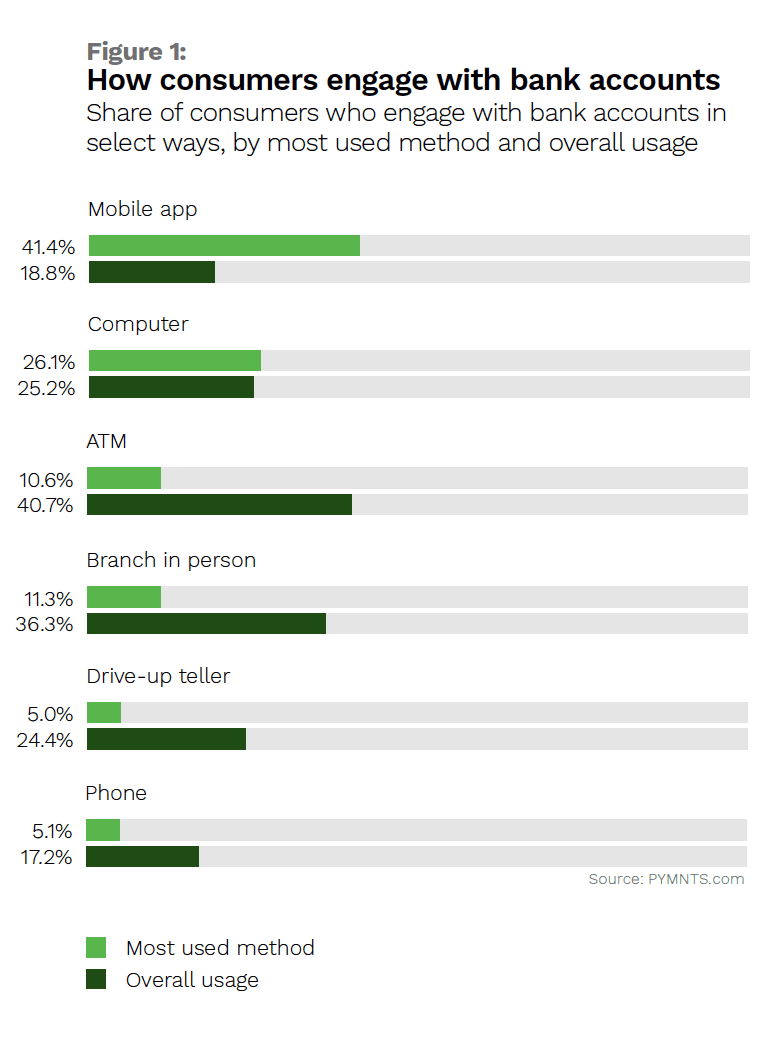

As the result of the pandemic, more and more banking customers worldwide rely on mobile and online banking solutions: 41% of consumers report that they bank primarily via mobile app, in fact, and 26% now say they prefer to use their computers. Aside from these trends, there is another tool playing a significant role in banking’s digital transformation: the ATM.

Nearly 11% of banking customers use ATMs as their primary banking channel, and approximately 41% identify ATMs as a routine way they access banking services. ATMs are also preferred more than drive-up tellers, which just 5% of consumers identify as their primary banking channel. The global ATM market’s expansion is a testament to the technology’s enduring popularity. It reached $20.18 billion in 2020, and its 4.9% compound annual growth rate (CAGR) is expected to continue through 2028.

This month’s Deep Dive examines the continuing appeal of ATMs and how technological advancements are creating cutting-edge solutions such as interactive teller machines (ITMs). It also analyzes how ATM-as-a-service (ATMaaS) offerings can help financial institutions (FIs) better scale their operations by shifting maintenance and management to third-party operators.

Bridging Branches and Digital Banking

Consumers’ growing preference for digital banking solutions does not eliminate the nee d for robust ATM availability, and ATMs provide a physical touch point that can help FIs bridge consumers’ physical and digital banking needs. This has been crucial during the pandemic as consumers have sought ways to transact conveniently and safely, and ATMs in many markets now offer more personalized, flexible experiences because of this shift. Users can now pay bills, make money transfers and even engage with tellers via ATMs, for example, illustrating how far the technology has evolved beyond facilitating simple withdrawals and deposits.

d for robust ATM availability, and ATMs provide a physical touch point that can help FIs bridge consumers’ physical and digital banking needs. This has been crucial during the pandemic as consumers have sought ways to transact conveniently and safely, and ATMs in many markets now offer more personalized, flexible experiences because of this shift. Users can now pay bills, make money transfers and even engage with tellers via ATMs, for example, illustrating how far the technology has evolved beyond facilitating simple withdrawals and deposits.

Research also suggests that the technology can help consumers use services more effectively when they decide to visit branches. More than 26% of consumers cited the ability to visit a physical bank branch as the most important retail bank benefit, but the services they seek when doing so are becoming more specific. Rather than visiting a branch for everyday banking services, consumers now expect to use them more for advice or consultation. Investing in cutting-edge ATMs that allow consumers to tackle various banking tasks can enable physical branches to be smaller, nimbler and more selective about the services they offer.

Advanced technologies also play an important role in ensuring customers have access to needed services when interacting with ATMs. Consumers across all demographics said they would use video ATMs if they were available at their bank branches, and the technology was ranked ninth among investment priorities for financial services leaders. ITMs can provide a wide range of services that aren’t possible through digital-only solutions, such as money orders or video consultations with financial assistants.

One-quarter of FIs have ITMs in place, and an additional 60% are planning ITM deployments within three years. This trend has been driven in part by banks’ need to deliver positive customer experiences, even as pandemic restrictions force them to close or modify their operations. Consumers are also interested in ITMs’ capabilities, with 68% using them for deposits and withdrawals, 40% making credit card payments, 26% opening new credit accounts and 21% paying bills.

ATMaaS Provides the Latest Technology With Manageable Costs

There is at least one major consideration for FIs aiming to bolster their ATM fleets with ITMs and other machines leveraging advanced technologies: cost. The upfront cost of purchasing an ATM with basic functionality may be a few thousand dollars, but more advanced machines can run into the tens of thousands.

Other recurring costs stem from cash management and software updates to regular maintenance, but ATMaaS solutions can offer a fix for many of these cost concerns. These services can help FIs handle the myriad costs associated with managing ATM fleets by offering comprehensive solutions for a single monthly fee.

They enable FIs to upgrade to the latest technology using subscription-based pricing without significant upfront capital investment, helping them consolidate costs and reduce the overall ownership expense. ATMaaS also helps FIs craft more consistent user experiences, impacting brand perception and loyalty. These solutions allow users to deliver new features, such as biometric authentication capabilities and eWallet access to an entire fleet.

Consumers are returning to their bank branches more frequently as pandemic-related concerns ease, but what they expect from branch-based interactions has fundamentally shifted. A growing number of consumers are looking to accomplish more of their financial tasks using ATMs and ITMs and are reserving visits with financial professionals for when they seek advice or consultations. In this climate, FIs that offer advanced ATM fleets equipped with the latest technologies and services more readily can serve the needs of their digital-first customers.