“Grocery, the growth engine of the business, is losing share rapidly. More than ever, Walmart shopper[s] are choosing the competition.”

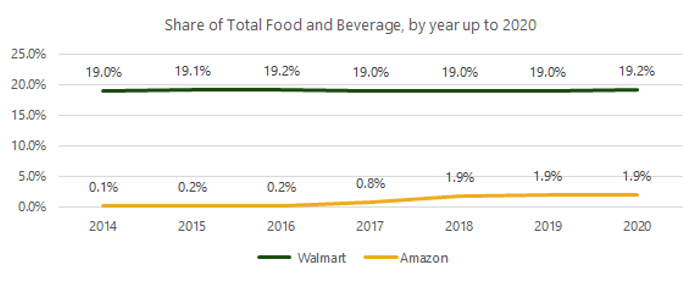

Over the course of the last 14 months, consumers have rewritten their shopping habits end to end — and merchants, particularly in grocery, have taken the opportunity to recreate their shopping experiences with an eye toward digital. When looking at the rivalry between the two retail giants, Amazon and Walmart, according to PYMNTS data, Walmart still holds a commanding lead in grocery. PYMNTS data showed that the “food fight” between the two titans remained strongly titled in Walmart’s favor — with $245 billion and 19.2 percent share of the category in 2020, it held a notable lead over Amazon’s $24.3 billion and 1.9 percent share.

Source: PYMNTS Data, April 2021

But that’s why Walmart is sounding the alarm. Groceries are Walmart’s single largest revenue driver, accounting for 56 percent of its domestic sales in 2020. But by its own admission — perhaps inspired by PYMNTS’ ongoing reporting of this data — shows the lead is slipping slightly after remaining largely stagnant for the last six-and-half- years. Walmart’s share of grocery has been roughly 19 percent since at least 2014, according to PYMNTS data. Amazon, on the other hand — while well behind in this race — is a grocery growth story. Taking into account only Amazon’s eCommerce food sales, its share jumps to 31 percent and accounts for about one-third of the category total. The remaining two-thirds of its grocery sales currently come largely from its Whole Foods unit, the chain of 500 upscale physical locations that it bought in 2017 for $13.7 billion to boost its presence in the highly competitive grocery industry.

Amazon’s grocery ambitions are growing — it was a little over a year ago when it began rolling out its second chain of physical grocery stores, Amazon Fresh, in locations nationwide. Not as a competitor to Whole Foods, but as a complement to it, designed to bring in an additional wave of buyers.

“We do think of these formats as complementing one another and serving different needs,” noted Jeff Helbling, vice president of Amazon Fresh stores. “Whole Foods is a longstanding pioneer and leader in natural, organic and clean foods. Amazon’s Fresh selection is fairly different. We see them operating next to one another, and we’re excited to offer customers the choice between the two.”

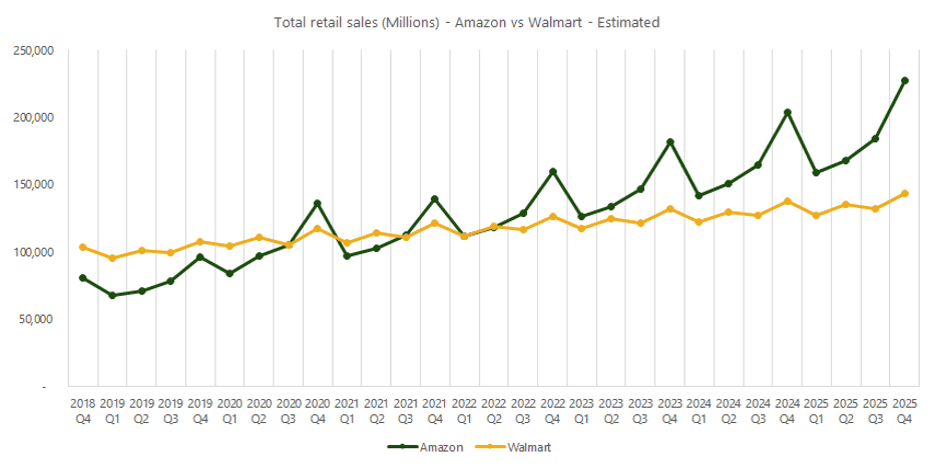

Amazon’s ambitious grocery game is just one part of its overall retail focus — which, according to recent PYMNTS research, positions Amazon to outgrow Walmart three-to-one over the next five years, with the former projected to bring in $315 billion in additional sales by 2025 and the latter only $100 billion. And Walmart’s issues, as the leaked memo indicated, go a lot deeper than Amazon’s encroachment on their territory as the race for grocery dominance heats up.

Source: PYMNTS Data, April 2021

The logos of Publix, Target and Albertsons, among others, all appeared in the secret Walmart memo, paired with data showing that consumers are increasingly selecting those competing grocers over Walmart. Another page of the document reads: “Walmart is not first and preferred. Must elevate quality assortment + value!”

In fact, those competitors are growing faster than Walmart — in Q4 2020, Walmart’s U.S. comp sales grew 8.6 percent and its U.S. eCommerce sales grew 69 percent. Meanwhile, Publix’s comp sales for the quarter grew 13.4 percent, Target’s grew 20.5 percent (while its digital sales grew 118 percent), and Albertsons’ same-store sales grew 11.8 percent and its digital sales grew 282 percent.

But Amazon isn’t Walmart’s only grocery nemesis. As forthcoming PYMNTS data indicates, 43.2 percent of grocery shoppers now use delivery aggregators to purchase their groceries, and 63 percent have been using them more over the last year. Some 21.5 percent of consumers have used an online order, pick up and delivery service such as Instacart during last year, and 21 percent are very or extremely interested in using it again.

Not surprisingly, the millennials and bridge millennials use the services more prevalently, with 40 percent of each expressing interest in using those services more in the coming months.

Then there is the threat from CPG companies going direct to consumer (D2C). Consumers, with more time to explore online for new products, are buying more grocery items directly from brands. PYMNTS data shows that 16.3 percent of consumers purchased grocery items directly from manufacturers, with 31 percent of bridge millennials doing so.

Read More On Grocery: