Amazon Versus Walmart Study Shows Who’s Winning Consumer Retail Spend

Retail behemoths Amazon and Walmart have become the two fiercest competitors for consumers’ retail spending. While the proliferation of mobile devices, apps and payment technologies makes online shopping ever more efficient, physical shopping seems increasingly friction-filled. As consumers seek more convenience, shopping has become a hybrid experience, blurring the lines between physical and online commerce.

Over the years, each retail giant has moved aggressively into the other’s turf: Amazon into grocery with Whole Foods, Amazon Fresh and Amazon Subscribe & Save; and Walmart into eCommerce with the acquisition of Jet.com. Both have also expanded into retail-adjacent areas, health and wellness in particular. While Amazon and Walmart continue to establish themselves as leaders in providing easy access to daily essentials, they also compete for consumers’ discretionary income, even as inflation shrinks spending power.

PYMNTS has been tracking these retail giants’ competition since 2018, gathering valuable insight into how they leverage their core strengths to capture market share in key retail categories. Each quarter, our analysts examine Amazon’s and Walmart’s quarterly earnings reports to reveal who is winning the battle for retail and overall consumer spend. We also explore how Amazon and Walmart compare in key retail segments.

In The Battle for Consumer Retail Spend: Amazon Versus Walmart Q2 2022, PYMNTS finds Amazon leading Walmart in both overall consumer and retail spend, a lead Amazon first captured in Q3 2020 earlier in the pandemic. As consumers moved their shopping online, Amazon flexed its eCommerce muscles, as Walmart’s share declined in nearly all retail categories. This includes discretionary spending and grocery, where Walmart’s share is slipping slightly quarter over quarter as Amazon intensifies its bid to capture more of consumers’ dollars.

In this report, we provide the key takeaways from Q2 2022 consumer and retail spending trends, with a particular focus on consumers’ discretionary spending. While inflation has taken a toll on consumer spending for essentials such as groceries and healthcare products, it has certainly had an impact on discretionary spending as well.

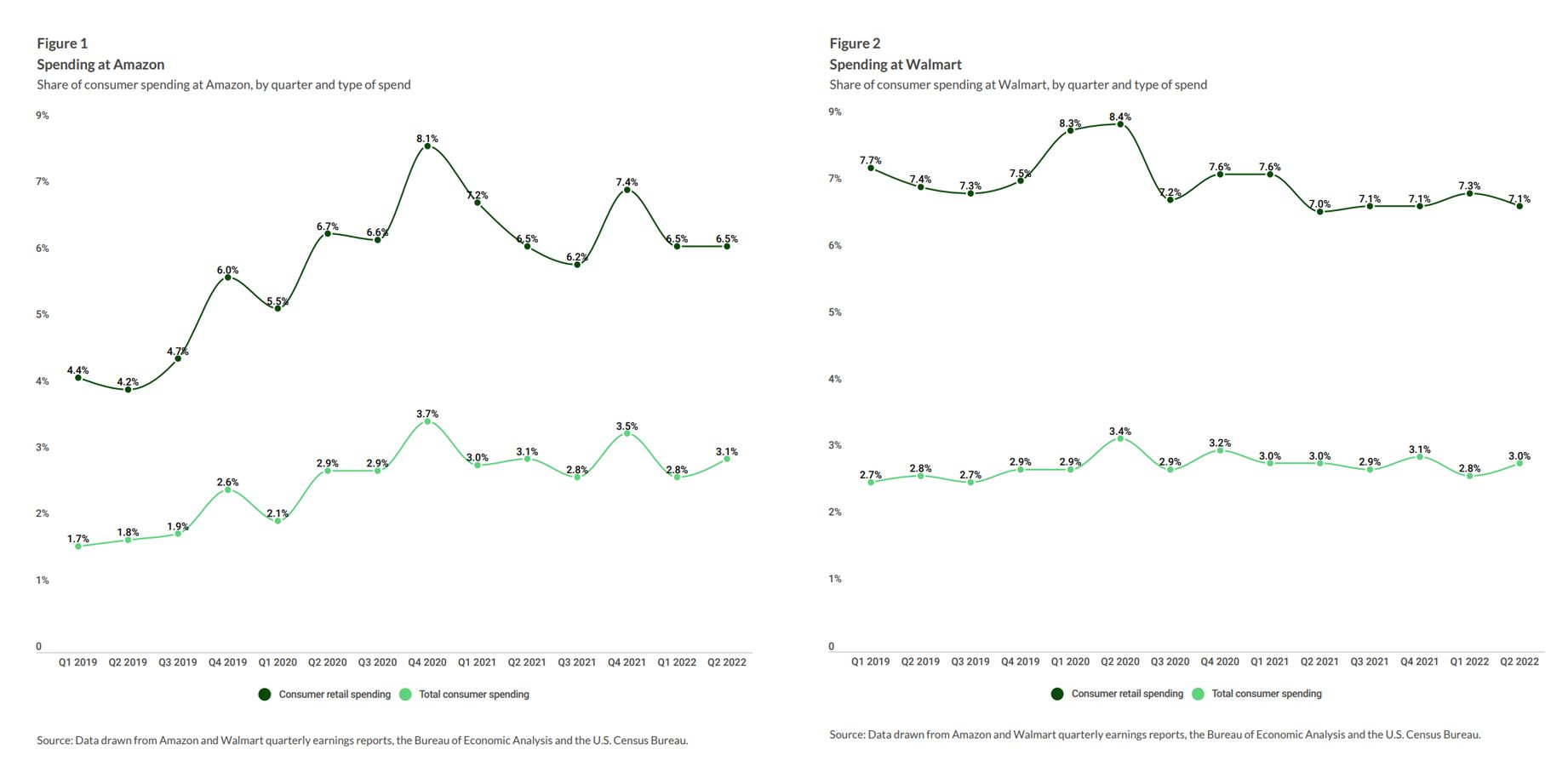

Amazon accounted for 6.5% of consumer retail spending and 3.1% of total consumer spending at the end of Q2 2022. But with its 7.1% share of consumer retail spending, Walmart has slightly outperformed Amazon again this quarter but has fallen slightly behind in total consumer spending at 3%.

In Q1 2019, Amazon held only 4.4% of consumer retail spending, which increased to 8.1% in Q4 2020. In Q1 2019, Walmart held 7.7% of consumer retail spending, reaching 8.4% in Q2 2020.

As of Q2 2022, Walmart’s share of consumer retail spending has slipped below its 2019 levels of 7.1%, yet the company still holds the lead in that area. Walmart saw a very slight increase in its share of total consumer spending, from 2.8% last quarter to 3% in Q2 2022.

While Amazon’s share of consumer retail spending held steady at 6.5% this quarter, the company saw a slight increase in its share of total consumer spending, which rose to 3.1% from 2.8% in Q1 2022. Compared to Q2 2021, Amazon’s shares of consumer retail spending and total consumer spending both remain unchanged. Meanwhile, Walmart’s market shares in both areas have remained steady since last year.

Amazon’s dominance of consumer retail spending reached a high of 8.1% in Q4 2021, while Walmart’s share has dropped from a pre-pandemic high of 8.2%. These shifts are interesting yet not surprising. During the pandemic, Walmart suffered and Amazon thrived, as consumers took to shopping online instead of frequenting large, brick-and-mortar retailers.

As pandemic-related restrictions began to subside, however, consumers returned to shopping in-store, cutting into Amazon’s burgeoning market share. Yet, in Q4 2021, Amazon’s share of consumer retail spend spiked to 7.4%, an indication that consumers did more holiday shopping online than they did in-store, an area in which Walmart could not compete.

With prices rising for everything from gas to groceries, inflation has dampened consumer spending. Overall market shares for both companies have dropped or remained stagnant in the first two quarters of 2022. Hopefully, the promise of everyday low prices or a frictionless, cost-saving subscription, such as Amazon’s Subscribe & Save, can help both companies appeal to inflation-weary consumers.

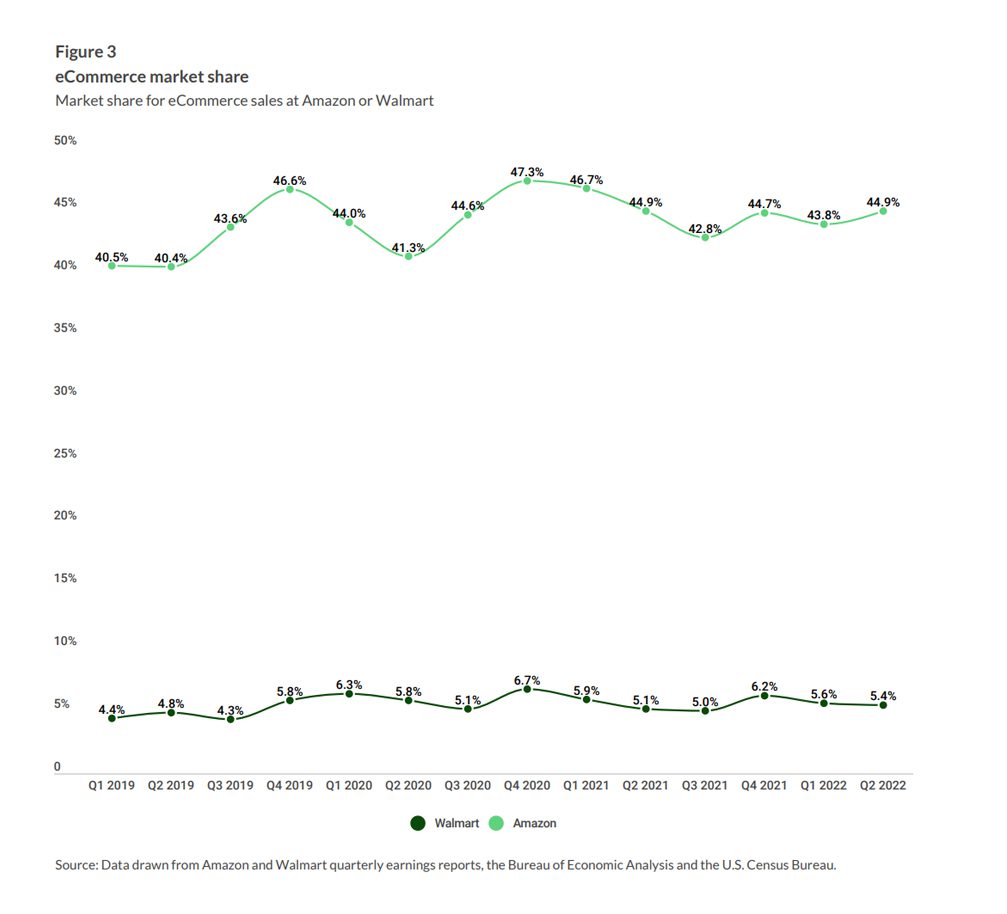

Amazon remains the preeminent eCommerce destination for American consumers, accounting for close to half of all online transactions in the United States in Q2 2021 and Q2 2022.

Although Amazon and Walmart’s shares in consumer spending are not far apart, Amazon remains the undisputed eCommerce leader, holding 45% of the market compared to 5.4% for Walmart. During Q1 2019, Amazon held 41% of the eCommerce market. Two years later, that increased to 45%, where it remains in Q2 2022. In particular, Amazon dominates eCommerce in sporting goods, hobby items, music and books (56%), electronics and appliances (54%), and health and personal care (43%).

Walmart started Q1 2019 holding a 4.4% share of the eCommerce market, which has only increased to 5.4%. Yet, Walmart’s eCommerce sales hit $13.5 billion in Q2 2022, a 12% increase over $12.1 billion in Q2 2021.

Again, the pandemic has been a key driver of Amazon’s growth in the past two years. Still, the company dominates the eCommerce market due to its extensive fulfillment expertise and vast resources — Amazon controls the shipping, ordering, packaging and delivery for all its products, while Walmart faces a long, uphill battle to become a serious competitor. This became especially evident in Q4 2020, when consumers took their holiday shopping online. Even as both companies saw spikes in eCommerce sales, Walmart had little chance of taking market share from Amazon.

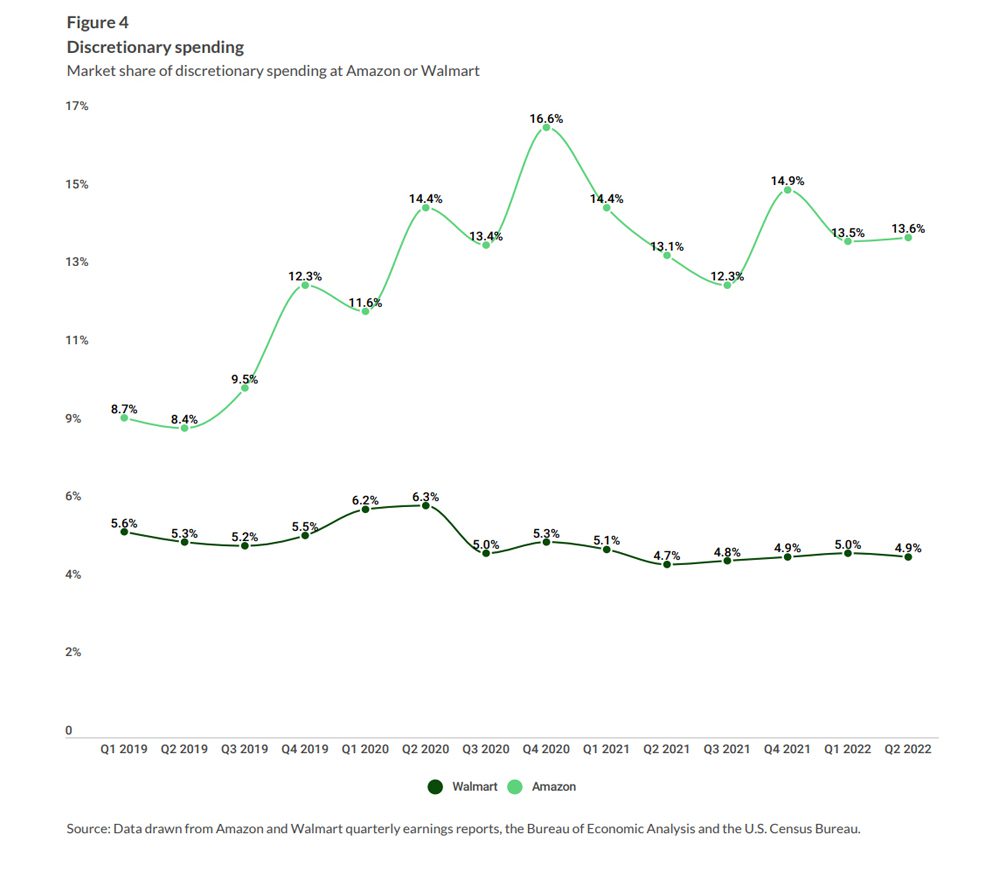

Amazon’s share of discretionary spending remains unchallenged, with Amazon holding 14% of this market versus only 4.9% for Walmart.

Amazon continues to take the lead in all discretionary spending on sporting goods, music, hobbies, clothing and apparel, furniture and home furnishings, and electronics and appliances. In Q1 2019, Amazon held 8.7% of consumers’ discretionary spending. By Q2 2022, this share had increased to 14%. Not surprisingly, Amazon’s share reached a high of 17% during the pandemic in Q4 2020.

Walmart, on the other hand, is losing ground on consumers’ discretionary spending. Walmart started Q1 2019 holding a 5.6% share; by Q2 2022, it had decreased to 4.9%. Amazon’s recent success could be attributed to the fact that it has tapped into consumers’ concerns about managing their spending in the face of rising inflation. Amazon regularly offers Prime members deals on essentials as well as items in the discretionary spending category.

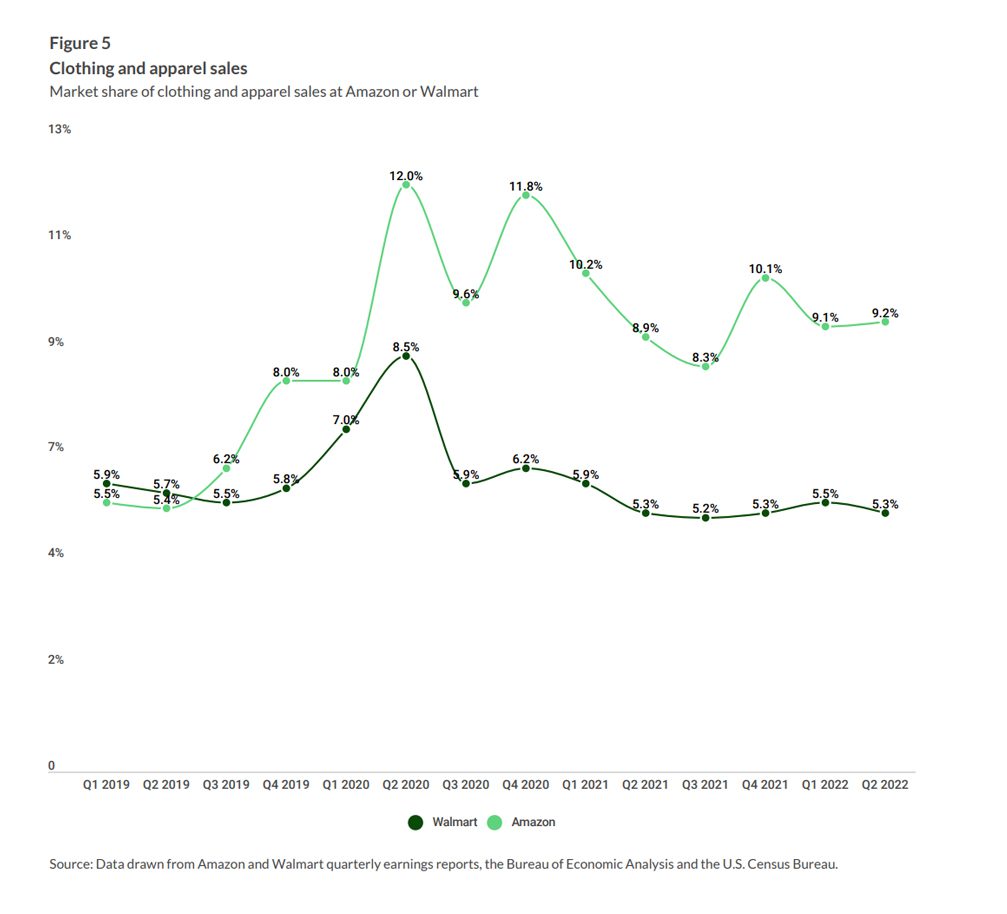

Amazon and Walmart both had less than a 6% share of the clothing and apparel market in Q1 2019. As of Q2 2022, Amazon’s share of 9.2% is almost double that of Walmart’s, which is at 5.3%.

In Q1 2019, Amazon held 5.5% and Walmart held 5.9% of the clothing market. By Q4 2019, Amazon had increased its share to 8%, while Walmart’s share stayed the same. The most significant change happened in Q4 2020, when Amazon nearly doubled Walmart’s clothing and apparel market share, at 11.8% compared to 6.2%. Amazon’s surge can be attributed to consumers taking their shopping online during the first holiday season of the pandemic.

In Q2 2022, Amazon maintained its lead in the market, holding 9.2%, while Walmart faced a slight decrease to 5.3%. With more than 50 in-house fashion brands, Amazon appeals to a broad demographic, many of whom still enjoy the convenience of shopping online.

Meanwhile, Walmart continues to target millennials and Generation Z with fashion-forward and influencer-tied collections. Despite Walmart’s efforts, Amazon remains the clothing market leader, even taking market share from other leaders.

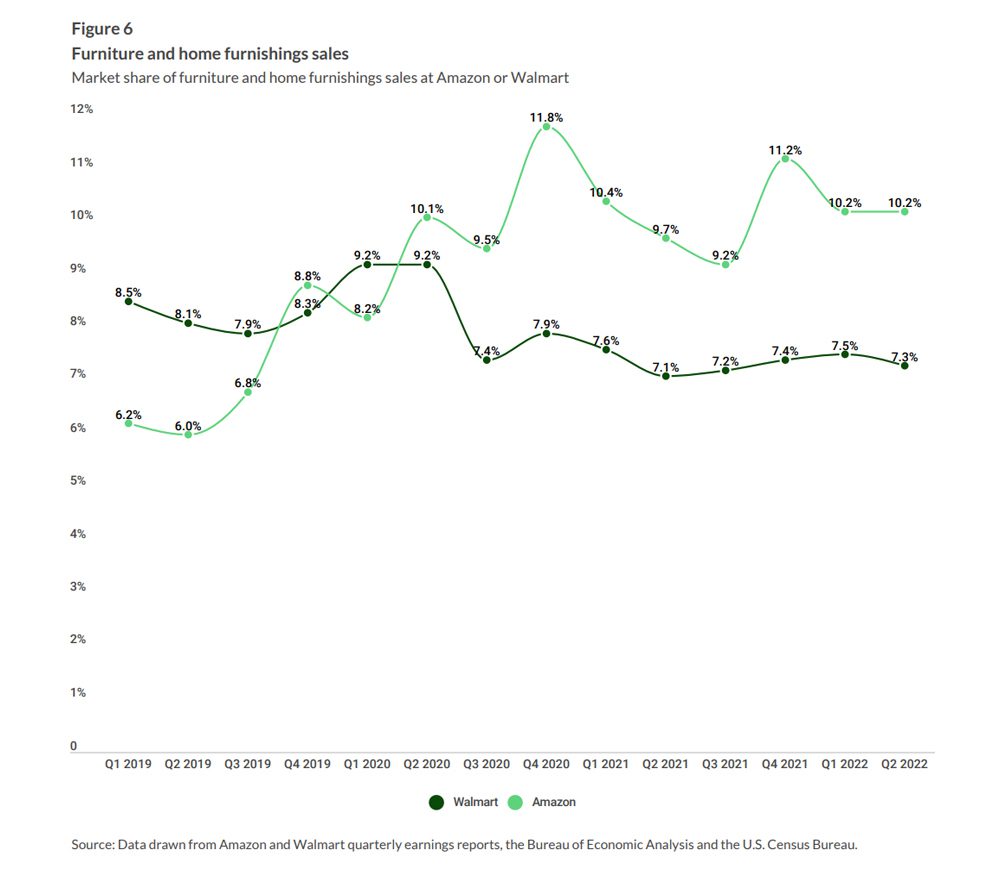

In 2019, Amazon was behind Walmart in the furniture and home furnishings category, holding 6.2% of this market versus 8.5% for Walmart. By 2020, however, Amazon had surpassed Walmart. As of Q2 2022, Amazon sits at 10% versus 7.3% for Walmart.

The market for furniture and home furnishings continues to move Amazon’s way, despite former leader Walmart having physical stores where consumers can inspect before they buy. Amazon’s home and furniture market share lagged behind Walmart’s by 2% during Q1 2019, but this had quickly changed by Q4 2019, with Amazon and Walmart’s shares statistically indistinguishable at 8.8% versus 8.3%, respectively. Amazon has continued to gain ground in this category, reaching its highest share of 11.8% during the fourth quarter of 2020 while Walmart held 7.9%. As of Q2 2022, Amazon’s current market share is at 10%, while Walmart maintains a solid 7.3%.

Again, these shifts can be attributed to consumers’ ongoing interest in online shopping, not to mention the convenience of free doorstep delivery of furniture for Amazon Prime members.

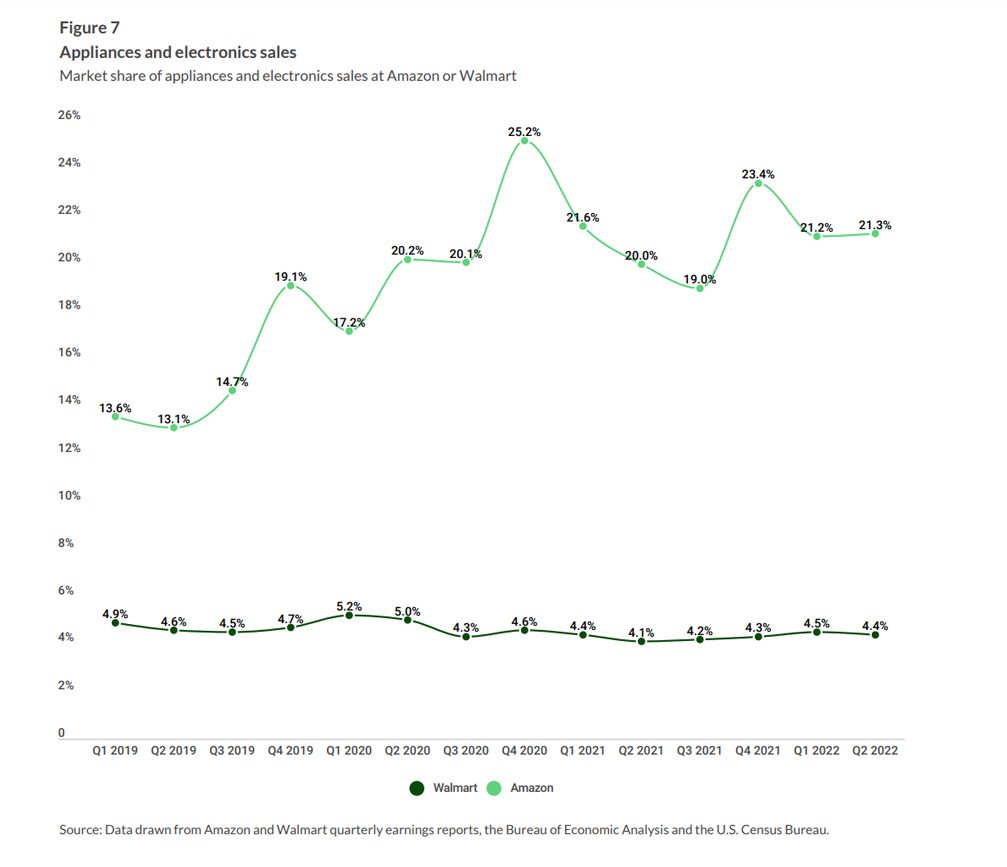

Amazon maintains its leadership in electronics and appliances, holding five times more market share than Walmart.

Since 2019, Amazon has held a higher share of the electronics and appliances market than Walmart. In Q1 2019, Amazon held 14% of this market compared to only 4.9% for Walmart. Since then, Amazon has increased its presence in this segment, reaching its highest point during Q4 2020 with a 25% share. Currently, Amazon holds 21% of the electronics and appliance market. In contrast, in Q1 2019, Walmart held only 4.9% of the market and has since maintained this footprint, with a slight decrease to 4.4% by Q2 2022.

Again, Amazon has managed to outpace Walmart in a segment that was once the exclusive domain of big-box, in-person retail giants such as Sears. Perhaps because eCommerce retailers such as Amazon offer detailed product information and reviews, consumers can confidently buy durable goods online without having to visit physical stores to get that information — and this trend shows no signs of reversing.

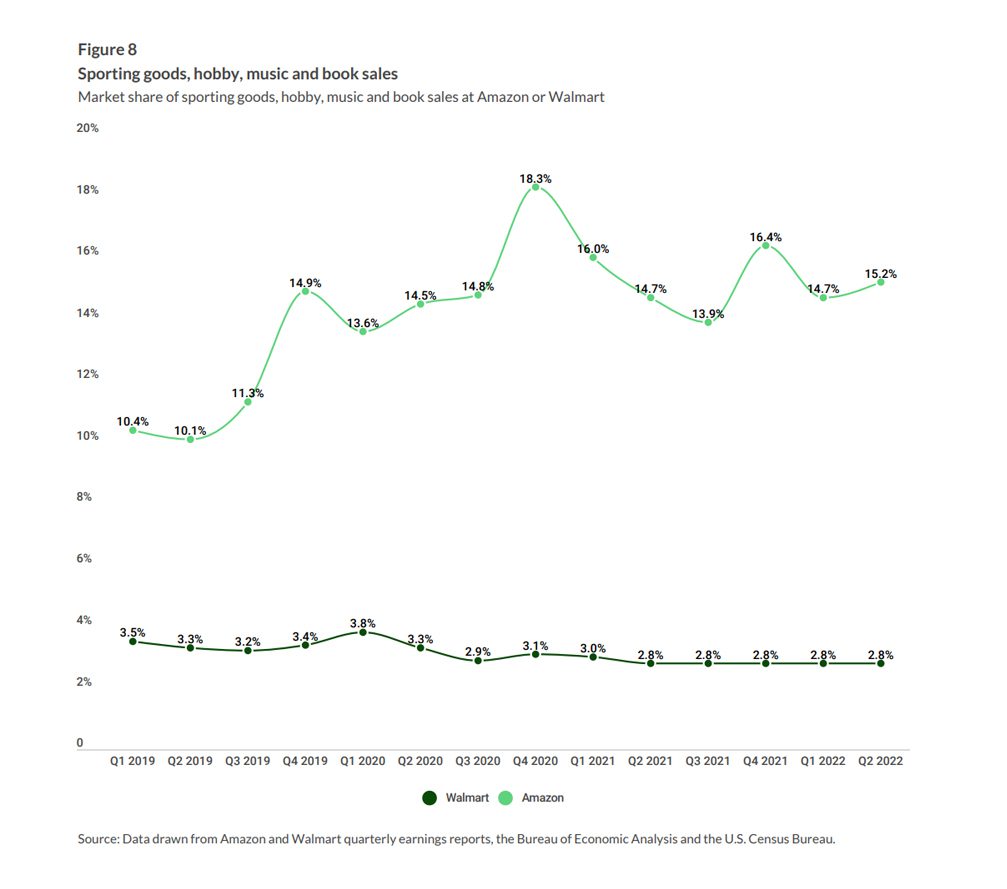

Amazon continues to dominate in the hobbies category, with nearly five times Walmart’s share of books, sporting goods, hobbies and music sales.

In Q1 2019, Amazon’s share of the books, sporting goods, hobbies and music categories was at 10%, while Walmart held only a 3.5% share. Walmart’s trend line has stayed basically flat since then, while Amazon’s share has been on the rise, spiking to 18% in Q4 2020 and 16% in Q4 2021, respectively. Again, these peaks are not surprising, considering consumers’ rush toward online holiday shopping at the height of the pandemic, behavior that continued during the 2021 holiday season.

As of Q4 2022, Amazon holds a 15% share of this segment — a slight increase compared to the same period last year. Walmart seems to be losing ground in this category, as its diminished participation seems to indicate.

Amazon’s long-term advantage in selling books, sporting goods, hobbies and music products has enabled the online giant to fine-tune its user experience. Tapping into a trove of subscriber data, Amazon suggests books and items to consumers based on their interests, an undertaking traditional brick-and-mortar retailers such as Walmart find difficult to achieve.

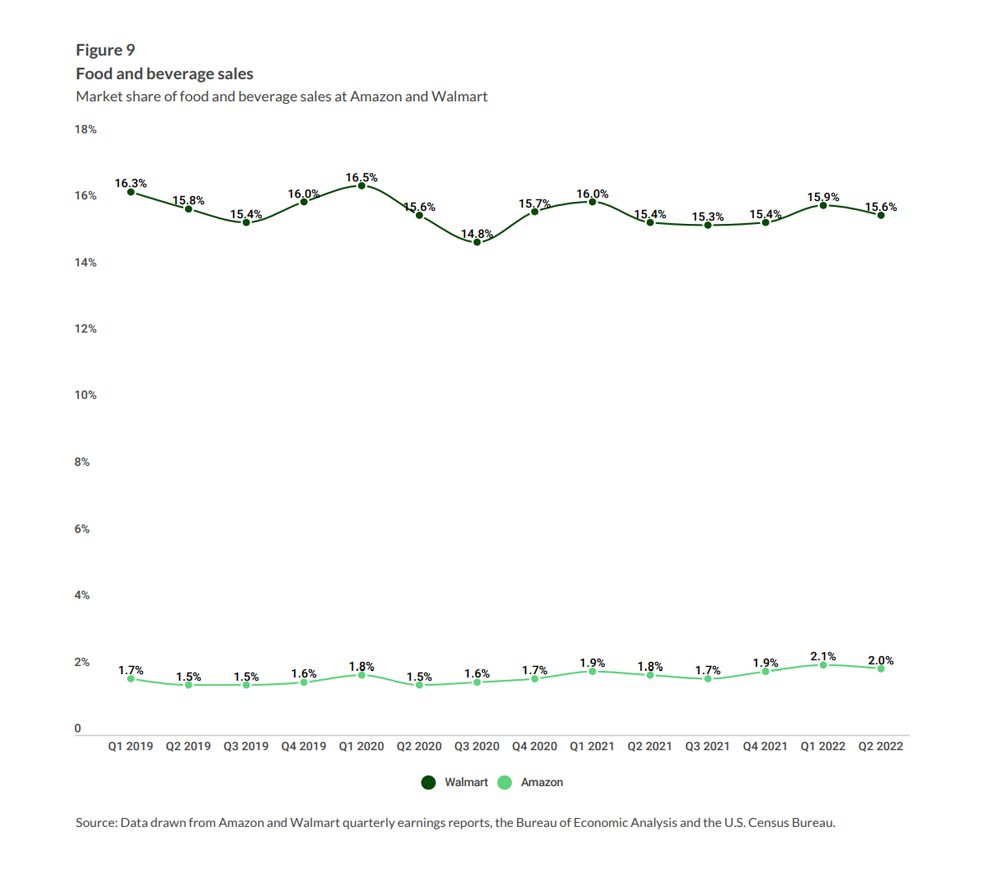

Despite maintaining its hold on the food and beverage market, Walmart’s market share in grocery is slowly eroding, while amazon still holds only a 2% share in Q2 2022, including its sales via Whole Foods Market.

Competing for grocery market share is not as easy as it used to be, with other leaders such as Kroger, Target and Costco taking a bigger slice of sales. As of Q2 2022, Amazon maintains only a 2% share of the food and beverage market, which has not significantly changed since it acquired Whole Foods in 2017. During Q1 2019, Amazon held 1.7% of this market, meaning its share has increased by only 0.3% in the past three years.

Yet, Walmart’s share in this market has been slowly decreasing over the past few quarters. Walmart held 16.3% of the food and beverage segment in Q1 2019; as of Q2 2022, this share had fallen to 15.6%.

Walmart still leads in grocery sales, according to some estimates, with sales of $467 billion in 2021, including more than $73 billion attributed to Sam’s Club, which is wholly owned by Walmart.1 As Kroger, Target and Costco aim to increase their market share, Walmart needs to amplify its leadership in this segment by providing both online ordering and rapid delivery.

Meanwhile, Amazon’s physical store revenue — mainly Whole Foods Market — increased 12.5% in Q2 2022 compared to Q2 2021, and 2.8% compared to the previous quarter. Amazon’s 2021 food sales in the U.S. were over $239 billion, making it the No. 2 retail grocer in the country, outpacing Costco, Kroger and Target.

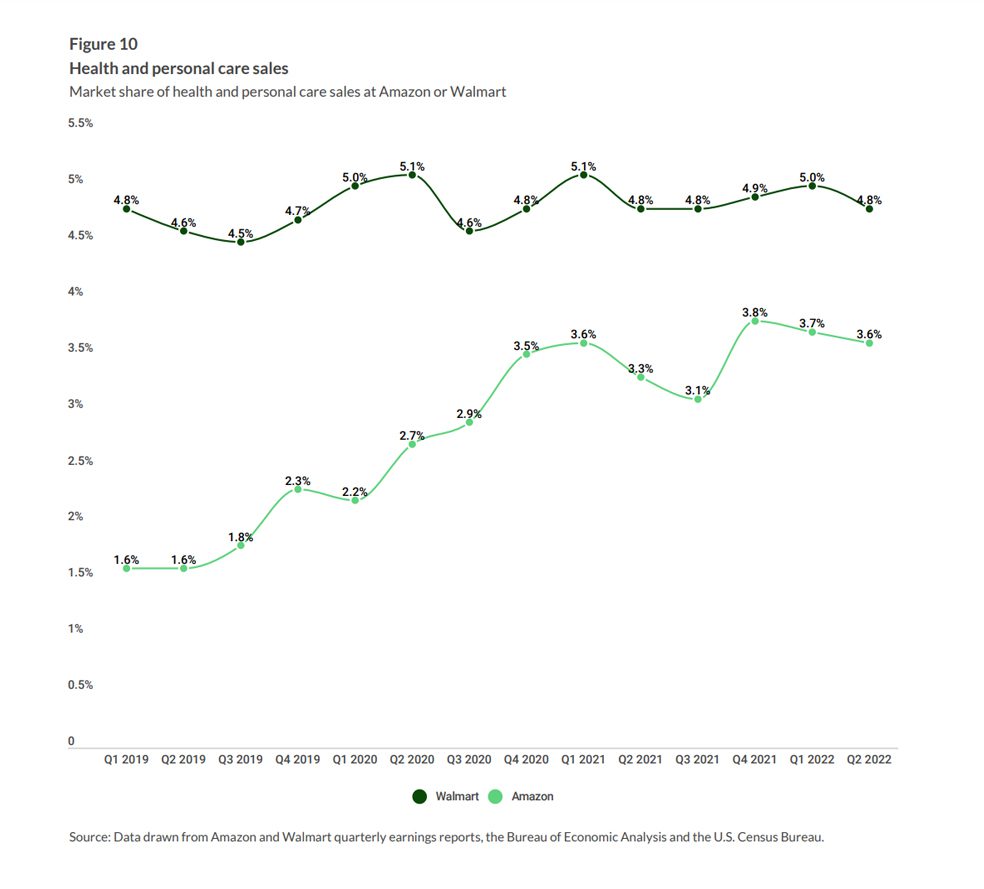

Walmart also has a small lead over Amazon in health and personal care.

Amazon’s pharmacy service launched in 2020, offering a range of over-the-counter personal care products in addition to general goods — but even as it dominates online health and personal care sales, it has yet to overtake Walmart.

While stuck for nearly two years at a market share of less than 4%, Amazon is slowly catching up with Walmart, which has not seen much growth since 2019. As of Q2 2022, Amazon has reached 3.6% of sales, while Walmart still leads at 4.8%.

Amazon and Walmart

By The Numbers

Amazon

Amazon’s gross sales in the United States have increased from $117 billion in Q2 2021 to $131 billion in Q2 2022. This represents a year-over-year increase of 11.5%.

Amazon’s U.S. eCommerce retail sales, excluding Amazon Web Services, have increased from $112.6 billion in Q2 2021 to $126 billion in Q2 2022. This represents a year-over-year increase of 11.8%.

Amazon’s compound annual growth rate (CAGR) for both total sales and eCommerce sales is 31%.

Walmart

Walmart’s gross sales in the United States increased from $118 billion in Q2 2021 to almost $129 billion in Q2 2022. This represents a year-over-year increase of 8.9%.

Walmart’s eCommerce retail sales in the United States have increased from $12.1 billion in Q2 2021 to almost $13.5 billion in Q2 2022. This represents a year-over-year increase of 12%.

Walmart’s CAGR for total sales is 8.1% and is 39% for eCommerce sales.

Conclusion

Top retailers Walmart and Amazon continue to compete head to head in an ever-changing retail marketplace. Amazon rode the online shopping wave as it peaked during the pandemic, yet the retail market soon shifted. As pandemic-related restrictions began to subside, Walmart, like other brick-and-mortar retailers, began to recover some of its lost market share. Even so, driven by convenience and a wider selection, many consumers still flock to online retailers for discretionary, if not essential, items.

With inflation expected to continue for months to come, consumers are looking for low prices and bargains, especially moving into the 2022 holiday season. While Amazon leads in discretionary spending, Walmart, known for lower prices, maintains its lead in grocery and health. Amazon’s huge lead in eCommerce sales is a frontier that Walmart must conquer to grow its market share. As competition intensifies, consumers will benefit — regardless of the winner.