Personal savings serve key purposes, chief among them as a financial safety net. But runaway inflation has started to eat away at consumers’ cash reserves, which spiked when government stimulus was abundant — and are now getting more and more difficult to replenish.

As credit tightens against the recessionary conditions expected in the second half of 2022, consumers will be on the hunt for lending products that help close the savings gap.

The Commerce Department gave a sense of the situation in its June 30 report detailing May consumer income and outlays, finding that personal expenditures rose 0.2% but in fact fell 0.4% adjusted for inflation, much as the 0.5% income rise seen in May was weakened to 0.1%.

PYMNTS data confirms the drain on savings, with the added finding that more consumers are spending more than they earn, making the rebuilding of savings cushions next to impossible.

According to “New Reality Check: The Paycheck-To-Paycheck Report — Financial Distress Factors Edition,” a PYMNTS and LendingClub collaboration surveying of more than 2,300 consumers, “19% of consumers living paycheck to paycheck have spent more than what they have made in the last six months, compared to 2.2% among consumers not living paycheck to paycheck.”

Unpacking the report leads to the eye-popping revelation that of consumers earning more $250,000 a year, “7% have spent more than what they have made in the last six months.”

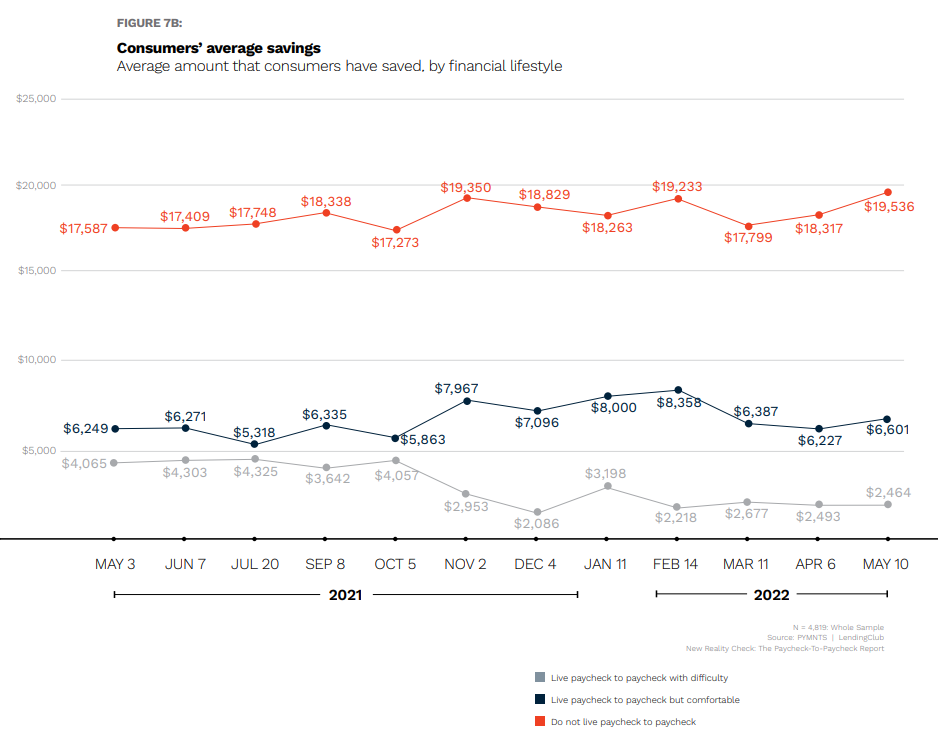

Over the course of the New Reality Check Paycheck-To-Paycheck study series, we’ve observed the average savings rate remain “relatively stable in a year-over year comparison, though it did rise to $11,274 in May 2022 from a low of $9,557 in March 2022,” per the new edition.

The line of demarcation is between those living paycheck to paycheck but comfortably meeting expenses, and those who can’t, with savings a prime indicator. For example, the Financial Stressors Edition found that savings among consumers not living paycheck to paycheck “has increased to a high of $19,536 — 11%, or almost $2,000, above the May 2021 mark.”

By comparison, those living paycheck to paycheck and struggling to meet monthly bills “have seen their average savings cut nearly in half, down from $4,065 in May 2021 to $2,464 in May 2022.”

Get Your Copy: New Reality Check: The Paycheck-To-Paycheck Report – The Financial Distress Factors Edition

Decision Time

Speaking on the latest study in the series, LendingClub financial health officer Anuj Nayar told PYMNTS, “In the same way that when the interest rates were low you refinanced your debt, mortgages or car loans, whatever else, to move your costs of borrowing down, now’s the time, if you’ve got any savings, to refinance your savings.”

The danger now is consumers with little or no savings running up and revolving costly credit card balances to make ends meet, when other financial products — namely personal loans — have kinder interest rates that are make the financial high-wire act less costly.

Nayar said, “You should be thinking about how to manage that at the beginning of the process versus what most people do, which is ‘I’ve got to spend the money, I’m going to put it on a credit card. I’ll deal with it later.’ Then you’re stuck in a hamster wheel of trying to pay that off.”

He added that “This is the time to be thinking … how do I move before other rates change? How do I move from a very high interest credit card to something that’s a little more secure and fixed, like a personal loan?”

See also: Unexpected Expenses Could Hobble Inflation-Weary Paycheck-to-Paycheck Consumers