Consumers are carrying the payment habits they developed in 2020 into how they shop in 2021, with the adoption of contactless and mobile payment tools continuing to rise. Many individuals are still leaning on familiar payment tools to make these touchless transactions, with the 2021 Debit Issuers Study conducted by PULSE finding touchless debit card penetration reached 30 percent in 2020. This compares to the 11% penetration such cards showed in 2019.

This indicates debit is still very much a favored payment solution among consumers, but how and where they utilize this method began to shift during the global health crisis as expectations for speed and convenience grew. Consumers are experimenting further with account-to-account (A2A) payment solutions such as peer-to-peer (P2P) apps and mobile wallets that allow them to send or receive funds directly from their bank accounts, for example. A2A payments represent the fastest-growing sector of debit payments, in fact, representing 4% of eCommerce transactions in 2020.

In the latest Next-Gen Debit Tracker®, PYMNTS examines the continued growth of A2A payments, as well as debit’s role as such payments become more popular. It also analyzes why merchants must keep pace with this trend as consumer payment preferences and needs continue to shift.

Around the Next-Gen Debit World

Consumers’ adoption of A2A payment methods has been steadily expanding for years, though many individuals may not be aware this is the case. P2P payment apps fall under this banner, for example, and data from as far back as 2019 found 71% of U.S. consumers were already making transactions using these apps. The global health crisis allowed P2P and mobile wallets to inch further into the payments mainstream, especially as payment providers such as PayPal’s Venmo implemented additional features into their wallets to boost usership. Venmo launched a QR code solution for in-store payments in late 2020, a move that indicates the use of such methods is quickly becoming ubiquitous for consumers. Merchants must be sure they are keeping pace to stay competitive.

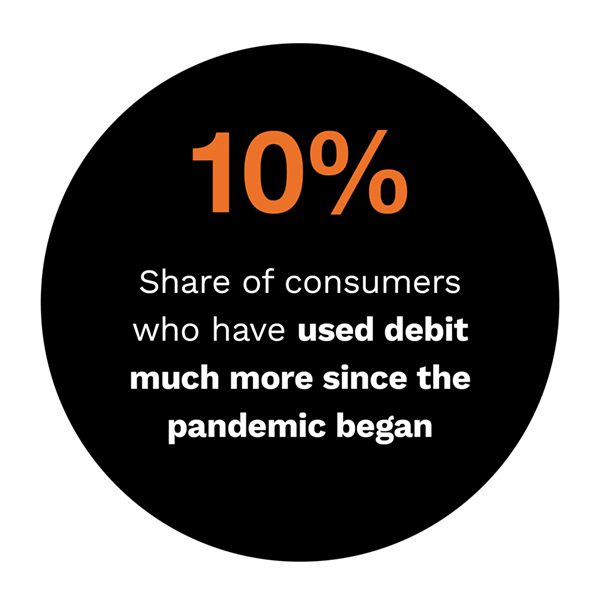

Many consumers may be choosing to underpin their P2P apps with their debit cards, leading to shifts in debit spending patterns. One recent report found that while debit transactions overall decreased from 2019 to 2020, spending on such cards rose 8% year-over-year (YoY). Most importantly, monthly A2A transactions per active debit card expanded by 60% during that same time, with the average cardholder making at least one A2A debit payment per month. This shows both that A2A payments are becoming more popular and that consumers are still using familiar payment methods such as their debit cards, if slightly different from the way they have historically used them to spend.

Expanding adoption of A2A solutions like P2P apps has led payment providers to consider uses for such tools outside of retail and consumer payments. PayPal recently announced it would be partnering with financial services provider Fiserv to allow for the direct deposit of gig workers’ paychecks into their PayPal or Venmo mobile wallets, for one example. This means ad hoc workers such as rideshare or delivery drivers will be able to instantly access and spend their funds, a key benefit for individuals who do not get paid on the same regular schedules as full-time workers. Ninety-four percent of U.S. employees already use direct deposit for their paychecks, and further extending this capability to gig workers or to unbanked consumers who lack traditional bank accounts could provide additional opportunities for financial inclusion.

For more on these and other stories, visit the Tracker’s News & Trends.

How Merchants Can Take Advantage of Rising Consumer A2A Payment Preferences to Grow Loyalty

P2P and mobile wallet tools were already seeing wide adoption prior to the pandemic, but concerns over public health and safety over the past 18 months have led to significant changes to where and how frequently consumers utilize them. P2P apps have become one of the main ways customers purchase groceries or make other daily transactions, putting pressure on both online and brick-and-mortar merchants to keep pace with their growing popularity. The global health crisis has therefore created a surge in interest in P2P and other A2A apps among merchants, explained Hisham Salama, chief digital officer, executive vice president for Bank of the West. To learn more about how P2P adoption has grown and how supporting such payments can provide merchants with an opportunity to expand consumer loyalty, visit the Tracker’s Feature Story.

Deep Dive: How 2020 Drove A2A Payment Adoption Forward and the Key Role Debit is Playing in its Continued Expansion

Consumers’ expectations for faster payments have only risen since the start of the global health crisis. More individuals than ever are adopting payment methods such as mobile wallets that allow them to send funds instantly between bank accounts such as PayPal’s Venmo, a trend that is only likely to continue over the next several years. One recent study predicted consumers will spend almost $1.2 trillion collectively through mobile wallets or P2P tools by the end of 2023, for example. It is critical for merchants to keep up with how consumers — and competing businesses — are utilizing such tools, but this also requires them to understand the payment rails supporting such payments. To learn more about how A2A payment adoption has risen over the past year, how it will grow in the future and the role debit is playing in this expansion, visit the Tracker’s Deep Dive.

About the Tracker

The Next-Gen Debit Tracker®, a collaboration between PYMNTS and PULSE, a Discover company, examines consumers’ changing payment behaviors, the innovations that are reshaping how they use debit and how advanced solutions like machine learning technologies can help financial institutions secure debit payments.