Signs are growing that cryptocurrency is moving into the mainstream, with important implications for other kinds of payments. Its long-term potential to replace cash and checks has been much described, but debit issuers are already seeing opportunity in its rise. Several major card networks have announced plans to issue debit cards that enable users to tap their crypto holdings to pay for everything from jewelry to groceries — as well as convert them into cold, hard cash at the ATM.

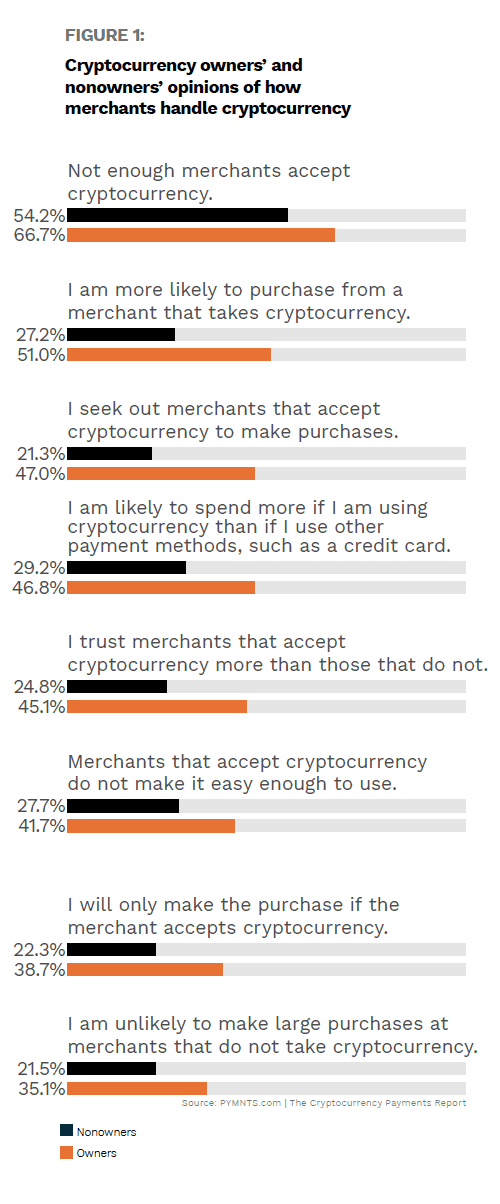

A recent PYMNTS study found that current and former users of cryptocurrency — and even nonusers — are eager to own and use crypto to make purchases, and they are likely to use it for daily shopping as well as expensive purchases. Consumers who use cryptocurrency to buy are highly selective in their choice of merchants, however: 51 percent of crypto owners told PYMNTS they are more likely to purchase from merchants that accept cryptocurrency, and 39 percent insisted they would make purchases exclusively from such merchants. Crypto owners are also likelier to spend more or make large purchases from merchants that accept cryptocurrency, so merchants have a lot to gain in consumer loyalty by accepting crypto payments — particularly if payment processors can support them in this effort.

The biggest challenge with cryptocurrency is its volatility, which has prompted payment networks to take certain precautions, notably to focus only on select cryptocurrencies for stability, such as stablecoins. Stablecoins are digital, meaning that debit payment networks could expect to see a correlated surge in digital debit cards. This Deep Dive explores how the use of cryptocurrency is impacting the debit space and how payment giants can leverage this demand to become consumers’ preferred networks for crypto payments.

The Crypto Payments Surge

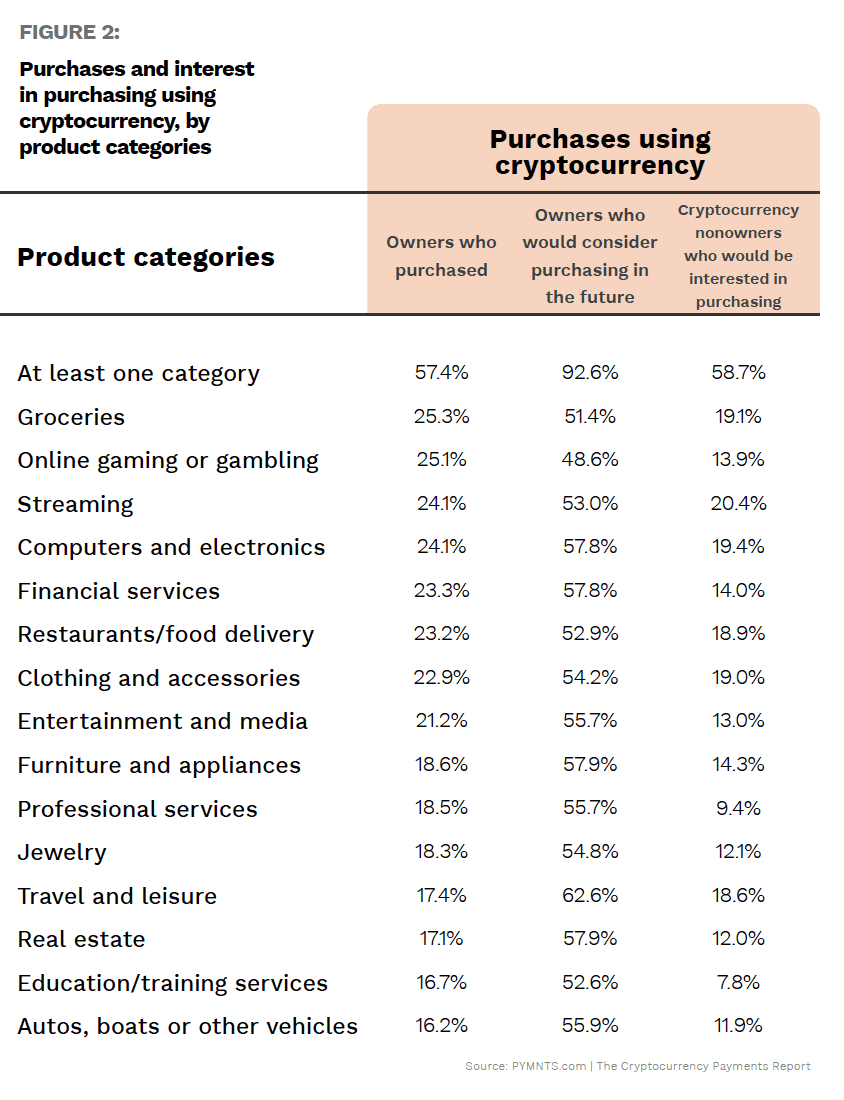

Cryptocurrency is utilized not only to buy other cryptocurrencies: U.S. consumers who used it to make purchases told PYMNTS they used it for gambling (25 percent), restaurants or food delivery (23 percent) and clothing and accessories (23 percent), for example. About a quarter of owners tapped cryptocurrency to purchase groceries and retail products as well as to pay for streaming or financial services, demonstrating the wide range of purchases for which cryptocurrency can be used.

The volatility of bitcoin and other popular cryptocurrencies has been the prime factor in discouraging merchants from investing in crypto payment acceptance. Debit card networks that support cryptocurrency plan to work around this inefficiency by tethering themselves to emerging digital currencies such as central bank digital currency (CBDC), which is issued by a country’s central bank and tied to a nation’s fiat currency, like the dollar, euro or yuan, for example. This eliminates the anonymity and volatility typically experienced with cryptocurrency and makes conversion easier.

This migration to digital assets could significantly alter debit card use, leading to the decline not only of cash and checks but also of physical debit cards as fewer consumers make deposits in their bank accounts and more turn to digital assets or to funds stored in their digital wallets. In turn, this could generate a rise in connected digital debit card use that may push digital debit cards to the forefront of payments. In other words, while usage of physical debit may decline, the enthusiasm for digital debit will likely rise, helped by the connection of debit to digital assets, or CBDCs.

Digital debit could also achieve this potential surge with help from the nearly 2 billion unbanked consumers worldwide, who would have the ability to store their money digitally rather than open a bank account. As more consumers use these digital assets and become familiar with the convenience of digital wallets, they may migrate to digital debit cards over traditional fiat options. This is how the rise of cryptocurrency can help reward banks, payment networks or payment processors that find ways to support this space.

The Debit-Crypto Connection

Some debit card networks are teaming up with cryptocurrency marketplaces to produce their own debit cards that enable users to pay with select cryptocurrencies for everyday purchases. These networks and merchants stand to benefit from supporting such increasingly popular digital assets, as digital debit cards offer reliability and security as well as meeting consumers’ payment flexibility demands.

Expanded payment acceptance opens merchants up to new customers who want to use their cryptocurrency to buy items and also helps build loyalty with existing customers who seek this option. Two-thirds of crypto owners and more than half of nonowners told PYMNTS that there are not enough merchants currently accepting crypto payments, in fact. Almost half — 42 percent — said merchants do not make it easy enough to use either, indicating plenty of room for improvement. Payment networks will also want to monitor transactions for an increase in digital debit usage to develop the right products and partnerships.

Networks and merchants that remain observant of payment trends in the rapidly evolving landscape have nothing to fear from cryptocurrency. Its rise could even represent a high-water mark in the debit arena.