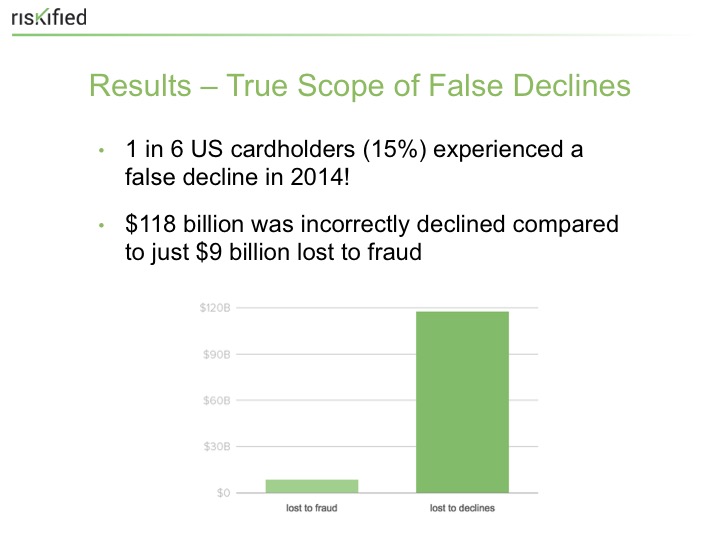

Falsely declining the transactions of online consumers is a move merchants just can’t afford to keep making: last year alone, nearly $118 billion was left on the table due to false declines. In an exclusive digital discussion, Andy Freedman, Chief Marketing Officer at Riskified, explained to MPD CEO Karen Webster, how “storytelling” can lower the risk of merchant’s risk of fraud, while increasing their revenue opportunity. Sound implausible? Not when you see the impact on conversions.

Falsely declining the transactions of online consumers is a move merchants just can’t afford to keep making. Last year alone, nearly $118 billion was left on the table due to false declines. The impact isn’t just a loss of that sale that time but disgruntled consumers who never return.

With the U.S. market finally reaching the post-EMV shift milestone (where, everyone says, a surge in card-not-present fraud is inevitable) and the looming holiday season, now is the time for merchants to understand how to better manage their fraud initiatives and reduce the impact of false declines.

But in today’s payments ecosystem, are merchants capable of guaranteeing fraud prevention without treating good customers like criminals?

Riskified thinks so.

The answer may lie in gaining a better understanding of how customers feel and react when it comes to false declines, which is why Riskified went directly to consumers for answers. By surveying 3,200 U.S. cardholders about their experiences with false declines last year, the company hopes its research can give merchants the insights needed to address the significant false decline problem.

As Andy Freedman, Chief Marketing Officer at Riskified, explained to MPD CEO Karen Webster, shining a light on the true cost of false declines will require a shift in the strategy and mindset merchants currently use to fight fraud.

Advertisement: Scroll to Continue

MONETIZING THE IMPACT

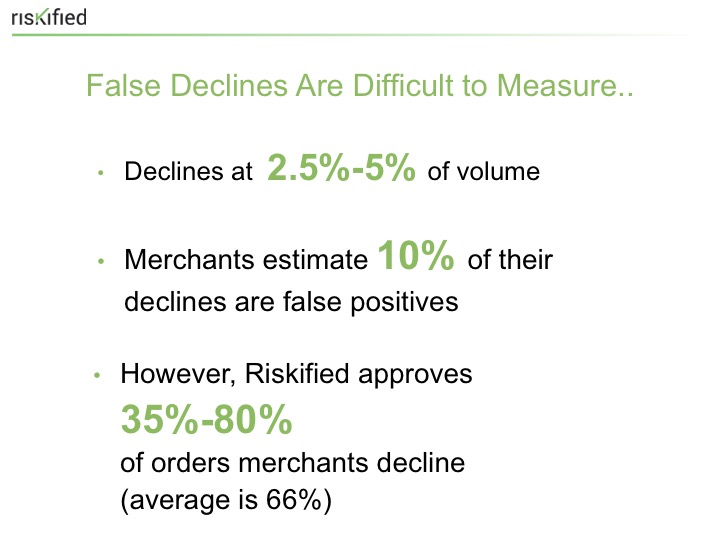

One of the biggest barriers to being able to truly and accurately measure false declines lies with the fact that there is a huge discrepancy between merchants’ perceptions of the problem and its reality. Riskified’s data clearly shows that merchants are declining many more legitimate transactions due to the fear of fraud than they realize — costing them big time.

Freedman noted that retailers overlook false declines for a variety of reasons, which include prioritizing their focus on other fraud-related metrics, interpreting the issue as an “invisible” problem, lack of time, limited resources and being unfamiliar with best practices surrounding the matter.

But saying “no” to the wrong customers can be detrimental to a company’s business, which is why retailers cannot afford to “think about fraud as solely a bottom line impact,” Freedman explained.

“The financial impact is vast; it’s not just that one transaction you are saying ‘no’ to. It is potentially the lifetime value of a very profitable customer,” he added.

According to Freedman, monetizing or quantifying the false decline impact retailers face must be looked at in terms of fraud costs (chargebacks) versus declined costs (potential revenue they are leaving on the table). Riskified’s research found a substantial variance between what’s being lost through incorrect decline, $118 billion, versus the $9 billion in real measurable fraud loss.

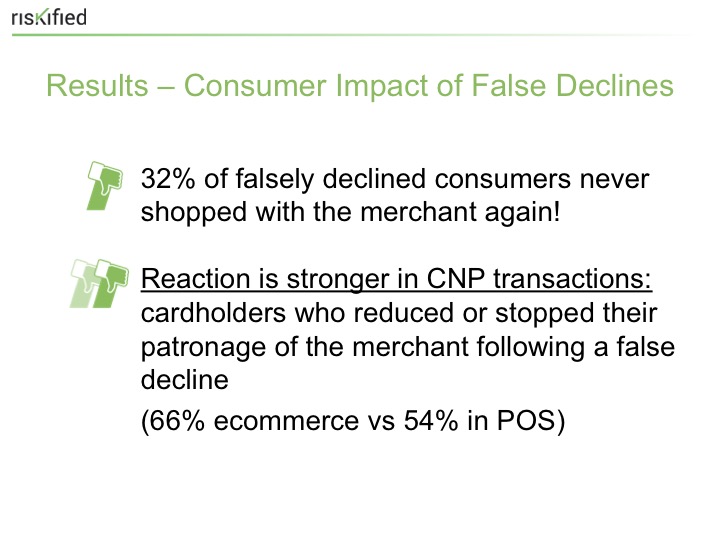

Considering the fact that one in three falsely declined customers reported never purchasing from that same merchant again, it’s easy to see the devastating financial repercussions turning down the right customer for the wrong reasons can have.

CUSTOMERS TAKE IT PERSONALLY

It’s not surprising that consumers are not very forgiving when it comes to having to deal with false declines, and in today’s commerce marketplace, it’s easier than ever for them to take their business elsewhere and never look back.

“Whatever the transaction may be, being told ‘no’ is an affront, and 32 percent of customers overall who have been falsely declined vow never to return to the merchant,” Freedman said.

That reaction from consumers proved even stronger when it came to eCommerce, with online channels offering very little barriers to people moving on to another merchant.

“Part of that is because it’s so easy. If you have one browser open on a gift that you like, it’s just as easy to open a new tab and go to the next player in a very quick amount of time,” Freedman stated.

While it may not be a surprise to learn consumers loathe false declines, Riskified’s data did reveal that in most cases the best customers are shockingly the ones bearing the brunt of the problem.

As Freedman explained, the two most affected segments of false declines are Generation Y and high-income consumers, both for reasons very specific to each demographic and the many factors that surround their shopping habits and behaviors.

Young adult consumers, who are naturally seen as the “consumers of tomorrow,” showed the strongest response (42 percent) to abandoning their merchant after their transaction did not go through. In the past year, nearly 24 percent of respondents in this demographic reported at least one decline, which Freedman said could have been due to factors such as using a different shipping address from the billing address associated with a payment method or even an increased number of orders being made from a single IP address in the case of students trying to make a purchase while on a college campus.

High-income consumers — those earning $100,000 or more a year — have a tendency to raise red flags due to the fact that false-positive decline rates increase significantly for purchase totals over $250. Twenty-two percent of high-income cardholders experienced a false-positive decline over the past year, and over half (58 percent) reported that they either limited or stopped their patronage of the merchant following the decline.

“At the very base level, we are all trying to be automated and efficient, but sometimes that efficiency of speed causes inefficiency in approval,” Freedman said. “The reality holds that two of your most attractive segments as a merchant are the ones you are impacting the most by your decisions.”

UNRAVELING THE FALSE DECLINE PUZZLE

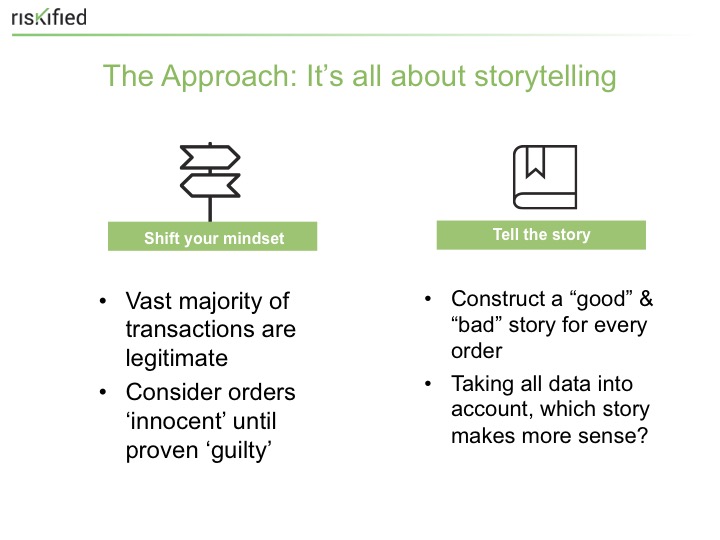

Ultimately, combating the impact and incidents of false declines must start with a big shift in the mindsets of merchants.

“We need to make sure we are looking at our customers as innocent unless proven guilty,” Freedman said, noting that it can be very difficult when the data surrounding the transaction or order may say otherwise.

“We always want to make sure that we understand who this customer is and why they would be placing an order with the components that we see,” he continued.

Riskified’s approach to fraud prevention, especially in the case of false declines, involves using storytelling to paint a more clear picture of whether a transaction is being made by a fraudster or an authentic consumer.

It requires attempting to tell two stories — that of the legitimate customer and the fraudster — and using risk management to make a decision on which one is actually more believable. It may sound unorthodox, but the approach is rooted in analyzing the details surrounding an attempted transaction and determining any common explanations that could prove it is legitimate based on the risk indicators being used.

“It’s important to always look at a story holistically. The point we are trying to make here is that letting yourself get too easily swayed with the negative part in the story is going to make you more eager or quick to decline, and you’re going to lose transactions that are actually pretty easy to approve,” Freedman stated.

Automation is a key part of the technology used by Riskified to reduce false declines, which aims to make machine learning even smarter through the act of making judgments based off of analyzing real human behavior.

For its clients, Riskified focuses on eliminating the use of automatic declines, increasing efforts to study and collect dynamic data, basing approval or decline decisions on multiple data points and linking data across transactions to reveal meaningful patterns and trends.

“Our business at its core is about guaranteeing satisfaction on two sides: on the customer side, which means making sure more orders are being sold to legitimate customers and keeping them happy, and on the merchant side, what that means to us is that every time we approve a transaction it is done with a guarantee,” Freedman stated.

To watch the full webinar replay please click the video shown below.