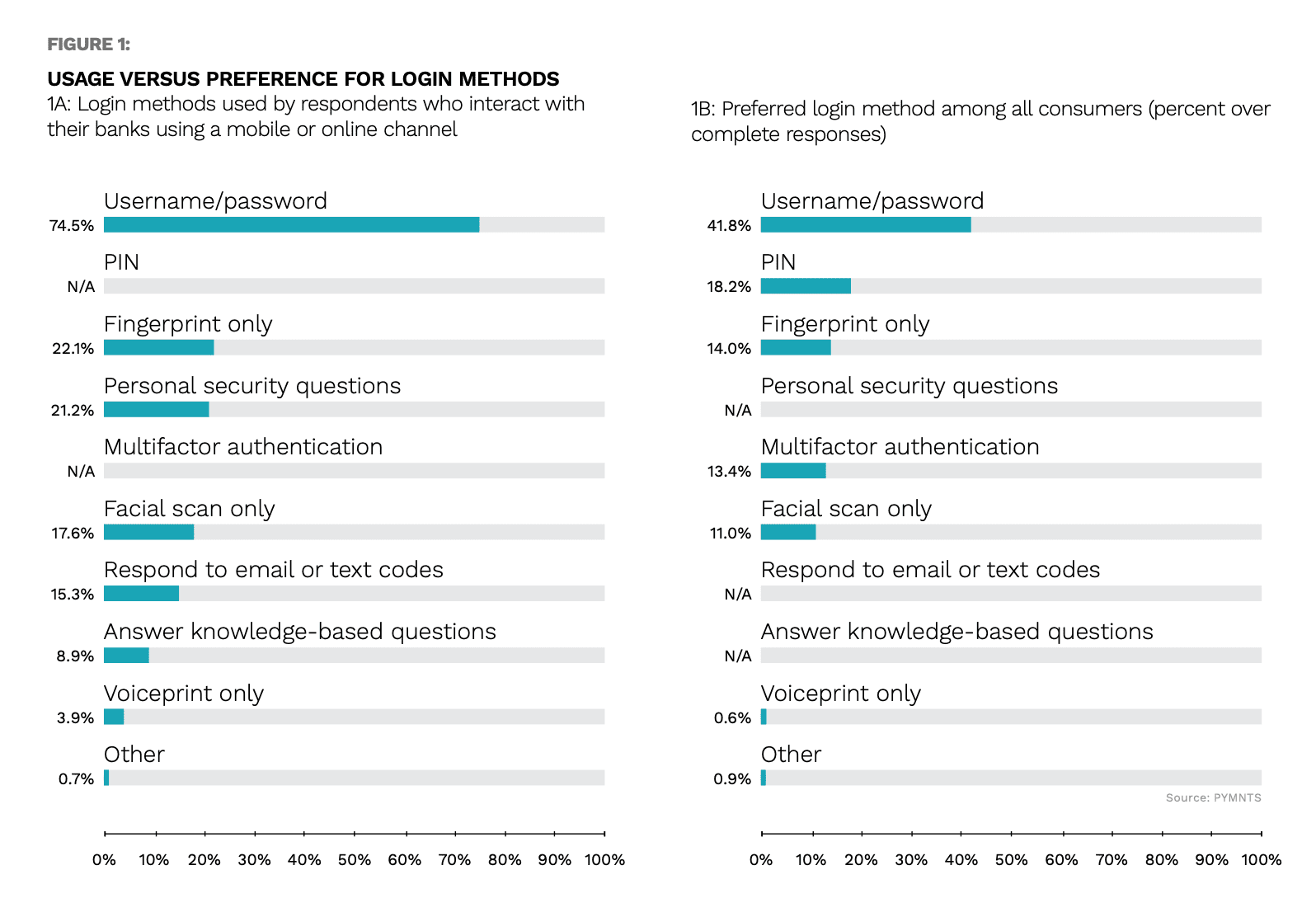

A new study, the Monetizing Digital Intent Tracker, a PYMNTS and Neuro-ID collaboration, found that usernames and passwords are used by nearly 75% of respondents who interact with their banks through an online or mobile platform, yet just 42% of customers labeled it as their preferred login method.

Get the study: Monetizing Digital Intent

KBA methods, while still preferred by some consumers, as losing favor as users adopt more seamless verification methods.

What’s more, methods such as KBA and passwords are not designed to confirm customers’ real identities, meaning questions surrounding their legitimacy may remain even after sign-up.

It is imperative for companies to appropriately mitigate identity theft and fraud risks as they differentiate between genuine customers and bad actors, but they cannot pursue these goals at the cost of seamlessness and convenience. Several emerging verification solutions can help businesses achieve these seemingly competing objectives, however.

For example, a behavioral analytics model not only reduces friction during the login process, but also better protects users from fraudsters. Stolen login credentials or account numbers are insufficient identifiers for a hacker to gain entry into a company’s personal data system because the technology immediately can recognize other peculiar behaviors and block access. Security professionals recommend the implementation of behavioral analytics into a business’s fraud defense system, especially as more traditional authentication methods grow increasingly unreliable.

Behavioral analytics operate seamlessly in the background during sign-up, allowing customers to analyze user behavior, such as how long it takes customers to fill out information and whether they make any mistakes supplying personal details. These insights, in turn, can provide clues about whether a prospective customer is legitimate or a bad actor in disguise.