Certain events stand out in stark relief for reminding us of just how interconnected the global economy is in the 21st century.

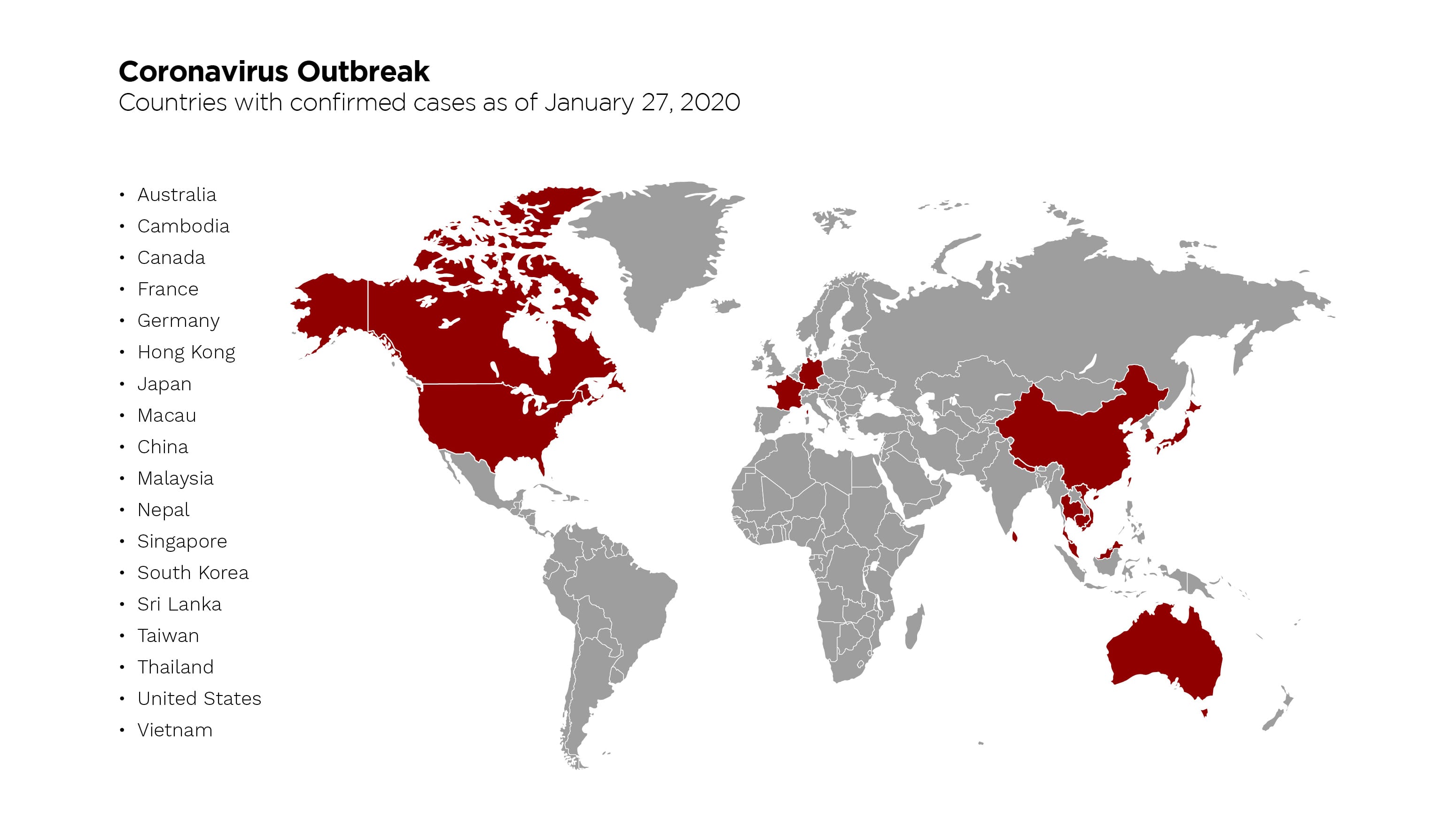

Bank runs. Trade wars. And now, most recently, the coronavirus pandemic that, at this writing, has spread to 18 countries across the globe, spanning Asia, Europe and North America.

The death toll is on the upswing. Though there are concerted efforts to find vaccines and cures (China is using HIV drugs as a treatment), and we hazard to guess that eventually there will be effective treatments, the impact on the global economy promises to be a lingering one.

SARS as Prologue?

SARS as Prologue?

If past is prologue, and history never really repeats itself, but rhymes, there may be some parallels with the SARS outbreak that marked the beginning of the millennium, in 2002 and 2003, and was a viral infection that was also identified as a coronavirus.

One study, via the National Center for Biotechnology Information and authored by Jong-Wha Lee and Warwick J. McKibbin, who are affiliated with Korea University and The Australian National University, said “just calculating the number of canceled tourist trips, declines in retail trade and similar factors is not enough to get the full impact of SARS” because of the linkages within and between economies and sectors. And through the authors’ models, the global economic loss from SARS came close to $40 billion in 2003.

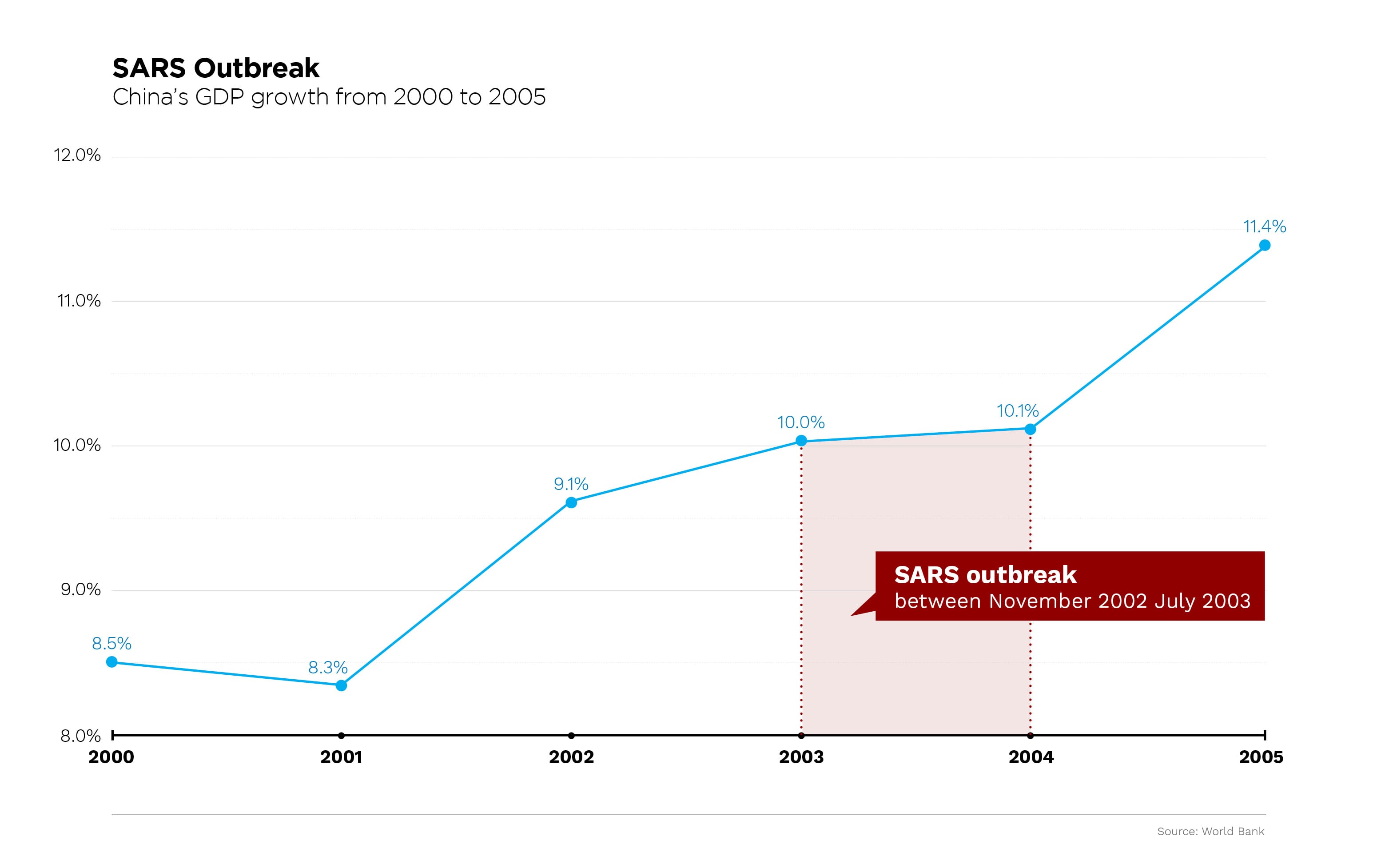

To be sure, economic growth rebounded quickly, from 2.9 percent to 4.4 percent from 2003 to 2004, via World Bank figures. Drill down a bit, and the World Bank estimates that China’s own GDP growth accelerated from 2002 into the ensuing few years, from 9.1 percent in 2002 to more than 1o percent in each of 2003 and 2004.

In the greater scheme of things, then, SARS — where about 800 people died and more than 8,000 were infected — did not do much to dampen the momentum that was already in place.

Is it Different This Time?

Is it Different This Time?

To be sure, each pandemic is different and carries particular new challenges for medical professionals and governments — and industries, too. The situation is fluid, and thus far, roughly three thousand cases have been reported, with the vast majority of those cases in China (at more than 2,800).

In an interview with CNBC, former FDA Commissioner Scott Gottlieb stated that the coronavirus outbreak is more contagious but less severe than had been seen with SARS. To get a sense of that speed of contagion, data from the World Health Organization, as recounted by CNBC, estimated that it took two months for SARS to reach 456 individuals. By way of contrast, the coronavirus had infected about double that number in a month.

Initial Impact

And here is where the cross-border impacts start to show.

With the vast bulk of cases still confined to China, the economic impact would likely be most concentrated in that country, and the general region. So far, the Chinese government has imposed a travel ban on roughly 35 million people. Travel bans, and self-imposed restrictions, mean that luxury goods sales, as individuals travel to destinations in Europe and the U.S., or as individuals buy at home would be seeing at least a short-term hit.

Hotel chains like Marriott get mid-single-digit to almost 10 percent of sales from China. Not all that long ago, Estee Lauder raised its earnings forecasts on strong demand in Asia, where sales in the region had been growing about 25 percent, and where China has been a mid-teens percentage contributor to revenues.

The anecdotal videos and pictures of empty streets imply that people have stopped congregating in places like malls and restaurants. McDonald’s, as has been well known, has shuttered at least some locations in the wake of the coronavirus news. And Yum China, which has closed some locations in the affected Wuhan city, as has Yum Brands, which gets roughly a quarter of KFC sales from China.

The stocks of these companies, for lack of a better word, have been savaged, at least in recent sessions. On Monday alone, shares in Estee Lauder were down by more than 4 percent. Oppenheimer downgraded its ratings from “outperform” to “market perform” on the coronavirus developments.

For Estee Lauder and Marriott, the question looms as to whether sales lost in the short term will be recouped in the longer term. As a tell, those firms’ stocks were down more than companies like McDonald’s — by several percentage points. In many cases, airlines are offering refunds or permitting delays for certain tickets without penalty. Hotel rooms or theme parks that go empty lose money.

The demand for higher-end consumer goods may get a bit of reprieve by comparison, as demand can be fungible. A purchase put off for a month or two may be consummated down the line. But then again, luxury handbags or makeup that sit on shelves for too long get marked down. Other companies, such as Apple, which gets more than 16 percent of sales from China, may suffer too. As Chinese shoppers are estimated to account for a third of luxury goods spending, as these consumers go, so will the top lines of these companies.

Time will tell, but the timing isn’t great, at least for commerce. Chinese officials said Monday that they would extend the Lunar New Year holiday — which now is being extended to Feb. 9, in part to limit the movement of millions of people and to keep the virus from spreading. Last year, Chinese consumers spent $149 billion across the holiday — given this year’s headlines and quarantines, it’s unlikely that this year will see a flurry of spending.

Data from China’s Ministry of Commerce shows that retail sales had been on an upswing by about 8 percent year over year, topping more than $5.7 trillion, as noted by China Daily.

As retail is likely the first (and largest) part of the economy, consumption faces headwinds, if not a decline, in the face of a prolonged outbreak. China is less export-driven amid a trade war that has lingered for two years and the impact on growth will be more pronounced as the country has to look to the consumer to drive GDP more than has been seen before. No easy task, perhaps, as GDP growth slows from the 9 percent seen earlier in the millennium to a current 6 percent rate.

And, as China has emerged as a larger component of GDP growth, the headwinds would be greater than had been seen, say in the SARS outbreak seen years ago.

Ripple Effects Elsewhere And Looking Ahead

If the most significant impacts — even short-lived — are to the travel industry, then countries such as Japan would see a least some impact. Nikkei Asian Review estimates that in Japan, Chinese tourists accounted for a third of visitors, and spent about $16 billion. Overall, Japan’s GDP growth could be hit by 20 basis points or more, as reported in The Straits Times. Hong Kong, too, is weakened when China’s growth suffers, as the country grapples with its cases of the virus and the lingering impact of protests (that have already decimated tourism). Hong Kong has closed Disneyland (though hotels are open), suspended flights and declared a state of emergency as the coronavirus continues to spread.

We’re too early in the outbreak to know if, medically speaking, the coronavirus is less, equal or more severe than SARS. But, in terms of the stats — the infection rates, we’re gaining ground.

The economic impact, too, may seem muted, if measured in the tens of billions of dollars, where the collective economic output is in the tens of trillions of dollars.

But, psychology counts for a lot, and a prolonged pandemic would start to have repercussions beyond the Chinese consumer and travel and food firms. As global stocks swoon, albeit off of (depending on where you look) record highs, the wealth effect may suffer, with consumers in other regions, such as, well, here, reining in spending. Want a snapshot? On Monday, in the U.S., stocks were off by 1.6 percent, and on London’s FTSE, stocks lost the equivalent of half a trillion pounds of value.

That would be a double whammy for multinational firms. A notable ding to earnings may crimp growth plans, which in turn — eventually — might lead to pressures in the job market.

It will take a lot to get there, but in the truly global economic age — where money and people and, yes, public health risks move across borders as never before — anything is possible.