In early December 2019, few had yet heard of COVID-19. News reports were only just trickling in. It didn’t seem like the entire world was teetering on the brink of colossal change, but it was.

The health crisis wrought massive changes in all areas of life, with consumer spending behavior high on the list. We’ve embraced a new connected way of life tied together by payments, and how we pay today almost two years into COVID foreshadows more changes still to come.

For the inaugural edition of PYMNTS’ new series “Digital Economy Payments: How Consumers Pay in the Digital World,” we surveyed nearly 3,600 consumers in November, uncovering fascinating patterns that are being established by pandemic consumers. A notable finding is the great love consumers have for debit.

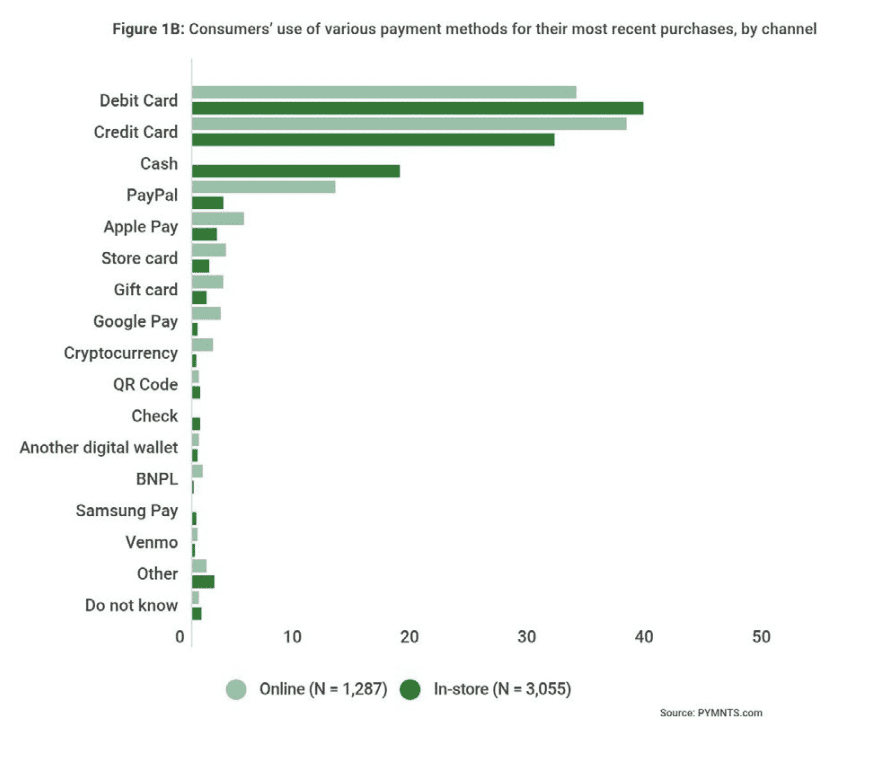

Per the study, “More than 38% of U.S. consumers use debit cards to pay for their purchases in physical stores, while nearly 33% use credit cards. The opposite is true when making online purchases, with 37% of consumers using credit cards to pay and 33% using debit cards.”

In all, 37% of consumers used debit cards to pay for purchases, while 32% said they used credit cards. Cash is a distant third, being used by just 13% of consumers we surveyed.

Get the report: Digital Economy Payments Report: How Consumers Pay in the Digital World

Get the report: Digital Economy Payments Report: How Consumers Pay in the Digital World

Credit Winning at Retail as Debit Rules Grocery

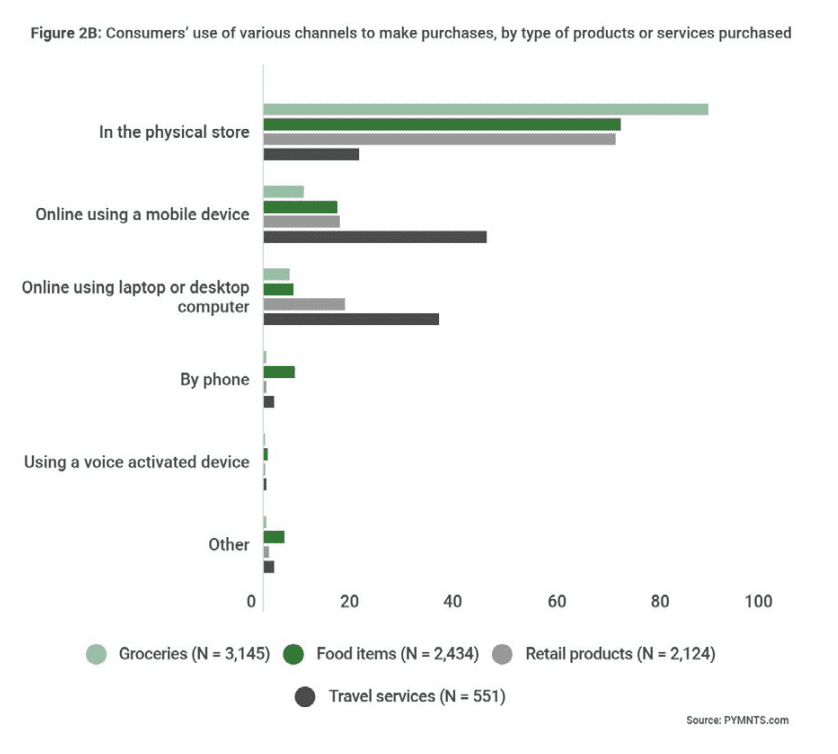

Digging into specific channels and goods, we find the digital shift pulling with it many pre-pandemic behaviors, like in-store shopping for certain items. For example, we found that 71% of grocery consumers continue to shop in-store, with 14% using a mobile device and 10% using a desktop or laptop.

When it comes to paying for groceries, the report notes that “consumers typically use debit cards regardless of whether they are buying them in a physical store or online. Overall, consumers spend $85.3 billion monthly on buying groceries in physical stores and nearly $19 billion when using mobile and online channels.”

This contrasts retail products, of which consumers purchased $127 billion using credit cards compared to just over $100 billion using debit.

That picture changes markedly in product/service purchases like travel. We found that 43% said of consumers are making travel-related purchases vis mobile, and that “credit cards are by and large the most popular payment method for these purchases — perhaps because consumers are accustomed to using them for their travel expenses or because many credit cards offer travel protection. Travel purchases also tend to be more expensive, and credit cards allow consumers to make big-ticket transactions now and worry about payments later.”

Buy now, pay later (BNPL) is hot, yet research found that just 4% of consumers used it to pay for retail products, and 1% or fewer used installments to pay for groceries in this study.

Get the report: Digital Economy Payments Report: How Consumers Pay in the Digital World

P2P Use Grows While Fraud and Decline Spell Losses

As it pertains to sending money fast, peer-to-peer (P2P) payments are big and getting bigger, as more consumers get comfortable using app-based money transfers.

Per the study: “P2P payment apps have fast become a popular method for consumers paying their friends, families and acquaintances, with 29% using these apps in the past month alone. These apps are particularly popular among bridge millennials and millennials, as more than 44% report using them to make P2P transactions.” We found that PayPal is currently the most used P2P payment, with PayPal-owned Venmo and Zelle also ranking well with P2P payment users.

Declines and fraud attend digital payments and cards, with the study finding that “10% of U.S. consumers experience a payment decline each month, with the average declined transaction valued at $149. This means that some $9.8 billion worth of transactions are declined every month.”

The incidence of fraud is lower than declines, but the damage is more costly. An estimated 7.4% of consumers surveyed experienced payment fraud within the past month, with average fraud loss at $343 — “more than double the amount involved in the average payment decline. This translates to roughly $13.3 billion lost to payment fraud each month.”

Get the report: Digital Economy Payments Report: How Consumers Pay in the Digital World

Get the report: Digital Economy Payments Report: How Consumers Pay in the Digital World