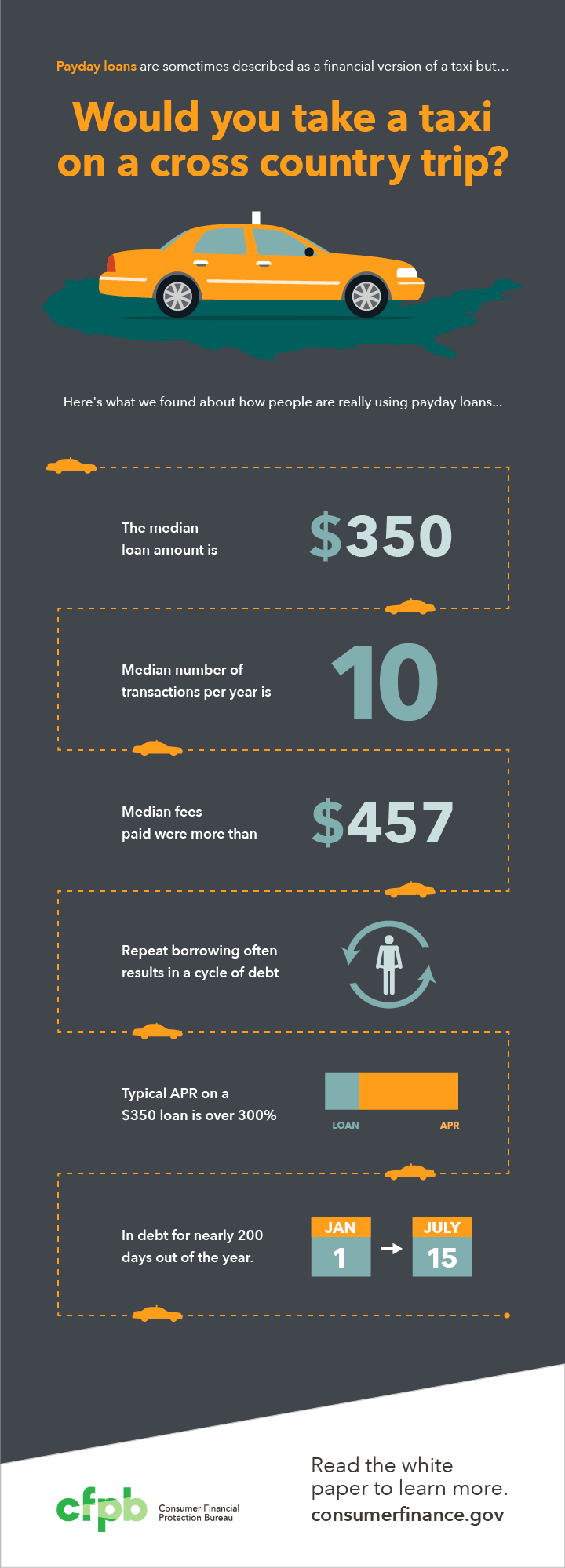

Did you know that the average payday loan borrower spends 196 days of the year indebted?

Yes, that’s a whopping 54 percent spent caught in what can be a vicious cycle of borrowing and repayment, and its one of the more telling stats brought forwards by the Consumer Financial Protection Bureau’s recent white paper: “Payday Loans and Deposit Advance Products.”

The results of the study seem to confirm what many have long held true: payday lending is ok in moderation, but has dangerous implications for those who use the services with frequency.

“It appears that these products may work for some consumers for whom an expense needs to be deferred for a short period of time,” the CFPB wrote in their conclusion.

“However, these products may become harmful for consumers when they are used to make up for chronic cash flow shortages.”

The numbers the CFPB now has to back up that statement are compelling: consider, for example, that the average borrower paid $574 in fees alone during the 12-month period over which the study was held.

We break down more of the CFPB’s findings – plus take a look at an infographic — in this PYMNTS.com Data Point.

Average Payday Loan Stats

According to the CFPB, the mean for payday loan amount came in at $392, while the median sat at $350. The mean fee per $100 was $14.40 percent, with a media total of $15. Payday loan recipients generally took 18.3 days to repay their loans, while the median total was 14 days. Finally, the APR for payday loans came in at a mean of 339 percent and a median of 322 percent.

Income Distribution: Borrower Economics

The CFPB also broke down payday borrowers by their income, annualized and as reported at the time of borrowing. Thirty-one percent of borrowers made between $10,000-20,000 per year: the highest percentage in the report. A quarter made between $20,000-$30,000, while 12 percent made less than $10,000. Sixteen percent reported income between $30-40,000, while eight percent reported income between $40,000-50,000. Surprisingly 4 percent each indicated they made between $50-60,000 or $60,000-plus during a year. The mean borrower income sat at $26,167, while the median reported was $22,476.

The report also breaks down the source of reported income at application, with employment taking a hefty share of responses at 75 percent. Eighteen percent indicated their income comes form public assistance or benefits, while 4 percent cited retirement funds and 3 percent cited “other.”

Loan Usage: How Often Do Users Borrow?

The CFPB notes that nearly half (48 percent) of all borrowers had more than 10 payday loan transactions during the 12-month study, with 29 percent conducting over 20 transactions. Just 13 percent of borrowers completed only one or two transactions, and 20 percent cited three-to-six transactions during the year. The median consumer in the CFPB’s sample conducted 10 transactions over the 12-month period, paying a total of $458 in fees, excluding the loan principal.

To see more of the CFPB’s statics on payday lending, read the full report here. You can also scan the CFPB’s infographic below for a quicker look.