There’s data and then there’s the story the data can tell — and sometimes the story you get is not the whole story.

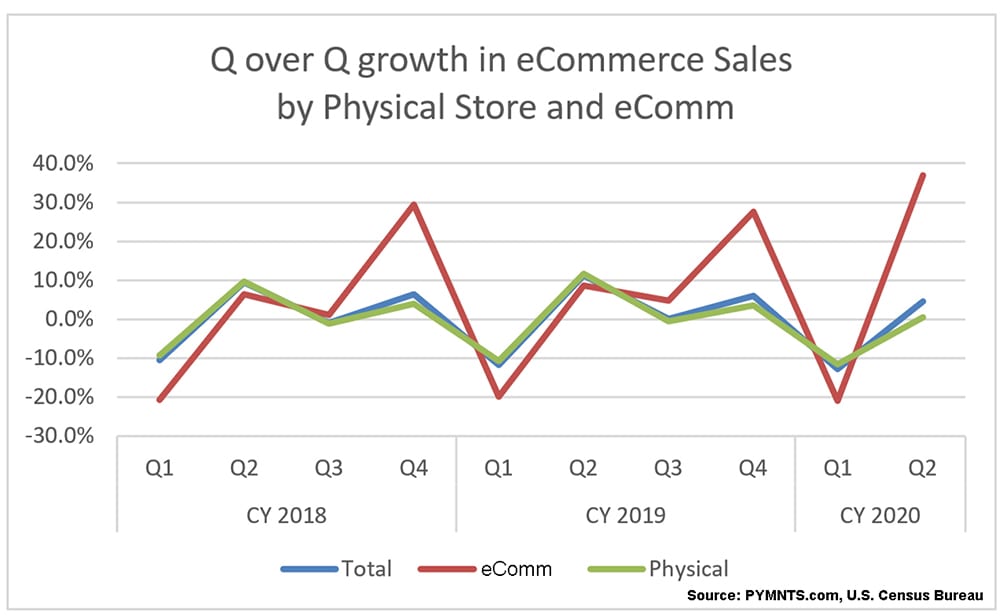

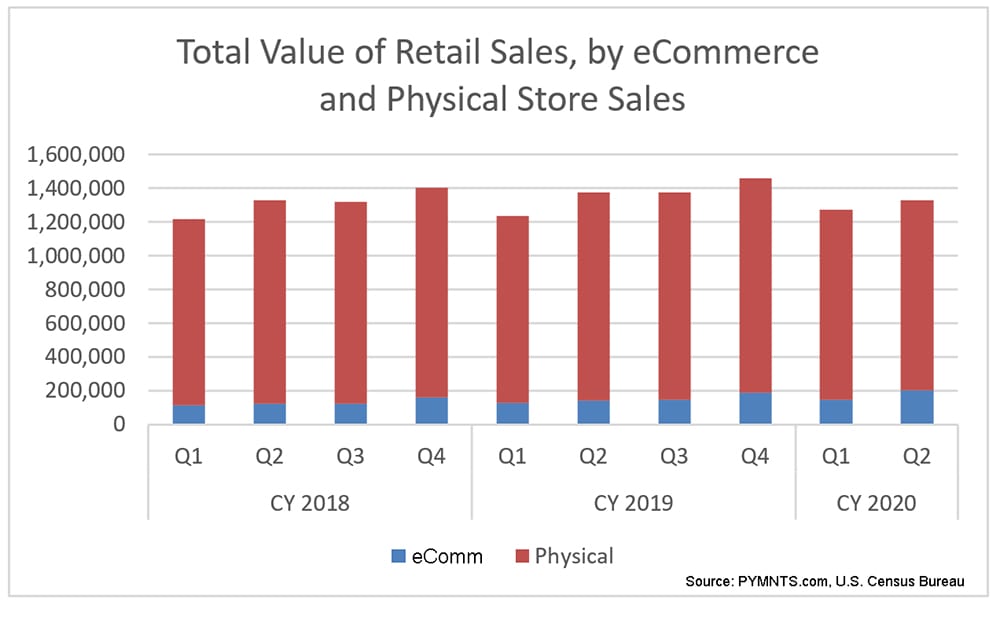

To that end, on Tuesday (Aug. 18th), the Department of Commerce’s U.S. Census Bureau reported that retail eCommerce sales for the second quarter, on an unadjusted basis, stood at $200.7 billion, up 37 percent sequentially, from the first quarter of the year.

That jump comes at total retail sales were $1.3 trillion, down 3.4 percent year on year.

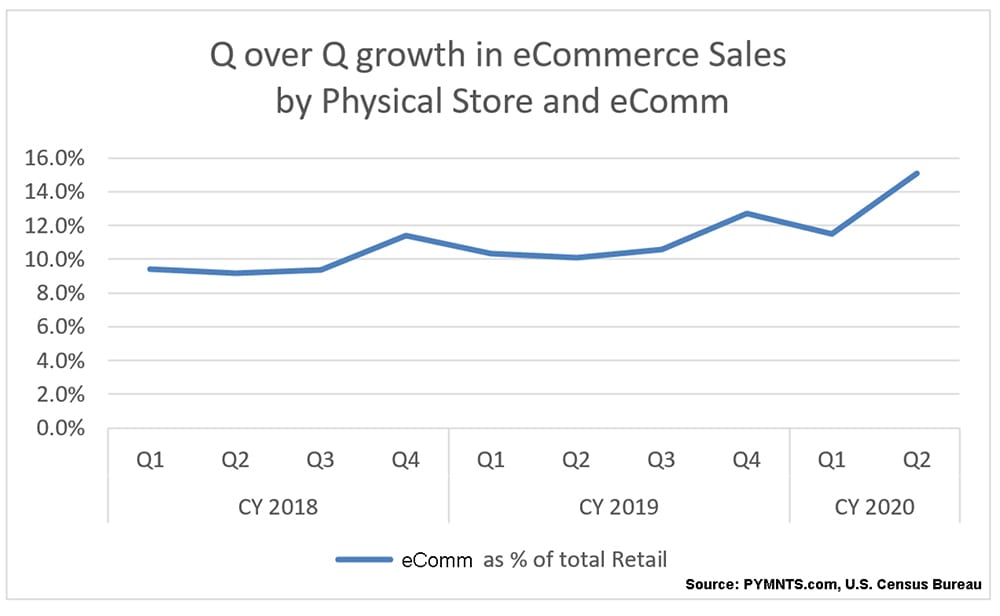

Online sales, then, stood at 15.1 percent of the total tally, and the overall decrease (in aggregated sales) comes as, of course, the lingering impacts of lockdown and staggered re-openings continued.

As measured year on year, eCommerce sales were up 44.4 percent, even as total US retail sales slipped 3.4 percent.

No matter how you slice it, then, eCommerce is booming. But we note that the boom might be even more seismic than the official data might show.

No matter how you slice it, then, eCommerce is booming. But we note that the boom might be even more seismic than the official data might show.

Consider the fact that in a discussion of the quarterly eCommerce data is collected, the Census Bureau notes that the numbers include “estimates for companies classified by the North American Industry Classification System (NAICS) as Nonstore Retailers (NAICS 454) and a subset of those companies in NAICS 4541 called Electronic Shopping and Mail-Order Houses. However, other retailers that may not be conducting eCommerce, including electronic auctions and mail-order houses, are also included in these estimates.”

Parsing that language: Non-store retailers may omit a significant number of companies that are logging a significant number of electronic transactions, across a variety of payment methods.

As defined in Census literature, non-store retailers are firms that “serve the general public, but their retailing methods are different than those employed by store retailers. These establishments reach customers and market merchandise through things like paper and electronic catalogs, door-to-door solicitation, in-home demonstration, infomercials, portable stalls and vending machines.”

That leaves out the plethora of storefronts, real ones (many with a growing virtual presence) that take payments online, yes, but also log digital transactions as they take orders in-store pickup or curbside delivery. These are the companies that take contactless cards or QR payments at the register — certainly they are digital sales too, even as consumers also check out on web pages.

Recent results from card network giants underscore the surge in card not present (and thus electronic commerce) transactions. Visa noted on its second-quarter earnings call that credentials active in eCommerce — excluding travel — were 12 percent higher in June than in January. The total spend per active credential was up over 6 percent. And buying online begets buying online.

Recent results from card network giants underscore the surge in card not present (and thus electronic commerce) transactions. Visa noted on its second-quarter earnings call that credentials active in eCommerce — excluding travel — were 12 percent higher in June than in January. The total spend per active credential was up over 6 percent. And buying online begets buying online.

As CEO Al Kelly noted on the call: “In fact, when you isolate the active credentials who tend to be more significantly engaged in e-commerce, the spend per active credential increased by over 25 percent.” And as for in-store transactions, contactless payments, including QR codes and digital wallets, have been on the rise.

Mastercard, for its part, in the second quarter, contactless penetration represented 37 percent of in-person purchase transactions up from 28 percent a year ago.

All of this translates into a shift not just toward digital transactions — but changes in how those digital transactions are done, and even where — which may hint that the official, government data gets the trend right, but perhaps at a muted pace.

Recent PYMNTS research shows that QR codes are gaining traction within touchless commerce — in restaurants, for example, Apple Pay (which just enabled that functionality) in Walgreens, and at Walmart.

Walmart, incidentally, offers a good snapshot of eCommerce growth. Headline numbers show that eCommerce sales were up 97 percent year on year (accelerating from 1Q’s 75 percent year on year boost).

It remains to be seen whether consumer behavior moves back into in-store mindsets when re-openings become a bit more entrenched.

But it seems the move toward in-person transactions will be as, well, distanced as possible, which implies QR codes, digital wallets and contactless cards, and not credit cards at the register, will be (payment) instruments of choice.