Paying a merchant with a promissory note is an antiquated concept at a time when consumers’ wallets — both the physical and digital varieties — brim with payment options. Yet, in the world of B2B commerce, paying on credit is alive and well.

Paying a merchant with a promissory note is an antiquated concept at a time when consumers’ wallets — both the physical and digital varieties — brim with payment options. Yet, in the world of B2B commerce, paying on credit is alive and well.

The informal rules of trade credit allow businesses to take weeks, if not months, to pay their suppliers. Just how widespread these practices are can be illustrated with one startling figure: $3.1 trillion. This is the net amount U.S. firms have suspended at any given time in accounts receivable (AR), according to PYMNTS research. In the SMB Receivables Gap: The Business Impacts Of Trade Credit Playbook, the latest in a series in collaboration with Fundbox, PYMNTS examines how these entrenched patterns affect everything from firms’ daily operations to their capital investments and marketing.

The informal rules of trade credit allow businesses to take weeks, if not months, to pay their suppliers. Just how widespread these practices are can be illustrated with one startling figure: $3.1 trillion. This is the net amount U.S. firms have suspended at any given time in accounts receivable (AR), according to PYMNTS research. In the SMB Receivables Gap: The Business Impacts Of Trade Credit Playbook, the latest in a series in collaboration with Fundbox, PYMNTS examines how these entrenched patterns affect everything from firms’ daily operations to their capital investments and marketing.

Our research reveals that trade credit is especially challenging for early-stage businesses and companies with low operating profit margins. Yet, trade credit also creates risk for more established and high-margin firms, which tend to be more active and generous in extending trade credit.

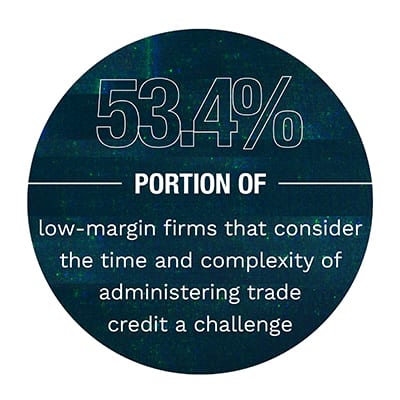

More than half of respondents, regardless of their profit margins, cite the time and complexity involved in administering trade credit as a chief challenge. Among high-margin firms, 54 percent view this as a problem, as do 53.4 percent of low-margin firms. Other challenges include the risk of customers paying late, which was cited by approximately half of respondents, and having too much money locked up in AR, which was cited by about 47 percent of firms.

More than half of respondents, regardless of their profit margins, cite the time and complexity involved in administering trade credit as a chief challenge. Among high-margin firms, 54 percent view this as a problem, as do 53.4 percent of low-margin firms. Other challenges include the risk of customers paying late, which was cited by approximately half of respondents, and having too much money locked up in AR, which was cited by about 47 percent of firms.

Where the experiences of low- and high-margin firms diverge is in the payment terms they offer. The average AR term extended by established, high-margin businesses is 40.3 days, while the average term is 25.6 days for early-stage, low-margin firms. High-margin firms are able to do this not only because they have healthier cash flow, but because they have greater access to financing products. In fact, low-margin firms are nearly twice as likely as high-margin firms to experience cash shortfalls on a regular basis. According to our findings, 30.9 percent of the former do so, compared to 16.7 percent of the latter.

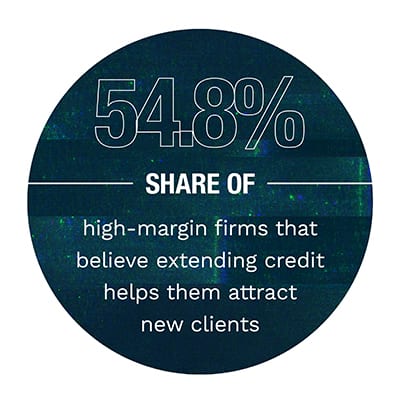

The ability to be more flexible with payment terms helps high-margin firms to court new customers and cement the loyalty of existing ones. Among high-margin firms, 55.3 percent believe extending credit helps create loyal customers, and 54.8 percent believe it enables them to attract new clients. In comparison, less than half of low-margin firms (45.4 percent) believe offering credit helps customer loyalty, and just 47.4 percent believe it helps expand their clientele.

The ability to be more flexible with payment terms helps high-margin firms to court new customers and cement the loyalty of existing ones. Among high-margin firms, 55.3 percent believe extending credit helps create loyal customers, and 54.8 percent believe it enables them to attract new clients. In comparison, less than half of low-margin firms (45.4 percent) believe offering credit helps customer loyalty, and just 47.4 percent believe it helps expand their clientele.

Extending credit comes at a cost to high-margin firms, however. More than a third of their customers pay them late, according to our research, while less than a quarter of the customers of low-margin firms do so.

To learn more about the hurdles trade credit creates for U.S. businesses — and how they can overcome them — download the report.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More