Lawmakers and regulators say we can expect a set of guide rails for the stablecoin business by year’s end. Here’s a look at the issues and the major pieces of legislation driving the discussion.

There are a couple of major policy points that define the U.S. stablecoin debate.

Some are controversial: There’s a rough and tumble fight coming over whether stablecoins should be issued only by federally insured banks, as the President’s Working Group on Financial Markets recommended — to more than a little opposition from members of Congress, many (but not all) of whom wanted state regulators to be able to charter stablecoin issuers.

See also: Powell, Yellen Clash Over Stablecoin Regulation at Senate Hearing

Treasury Secretary Janet Yellen and Fed Chairman Jerome Powell even disagreed on this part.

Some are less controversial. Especially after the $48 billion collapse of the Terra/LUNA algorithmic stablecoin in May and subsequent wave of bankruptcies affecting crypto lenders with hundreds of thousands of investors’ funds frozen and at risk, there is pretty universal agreement among lawmakers and regulators, as well as a fair chunk of the crypto community, that all stablecoins should be backed one-to-one by dollars or highly liquid assets like U.S. Treasurys. That’s outside of decentralized finance (DeFi), where algorithmic stablecoins are still flourishing.

The only major disagreement on that point by legislators and regulators is where those reserves should be held: state or federal institutions, or even the Fed directly.

A major entrant into the debate will come next month when various government agencies working under a presidential executive order make their own proposals known.

Banks Don’t Like Them

The banking industry wants stablecoins to be issued by fully regulated institutions, at the very least and has a number of problems with them generally. The American Bankers Association (ABA) told the Senate Banking Committee late last year that “stablecoins, unlike other financial instruments, are not subject to a consistent, comprehensive set of regulatory standards that mitigate the risks they pose to consumers and the financial system. The lack of regulation is particularly concerning as the rapidly evolving uses of stablecoins is fueling significant market growth.”

It also took exception to the argument that stablecoins would facilitate real-time payments, noting that those are already “fast becoming a reality” in the regulated banking system. It added that stablecoins “are designed to circumvent this established regulatory architecture” and pose a number of risks, notably runs — which is what happened to the TerraUSD stablecoin in May.

Comptroller of the Currency Michael Hsu had made similar comments before the Terra/LUNA collapse, and both were quick to point that out.

One big problem banks have is that stablecoin reserves kept in their institutions would likely have to be maintained 100%, rather than loaned out with fractional reserves.

Where It Began

It’s worth remembering that whenever stablecoin regulation is discussed, it started with Meta’s 2019 project to create the Libra (later Diem) stablecoin that would be instantly usable by Facebook’s 2.3 billion customers, including across national borders — which central bankers feared would damage their ability to influence the economy and fight crises, and possibly cause fiat to be bypassed altogether in some jurisdictions with weak currencies.

That was beaten into collapse by regulators and elected officials in the U.S. and abroad, but distrust of Facebook was a big part of that fight.

But a more basic argument, whether stablecoins are a threat to national currencies or a tool of financial innovation that the U.S. can’t afford fall behind on, fuels much of the current controversy.

That concern is behind much of the push to create central bank digital currencies (CBDCs) like a theoretical digital dollar and digital euro, and the nearly live digital yuan. How big a concern is it? More than 100 countries are at some point in investigating, piloting or building CBDCs — something that wasn’t really an issue before then-Facebook launched Libra.

Current Proposals

Here is a look at some of the more prominent legislation Congress is considering now.

It’s worth noting that a major one is likely coming from House Financial Services Committee leaders before the end of the year.

See more: Report: House Stablecoin Bill Put on Hold

Chairwoman Maxine Waters, D-Calif., and the top Republican on the committee, Rep. Patrick McHenry, R-N.C., were trying to get a bill agreed upon before Congress left for the summer but couldn’t get the details down. But given the urgency put behind stablecoin regulation since the TerraUSD collapse, a version of that bill will likely be seen before the end of the year.

Key elements: This is a “discussion draft:” not a final proposal.

Key elements: This is a “discussion draft:” not a final proposal.

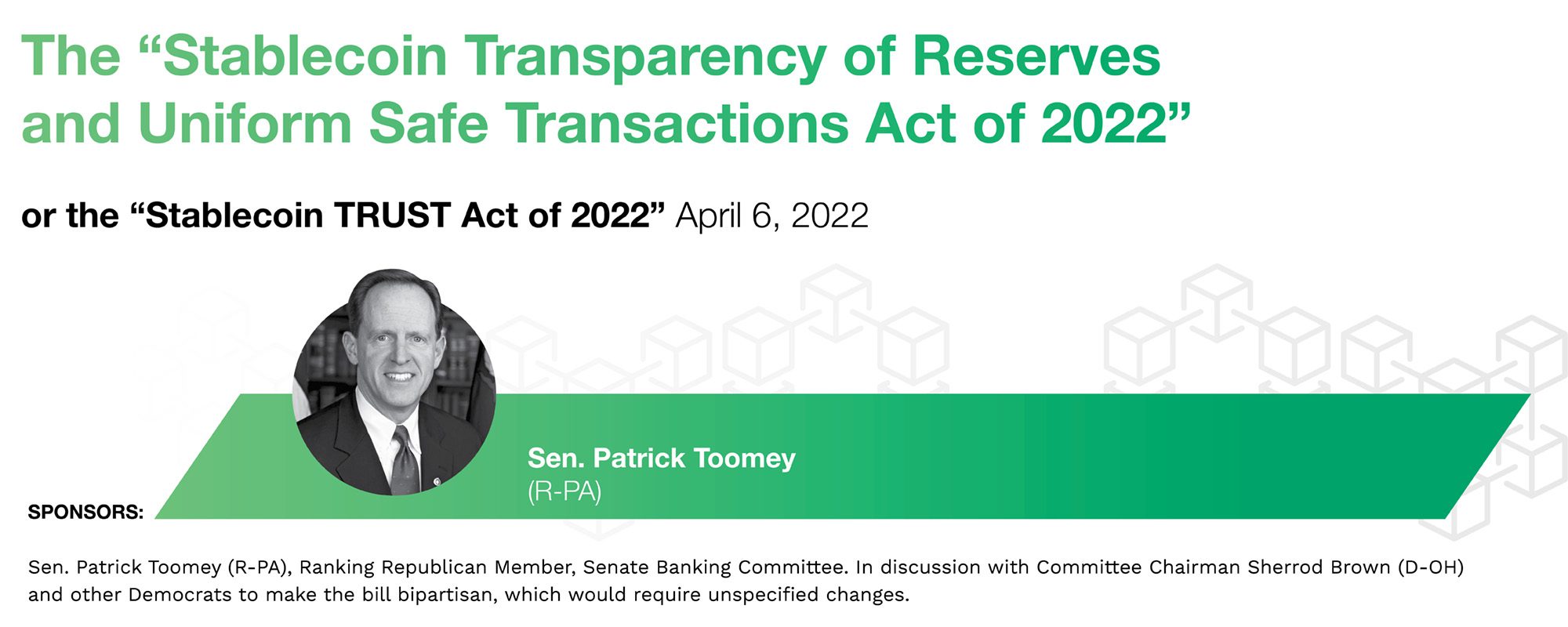

- “The Securities Act of 1933 … is amended by adding at the end the following: ‘‘The term ‘security’ does not include a payment stablecoin, as that term is defined in section 2 of the Stablecoin TRUST Act of 2022.”

- A “payments stablecoin can be issued by a state-chartered money transmitting business; national limited payment stablecoin issuer (licensed by the Comptroller of the Currency); insured depository institution.

- Requires disclosure of assets backing stablecoin on a monthly basis, audited quarterly by a registered accounting firm, filed with the Treasury secretary and made public.

- Backed 100% by cash, cash equivalents, level 1 high quality liquid assets denominated in U.S. dollars.

- The Treasury Department may not collect user information without a warrant.

Key elements:

Key elements:

- Defines stablecoins as backed 1-to-1 by U.S. dollars or government-issued securities like Treasurys.

- Defines a “qualified stablecoin” as neither a security nor a derivative.

- Backing reserve cash must be held in a segregated FDIC-insured account.

- Issuers must be either a bank or a non-bank qualified stablecoin issuer.

- The Federal Deposit Insurance Corporation (FDIC) will be “required to develop a Qualified Stablecoin Insurance Fund to manage the insurance of redemption payments of non-bank issuers.”

- Gives OCC primary oversight.

- Does not restrict the issuance of other types of stablecoins (like algorithmic stablecoins) but they may be securities or derivatives.

Who supports: Digital Chamber of Commerce, USD Coin stablecoin issuer Circle, Blockchain Association and many other crypto companies.

“Rep. Gottheimer’s bill represents the most comprehensive and well-thought-out stablecoin legislation we’ve seen to date,” said Kristin Smith, executive director of the Blockchain Association.

Key elements: A total cryptocurrency regulatory bill, stablecoins are just one part of the bill.

- Must be backed by 100% reserves of dollars or high-quality liquid assets like Treasurys.

- Public disclosure of the makeup of the reserves.

- Ability to redeem all issued stablecoins at par on demand.

- The OCC will be able to charter national stablecoin issuers and establish a charter process for state banking institutions.

- A rule would seek to ensure that “existing stablecoin issuers and new entrants into the market have an adequate opportunity to compete with existing banks and credit unions for the issuance of payment stablecoins.”

- Create a FInCEN Innovation Lab for stablecoin development.

Who supports: Digital Chamber of Commerce, Association for Digital Asset Markets, Blockchain Association, Crypto Council for Innovation, and many crypto firms including Coinbase and FTX exchanges.

“The Responsible Innovation Act is a foundational, comprehensive start to setting a national regulatory framework for digital assets and addresses inter-agency cooperation, regulatory oversight and the consumer protections necessary for these types of innovative products and services,” said Perianne Boring, founder and CEO of the Chamber of Digital Commerce.

For all PYMNTS crypto coverage, subscribe to the daily Crypto Newsletter.