After all, the FinTech-led buy now, pay later (BNPL) space hasn’t been exactly an overall money-printing endeavor. The popular consumer finance tool shot into the mainstream during the pandemic, when low interest rates allowed sector FinTechs maneuverability in both raising money and how it offered the payment method.

BNPL FinTechs struggled with profitability even before the Fed began raising rates. Now, they are in a near freefall, as evidenced in the “FinTech Tracker®,” a PYMNTS and Sezzle collaboration.

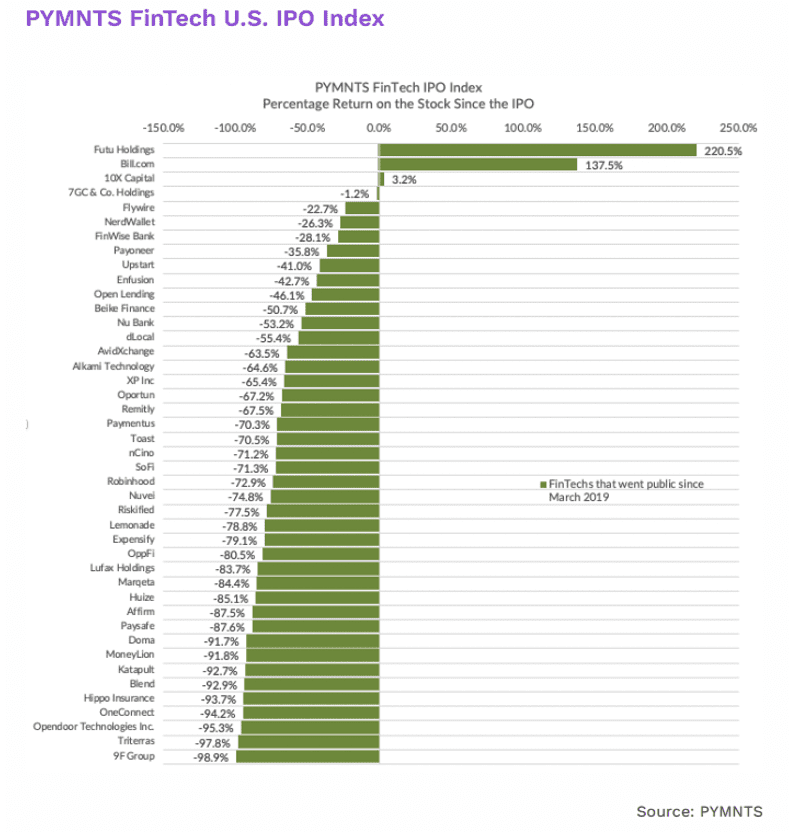

BNPL providers included in the PYMNTS FinTech U.S. IPO Index demonstrate the sector’s difficulties. For instance, MoneyLion’s stock return has sunk 92% since its initial public offering (IPO), and in an example of BNPL’s profitability challenges, popular provider Affirm is down 88%.

Across the sector, stock prices and valuations have dropped as lending and venture capital funds dry up due to tightened lending and increased regulatory scrutiny following Silicon Valley Bank’s collapse. Complicating matters is the current market oversaturation, as there are nearly 200 providers, per PYMNTS’ data.

All of these economic quirks of BNPL beg the question: Why would Apple enter the BNPL fray, especially now. So far, the tech behemoth’s steps into financial services have been limited to profitable, or at least safer, offerings. These efforts include the offering of savings accounts and its digital wallet, Apple Pay.

Apple’s Pay Later will be working a little differently than its other consumer-facing financial tools. Subject to eligibility and approval, the installment plan will be built into Apple Wallet. The payment method is limited to select users before an expanded rollout in the coming months, and users will be able to split purchases into four interest- and fee-free payments spread over six weeks.

Apple’s loans will range from $50 to $1,000 and can be used for online or in-app purchases through an iPhone or iPad, with the ability to track, manage and repay within Apple Wallet. Loans will be reported to credit bureaus and become part of user’s financial profiles.

Without official word from Apple, answers to “why now” are still in the air. One possibility is that the company may not be facing the same economic challenges pure play BNPL FinTechs face. With Apple’s dedicated and loyal customer base and many merchants already accepting its wallet, the tech giant has no need to spend on customer acquisition or further retailer integration.

Given this significant difference than pure play competitors, Apple could have better unit economics. After all, it only needs to ensure that more people pay back these loans than don’t, which may be one clue as to why the company is keeping Pay Later invite-only for now.

Additionally, if Apple’s overall strategy is to keep their users in-house through a variety of offerings, then the goodwill and brand affinity generated by Pay Later may turn out to be more lucrative than strict dollars and cents.