Most consumers probably don’t have strong opinions about their banks, since the relationship tends to be more transactional than emotional.

However, in the 2019 Retail Banking Report, a study by Reputation.com that analyzed online data relating to retail banking locations for 23 major U.S. banks, the banking industry was found to be lacking.

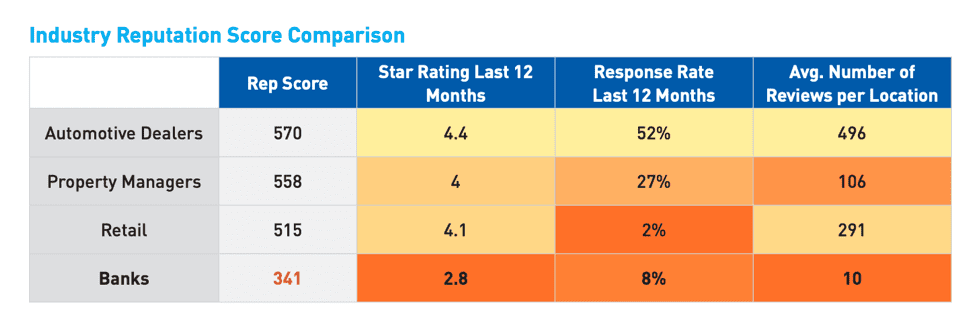

The study came up with Reputation Scores, measured on a scale of 100 to 1,000, based on online reviews, accurate listings, social media, search results and customer engagement.

At a high level, retail banking didn’t score as well as other industries with a 341, 174 points lower than retail’s 515. Automotive dealers (570) and property managers (558) fared best of all.

The low score for retail banks is due to factors like star ratings, which equaled 2.8 in the last year, a low number of customer reviews, which affects search result ranking, and a low response rate to online consumer concerns. Engagement drives loyalty, so being responsive is in the best interest of a business.

Retail banks weren’t low-scoring across the board, though. Capital One had the highest overall reputation score at 405, followed by TD Bank (374) and Chase Bank (370). According to the study, over four years KeyBank responded to 79 percent of online reviews, while U.S. Bank responded to 71 percent.

Another notable finding from the study was that while online banking has become more popular, physical bank branches matter greatly to consumer satisfaction. Reputation.com analyzed consumer sentiment in online reviews and found that perception was influenced by the following: general staff, courtesy, wait time/efficiency, parking/facilities and competence.

Citizens Bank scored highest on general staff (3.2) but out of five possible stars, that’s still fairly low. Citizens Bank also scored the highest in other categories with a 3.7 for courtesy, 3.3 for wait time/efficiency, 3.1 for parking/facilities and 3.5 for competence.

The study didn’t examine in-depth why particular banks outperformed others. It’s not a stretch, though, to imagine that banks that resonate with customers for courtesy and competence on-site are also attuned to the digital customer experience.

Last year, Citizens Financial Group, which received consistently high marks in the Reputation.com study, launched Citizens Access, a nationwide, direct-to-consumer digital bank.

John Rosenfeld, president of Citizens Access, told PYMNTS in an interview that offering digital banking was a natural progression since direct bank deposits have grown six times faster than traditional bank deposits over the past few years. “To address these evolving customer needs, we designed Citizens Access to provide an exceptional digital experience where every task is intuitive and easily accomplished, even on a mobile phone,” he said.

A majority (58 percent) of consumers prefer digital banking to other methods, though engagement is important in all channels, whether at branches, online or mobile, so financial institutions have to balance the digital banking experience with service in physical locations.

Sherif Samy, senior vice president of North America at Entersekt, told PYMNTS in an interview that banks are dealing with a “significant level of transformation” in consumer interactions and need to meet diverse needs, from younger tech-reliant consumers to older users who prefer banking in-person.

Samy also explained how mobile is the key in creating an omnichannel banking experience. For example through a mobile device banks can tell where a consumer is and offer services based on location or send push notifications for transaction approvals to reduce fraud.

In an interview with PYMNTS, Jim Priestley, chief revenue officer at Feedzai, also mentioned the importance of mobile banking in connecting the online and offline worlds. Where once mobile strategies were reserved for big national banks, now community banks and credit unions have also adopted mobile offerings.

According to the latest Credit Union Tracker, a majority (59.5 percent) of consumers think it’s “very” or “extremely” important for credit unions to offer mobile apps.

Customer experience in all channels directly affects satisfaction. “Most applicants would prefer to submit an online application without having to go into a branch, but not even half of banks that offer online applications support the entire account application online,” said Priestley. The customer onboarding experience can be marred by directing an online applicant to a physical branch for identity verification.

Connecting digital and physical approaches for customer convenience can improve retail banking’s reputation and in turn translate to customer satisfaction and loyalty.