Michael Porter’s Five Forces And Payments Innovation

I feel like I’m back in school.

In preparing for The Innovation Project’s lead off session with Professor Michael Porter, the father of competitive strategy, and 10 CEOs from across the established and emerging payments/commerce ecosystem, I decided to do a “five forces” framework analysis for payments. Wait, this isn’t how most of you spend your nights and weekends?

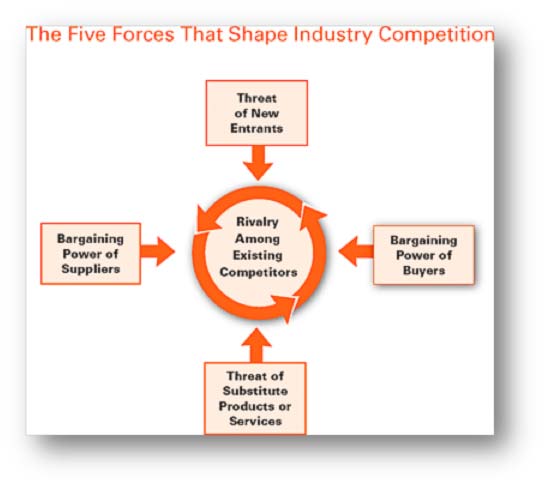

For those of you who might have cleared the five forces stuff from your brain’s memory bank to make room for other stuff, it’s a strategic framework that Porter first published inHarvard Business Review in 1979. It establishes a consistent way to look at an industry to determine its profit potential. Porter’s punch line is that there are forces, five of them, in any given industry that drive profit and, therefore, influence its competitive landscape.

Those forces relate to the chokehold that buyers and suppliers have on an industry, the threat of new entrants, the availability of substitutes and the intensity of competitors whose actions to capture and preserve market share can diminish profitability. Each of these factors is evaluated to determine the degree to which it increases or decreases competition. When taken together, these five forces help strategists determine whether they have a shot at producing profits.

Porter’s 1979 article became a book, Competitive Strategy, a year later. Since then, it’s been reprinted 60 times and in 19 languages. As of 2008, it was estimated that more than 1 million people have internalized and applied this framework to matters of strategy across dozens and dozens and dozens of industries.

Here’s the Cliff Notes version of the five forces framework as taken from one of Porter’s recent articles on the topic.

Supplier power is determined by the number of suppliers, the uniqueness of their products and the degree to which they have control over a proprietary technology or capability which might make switching away from that supplier difficult or expensive. The fewer the number of suppliers and the more they are needed to produce a product, the more powerful each supplier is.

Buyer power is driven by the number of buyers, the importance of any one individual buyer to the industry, and the ease with which they could switch to a competing supplier. Fewer buyers means more control over suppliers and the makings of a powerful force that can, ultimately, drive prices and profits down.

Threat of substitutes is the ease in which buyers or suppliers can find a different way of doing or getting what they currently do or get from a buyer or a supplier. If it’s easy, then existing players can wave bye-bye to higher prices and profits.

Threat of new entrants is about how easy it is for a new player to enter the market and provide services. If it isn’t difficult it’s cheap, the regulatory hurdles are low, proprietary technologies aren’t required to produce a product or deliver a service, and economies of scale don’t matter. Then it’s relatively easy for new players to enter and compete away potential profits.

Competitive rivalry is about the number and capabilities of competitors. If there are tons, and they all offer more or less the same services and capabilities, the power then accrues to the buyers and suppliers who can pick and choose from a variety of alternatives. Competitors respond by reducing prices, which can spell death to profits. The opposite effect is also true if a particular player has a unique capability that’s difficult to replicate.

So, an industry is attractive from a profit perspective if most of the power is concentrated in a few strong suppliers, there aren’t many available substitutes, and it’s difficult and expensive for new players to enter.

How this applies to payments

Yeah, easier said than done. Let’s take a look at how this framework can be applied to payments.

Right off the bat, I’ll say that it’s a bit tricky. Payments is an intensely complicated ecosystem, made even more so now given the degree to which new ecosystems are influencing the direction of payments, such as mobile and online, etc. It’s hard to isolate and label players as suppliers and buyers since payments is a platform ecosystem with multiple and interdependent stakeholders who rely upon sets of rails to enable payment and commerce services.

But as I began to play around with it, I discovered that it turned out to be very helpful in illustrating a few fundamentals about strategy and competition.

See what you think.

Before the formation of Diners Club in the 1950s, the payments industry was pretty straightforward. Consumers had more or less two options to pay for things at the physical store: cash and checks. In this pretty simple world, the supplier of the rails for these payment instruments was, for all intents and purposes, the government. It operated the cash and check systems. The buyers, if you will, were the banks that operated as the conduit between the supplier of the payments rails, the consumers who used instruments that rode on those rails and the merchants who accepted these instruments.

Of course, there were also merchants that supplied credit to their customers via revolving credit accounts or store accounts that were settled in full at the end of every month. But store accounts weren’t interoperable – they couldn’t be used at other stores, so there was no impact on the competitive environment in any real sense.

Since there weren’t any substitutes for cash or check, there was no competitive pressure on the part of the banks to do anything to differentiate their product or compete for business. In fact, differentiation among check and cash products was not even a competitive consideration. Of course back in the day, banks gave away toasters and even TVs to people to get them to open accounts, but once they did, hey, a check is a check, an Andrew Jackson is an Andrew Jackson.

That all changed in 1950, thanks to Frank McNamara and Diners Club. McNamara left home without his checkbook one evening and decided it was time to introduce a new way to pay for things at merchants. So, rather than limit consumers to being able to buy using what they had (cash or check), McNamara decided to issue a card to consumers they could use at multiple merchants that would allow them to pay a single bill at the end of the month for purchases made at those merchants. He decided to launch this in the restaurant sector and with affluent consumers.

He also changed the competitive landscape by doubling the number of payments suppliers overnight, introducing a new set of rails and a new payments substitute. But he also did something else: he introduced a new buyer into the mix.

Merchants now became a buyer of payment services since they had to both agree to accept his new payment method that used these new rails supplied by Diners Club and to pay a fee for doing so. The pitch to this new set of buyers was the ability for them to attract new consumers who would, in turn, deliver incremental sales.

Diners Club ignited this new payments scheme by mashing up the role of both supplier and buyer – operating the rails and as banks did before, distributing the new payments products to merchants, and introducing a new power player on the supply side of the industry.

Diners Club and McNamara ushered in a new competitive dynamic in payments. The three-party system was born – rails, merchant and the consumer.

At launch, Diners had 14 restaurants and 200 customers. By the end of year one, thanks to the magic of network effects, there were 1,000 restaurants and 20,000 customers. Eight years later, in 1958, American Express entered the payments industry with its own three-party network product that competed with Diners Club. So did Carte Blanche. At that point, the payments landscape had four suppliers, three three-party systems that operated a business model that charged merchants for accepting their payments method (Diners, Amex and Carte Blanche), and one that didn’t (the government).

Enter Visa and MasterCard

Let’s skip ahead a few years and over the complicated history of how Visa and MasterCard evolved. It’s now 1966.

MasterCard entered the payments market as a supplier but did it in an entirely new way. It organized banks into a national network that would enable merchants coast to coast to accept a general-purpose payment product. This model separated the extension of credit (what the banks who were part of the network would do) from the operation of the payments rails and the setting of the payments standards (what MasterCard would do) and processing of the payments transaction (what third parties would later do on behalf of merchants). Basically this model introduced a fourth party – the payments network – that gave banks the chance to offer a new product to their customers and, therefore, a new way for merchants to be paid.

In 1976, Visa was the name given to the national bank cooperative that was started by Bank of America in 1958 (Bank Americard); it would operate the same way.

These sales pitches to banks and merchants came at a very good time. Throughout the mid-to-late 1950’s and 1960’s, merchants had been extending revolving credit to consumers and were happy to relinquish the provision of credit to someone else who would bear the risk. They also didn’t mind paying a fee to the bank for that service in exchange for being able to accept a card that made it easy for consumers to buy things (and even buy more things) in their stores.

Banks didn’t have to be sold that hard either, seeing the opportunity in the market that American Express and Diners had uncovered and a way for them to add a new revenue stream by distributing payments products and extending credit. Consumers were perhaps the biggest beneficiaries of all. They could get a single card that could be used in place of the stacks of store cards that were inconvenient to carry, were extended credit, and had now multiple players vying for their business.

In the space of eight years, the supply side of the payment market had quadrupled in size. [Amex, Diners Club, MC, Visa, Carte Blanche are knocking on death’s door]

And that’s the way the competitive landscape in payments would stay until 1985.

Why so few new suppliers over such a long stretch of time?

The power in the payments industry was concentrated on the supplier side – those who operated the rails over which new payments methods operated. They had built up scale economies in operating those national payments rails over the course of 35 years and had created national merchant acceptance for their products. They had invested in systems and standards that made it expensive and even impractical for others to replicate. Most any banks that mattered ultimately belonged to Visa or MasterCard, or often both, and were basically locked into those systems.

Rivalry missing?

So, where was the competitive rivalry in payments?

Well, for sure the payment rails competed, but the main competition was between the bank issuers, along with Amex (Diners Club and Carte Blanche had shriveled), all of whom vied for consumer to get one of their cards and use it to pay.

Banks competed for consumers to use their products. As card acceptance became more commonplace across all of the supplier-branded products, merchants didn’t really have the ability to “steer” payments choice to a particular product. Banks did. They tried really hard to introduce features and enhancements that made their cards more appealing to consumers than others. Suppliers such as Amex touted having a more affluent customer base that could drive more spending at merchants and charged merchants more to accept their cards.

Then a funny thing happened in 1985.

Discover entered the market. What made Discover decide that it could make a go of it after 35 years without a single additional new supplier entering the market?

The end of regulation helped a lot.

The 1970’s was a bit of a disaster for the payments business. Between the high inflation and interest rates, there wasn’t much profit to be had in the credit card business. Even though the suppliers served a national consumer and merchant base, regulation was on a state-by-state basis, and state usury laws capped interest rates at 10 percent to 12 percent. That changed in 1978, when the Supreme Court ruled that credit card companies could peg interest rates to the state in which they operated instead of the state in which their cardholders were located.

That Supreme Court decision, along with the end of the recession in 1982, changed the economics of the business. Card companies realized that they didn’t have to lower interest rates to keep consumers using their products. That created a very profitable card operation for banks and networks and stimulated consumer spending at merchants.

Discover, observing this dynamic, decided that the time was right to enter as a supplier – a new set of payments rails. And, like their predecessors, it, too, leveraged the forces on the buyer side of Porter’s framework. Discover saw the opportunity to create supplier power by turning a large merchant-customer base – Sears’ 25 million cardholders – into an incentive for merchants to want to accept a new payments alternative.

Discover not only introduced new rails, it also introduced a new product feature to make it attractive to consumers – the idea of cash back on purchases made on the card. It also decided to charge a lower fee to merchants so more merchants would want to accept its card product. Discover entered the competitor landscape as a new supplier, using the three-party model, which destabilized the buyer and supplier side and introduced a brand new product substitute all at the same time.

Over the course of the next 20 years or so, there wouldn’t be much change to the supplier side of the payments industry. Like the period of time between the 1950’s and 1985, most of the competitive rivalry was on the buyer side, with issuers competing for consumers to take and use their cards. Private-label store cards would emerge as niche supplier rails but not capture much market share since they were store specific and not interoperable. Supplier revenues and profits increased as scale economies drove efficiencies, and the use of cards, regardless of which bank issued it, only drove more volume over their networks. Life was good.

Over that time, large merchants would use the power of their transaction volume to negotiate more favorable terms with the networks. But other than that, it would then be 20 years, right around 2005 or so, before the next shock to the payments industry competitive field would be felt. The impact of that shock would not only change the competitive landscape for payments, but the field upon which the game of payments would be played.

Shock wave emerges

To be precise, that shock is actually five related shocks: the Internet, the mobile phone, cloud computing, regulation and the financial crisis of 2008. Together, these forces gave birth to new players, new technologies and new ways of serving merchants, banks and consumers, altering the competitive rivalry in payments in new and interesting ways

All of a sudden, the barriers to entry to the payments industry fell and the ways in which revenue and profits accrued would change.

New entrants used technology to make the card products that banks were offering consumers more attractive and useful – new rewards and loyalty schemes emerged enabled by these third parties who complemented existing products instead of replacing them.

The Internet gave merchants an additional storefront through which to serve consumers and a new channel through which to mobilize digital promotions to drive those consumers into their physical storefronts. The Internet also introduced new sources of competition for merchants and new places for consumers to use existing payments products. New players seized these new online storefronts to introduce new payments rails on the supply side – some successful, most not.

Merchants and banks joined forces to co-brand promotions and even card products directed to consumers to drive preference.

Regulation – The Durbin Amendment, specifically – changed the business model dramatically on the buyer side. No longer could banks charge merchants the same fees they once did for accepting debit products, which blew the business model for the DDA products tied to these debit card products to smithereens.

The new pricing scheme that resulted drove many marginal accountholders into the arms of alternative players. Merchants preserved their pricing power; banks ceded theirs. And there is every reason to think that the same battle will be fought over credit card fees in the not-too-distant future and every reason to believe there will be a similar outcome.

Cloud competing and new technologies have introduced a new software layer that sits between merchants and the payments rails. These players enable more a more efficient way of transacting and a more robust set of merchant services, marginalizing traditional processors in the process and shifting profits away from traditional players to these new software-based entrants.

The economy turned consumers into bargain hunters and, in the process, minimized the degree to which they valued the product set that traditional banks offered credit card customers – points based on spend. Instead, what consumers valued was a deal, an offer, or something that could be redeemed right away. The result was the entry of a whole new crop of third parties who would offer products that shifted consumer attention towards saving $10 rather than earning 1,000 points. This would force banks to rethink the value proposition of their card products, something that has become particularly important as the move to digital/mobile makes payments brands less visible and tangible once stored in digital wallets.

Smartphones set new pace

Smart mobile phones have intensified the competitive rivalry on a number of levels. Apps with embedded payments have spawned new entrants on many sides of the five-forces framework. New merchant categories emerge, thanks to the ability to payment-enable new capabilities, like getting a taxi or outsourcing household errands.

Mobile devices have become point-of sale terminals, disrupting the traditional players in the ecosystem that enable payment acceptance at merchants. Mobile devices also influence the ways in which consumers now shop, even in physical storefronts. New technologies also turn mobile phones into new form factors used to pay at the physical point of sale, important turf that everyone wants to claim since 95% of transactions still happen there.

But in spite of all of these developments and the change that the 2005 shocks have introduced, what has changed very little is the power of the supply side of the payments industry. There are still only four major payments networks – those that have powered the rails that the industry has used for the last 64 years: American Express, MasterCard, Visa and Discover (which acquired Diners Club in 2008). The only thing that has changed, at least so far, is that the plastic card is now a digital artifact in a digital wallet enabled by a connected device. All of the innovation that has been unleashed as a result of the new technologies and ways of interacting at merchants still rides the existing network rails.

Why?

They have built universal acceptance at all physical merchant locations now on an international scale, and that is a very, very difficult capability to replicate without great expense and over a very long time frame. Their rails are needed to facilitate acceptance of new digital and mobile products that are now possible given the increasing use of digital products as payments methods across all retail channels, including the physical storefront.

These digital products are not necessarily substitutes for existing card products, they are just enabled by new technologies that rely on mobile or other connected devices as the conduit for the payment transaction. Many digital wallets or apps with embedded payments in them actually leverage card products that ride existing payments networks. And supplier networks continue to make money and accrue profits so long as consumers use their branded products – the plastic card, a registered account in a mobile or digital device – it’s all just volume for them.

Rivalries heat up

This reality has given birth to some new and interesting plays that have intensified the competitive rivalries in payments.

In what the industry regarded as a pretty gutsy move, Discover, as both the newest and smallest set of payments rails, announced its intention in August 2012 to increase the number of competitors on the supply side of the payments industry by licensing its network to innovators that wanted to gain international merchant acceptance for their digital products at the physical point of sale. PayPal, the player that had entered the payments space in 1999 as an online-only payments network, was its first partner.

Like Discover’s move some 27 years earlier, it could use its 120 million digital wallets to entice merchants to accept it. Today, PayPal is using the rails supplied by Discover to expand its physical footprint via a variety of digital and card products.

MCX, a coalition of merchants that account for more than a third of all consumer spending in the U,S,, is creating its own mobile-only payments solution that will ride a new set of rails – the ACH network operated by a coalition of banks established in 1974. If MCX gains traction, suppliers volume and therefore their profits, will take a hit.

Chase, one of the largest card issuers in the U.S., used its buyer power to negotiate an arrangement with Visa, the supplier of its payments rails to create something called ChaseNet. ChaseNet is an asset of the newly formed Chase Merchant Services group within Chase, which now operates its own set of rails. Chase Merchant Services, like American Express, Discover and Diners before it, now connects directly with merchants and consumers, essentially setting up a new three-party network that leverages the 150 million cards that is the Chase consumer card portfolio. Visa may not lose volume, but it will likely lose margin, and it remains to be seen how Chase prices its services to merchants that accept Chase branded products and the impact that will have on the competitive rivalries on the supplier and buyer side of the Porter framework.

clearXchange, a network of four of the seven largest U.S. banks, operates a P2P network today using the ACH rails. It seems positioned to parlay its consumer and bank relationship into a new supplier of payments rails, as well, perhaps setting up an alternative to today’s debit products or perhaps creating its own new set of rails that follow in the footsteps of the bank cooperatives that became Visa and MasterCard several decades ago. .

Square is building a merchant and consumer network that, at the moment uses existing payments rails, but is acquiring merchants directly and introducing hardware/software bundles that enable mobile payment for those consumers using its digital wallet product. It is leveraging existing supplier rails to build a consumer base for its digital wallet and is competing on the merchant side for acceptance of its payment product by offering integrated hardware and software terminal replacements to merchants that accept its wallet and other payments types as well.

Then, there are the myriad of players for which the ability to embed payments is creating whole new areas of commerce. Social recommendations sites that link payment to product or business reviews can shift power away from merchants to a new category of uber-merchant or aggregator. Apps that aggregate spare capacity and make it available for consumers or business to consume on demand and pay for without friction can do the same thing. Absent payment, these businesses would have no way to monetize their capability or even exist as a business. In both cases, this new category of buyer leverages existing supplier rails, but could destabilize existing merchants

So, what does that imply for the future of payments, and what can Porter’s five-forces framework tell us about devising a competitive strategy for the next 50 years?

Well, probably that given the power of the supplier networks and the lack of competition with any traction there, very little is likely to happen in the next decade to diminish the power of the supplier side in payments. All one has to do is to look at the stock prices of the existing rails to see where the profit pools in payments are. The real question is the extent to which the next 20 to 30 years could see a shift happening if any of these players get traction or new ones emerge. But, too much more, and I’ll spoil the kick-off session with Professor Porter and his CEO panel.

What I will tease is that Professor Porter’s counterparty, David Nelms, the CEO of Discover who made the bold decision to intensify the competitive rivalry in payments two years ago, will drive an interesting conversation about that very topic.

Porter and Nelms will talk about the tools that the existing suppliers have and could use or develop to further strengthen bank and merchant reliance on their rails – weakening their bargaining power and stunting new entrants and their growth.

They’ll talk about the role of the banks in this chapter of payments competition and the threat to their future by alternative players and new suppliers and regulation, which could gut their source of profits. They’ll talk about the profile and focus of new entrants, and which of the five forces they believe is either too weak so they can replace it, or strong enough that they can join forces and leapfrog the other players to create stronger buying power on the supply or buyer side. They’ll also talk about the likelihood of a new set of rails emerging, one that is based on a digital or virtual currency that can also completely disrupt existing suppliers such as bitcoin.

Finally, they’ll debate with the CEOs their views on whether the existing networks and the merchant acceptance that they enable are so entrenched on a global basis that they’ll never disappear, or whether mobile is the big game changer that could, in time, introduce a new supplier dynamic that marginalizes their power. And they’ll talk who they see way out on the horizon, who could appear to introduce a completely new model and way of doing business, borne out of a simple solution to an obvious need that we are all too busy to recognize.

And, to think this is only a two-hour session.

Professor Porter, Discover CEO David Nelms and 10 of the most dynamic CEOs in the space in your own personal payments competitive strategy immersion course. Can you really afford to miss out on this one?

Reinventing and Reimaging The Future of Payments | March 19, 2014 |

Jan Estep | President | NACHA

Rocco Fabiano | President | Qualcomm Retail

Chris Gardner | CEO | Paydiant

Alex P. Hart | President Official Payments

Mike Kennedy | CEO ClearXchange

Ron Totaro | President Pitney Bowes Financial Services

Mike Passilla | CEO Chase Merchant Services

Seth Priebatsch | CEO LevelUp

Scott Rankin | COO | MCX

Bill Tauscher | CEO Blackhawk

To request an invitation, please use this link.