This competitive edge has disappeared in recent months, however. COVID-19 has forced many CUs to limit their brick-and-mortar hours of operation or close their branches completely, leaving CU members to rely primarily — and sometimes exclusively — on their CUs’ digital banking options.

This competitive edge has disappeared in recent months, however. COVID-19 has forced many CUs to limit their brick-and-mortar hours of operation or close their branches completely, leaving CU members to rely primarily — and sometimes exclusively — on their CUs’ digital banking options.

So, how can credit unions work to stand out from their competitors when every bank is digital-first?

This is just one of the key questions PYMNTS sought to answer in the Credit Union Innovation Playbook: Challenger Banks Edition, in collaboration with PSCU. We surveyed more than 4,000 CU members, CU leaders and FinTech executives about why they believe challenger banks may have an upper hand when it comes to digital banking innovation and why it might  help them gain a competitive edge over credit unions and FinTechs.

help them gain a competitive edge over credit unions and FinTechs.

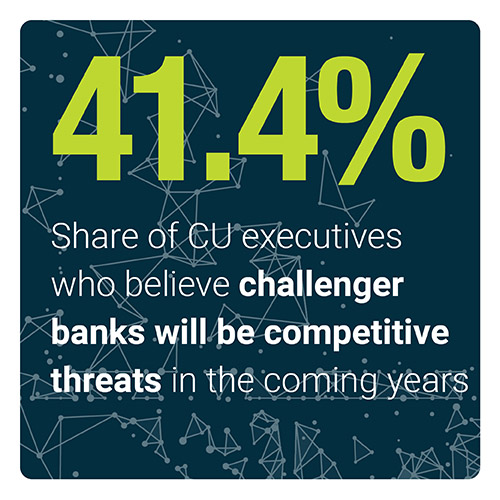

Our findings show that many CU executives are concerned that their members might feel tempted to switch to challenger banks — and their fears are not unfounded. Three out of 10 CU members say they would be interested in banking with PayPal, and two out of 10 would be interested in using banking services offered by large technology firms.

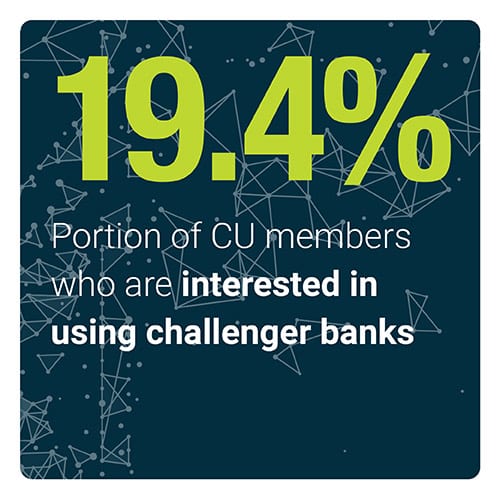

The primary draw of challenger banks like these is that many consumers believe they would be able to offer easier-to-use, more convenient services than CUs, with 35.9 percent of CU members saying as much. Thirty-two percent are also intrigued by challenger banks’ online services, and 28.9 percent say they believe challenger banks’ mobile apps would be of higher quality. This wide assortment of digital services places added pressure on CUs to enhance their own digit al banking capabilities — especially now that they have become central to their mid-pandemic member outreach efforts.

al banking capabilities — especially now that they have become central to their mid-pandemic member outreach efforts.

The Playbook details how they can tailor their innovation plans to help maximize consumers’ digital banking access and stand out from up-and-coming challenger banks and FinTechs.

To learn more about how CUs can use innovation to differentiate themselves in an all-digital-first banking environment, download the report.

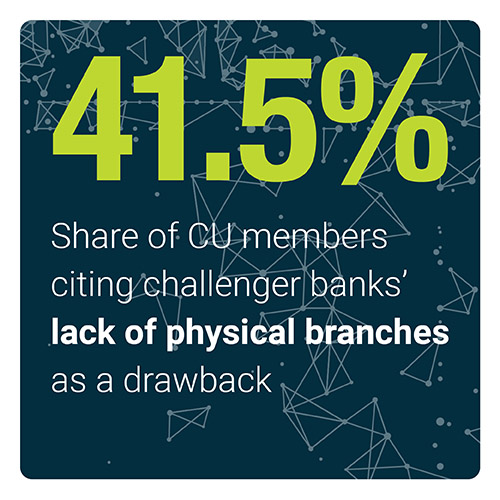

Brick-and-mortar presence used to give credit unions (CUs) a competitive edge over digital-only challenger banks. PYMNTS research shows that 41.5 percent of CU members believe that being unable to visit branch locations represents one way in which using challenger banks would make their banking experiences worse.

Brick-and-mortar presence used to give credit unions (CUs) a competitive edge over digital-only challenger banks. PYMNTS research shows that 41.5 percent of CU members believe that being unable to visit branch locations represents one way in which using challenger banks would make their banking experiences worse.