The $4.5 Quadrillion Opportunity in Human Time

Behind almost every great innovation is a story of time.

Maybe an innovation saved a lot of our time. Or it made us live longer. Made us more productive workers who could command a higher premium on our time. Or enabled us to pack more things into the limited time we have. Some innovations have done most of the above.

Innovations in time have massively improved and extended our lives over the last several centuries. And there’s no letting up.

The next wave of disruption will come from those who deliberately innovate around time. Those who see time not as the tick of fixed seconds, but as a human asset whose value has almost unlimited potential.

To find inspiration for the next breakthrough, decacorn, and more, catalysts should study time.

How Time as An Asset Stacks Up

No asset is more valuable, or more limited, than time.

Advertisement: Scroll to Continue

Each day, we get just so much. Twenty-four hours, 1,440 minutes, 86,400 seconds. If we don’t use it, we lose it. So, we try to make the most of it.

To do that, we trade it, swap it and compress it, each day and over our lifetimes.

We can use some of our time endowment to work and make money to buy things. By using our time to learn when we are young, we can earn more money and enjoy our time more when we are older.

Just like people value their houses and businesses value their capital stocks, people value their time.

In the U.S., economic studies find that the average person values their time on earth at around $13 million. That is based on looking at how much people must be paid to take risks that could end their lives. The government uses that figure to evaluate benefits and costs involving lives.

That makes the value of the stock of time for the U.S. population of 340 million people around $4.5 quadrillion (340.1 million people times $13.1 million per life).

By comparison, the U.S. housing stock is worth a measly $55 trillion according to Zillow; the total fixed capital stock was worth $87 trillion in 2024 according to the Bureau of Economic Analysis; and the total value of companies on public exchanges in the U.S. was $68 trillion at the end of September.

A more precise estimate of the value of time would account for the fact that the value of life and life expectancy vary with age. But when you get to quadrillions, who’s really counting?

Governments, businesses and innovators should treat time as what it truly is. A national and global asset.

And like every other great asset, its value can grow through disruptive innovation. The better we use it, the richer the world becomes.

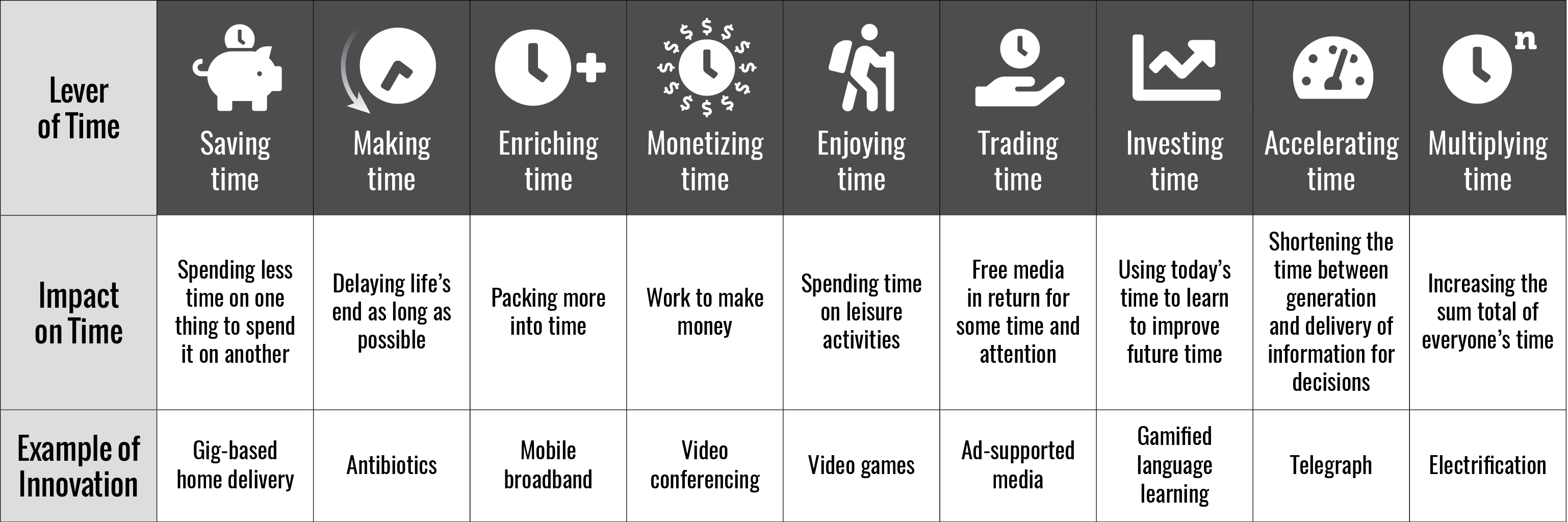

The Nine Levers of Disruptive Time Innovation

Almost 90% of American farms didn’t have electricity as late as 1935. Robert Caro’s famous biography of Lyndon Johnson, “The Path to Power,” shows what that meant to the people living in Hill Country, Texas.

A typical farm family used 40 gallons of water a day. To get it, they had to walk to a well located about 250 feet away with a bucket and carry it back to the house. A federal study found the average family spent about 500 hours a year and walked about 1,750 miles just to get water.

The family devoted even more hours to hauling wood and washing clothes by hand. Tasks that consumed time and strength, especially for women who, literally, carried the heaviest load. More than half suffered physical injuries from the strain of constant standing and physical labor involved in doing both.

Without electricity, there wasn’t much else to do. “No radio; no movies; limited reading—little diversion from the hard day just past and the hard day ahead,” according to Caro. “Living was just drudgery,” one person reminisced.

Electrification changed all that, not just in Hill Country, but throughout the U.S. and eventually most of the world. People had more time. And more to do with that time. They could also expect to live longer as electrification reduced infant and adult mortality.

Disruptive innovations can make time far more valuable.

Entrepreneurs, innovators, businesses and governments have nine levers to find the next big thing in time.

1. Saving Time: Spending less time on one thing so you can spend it on another.

Millennia ago, people learned to domesticate horses, which reduced the time spent traveling. Running water from electric pumps likely saved all 500 of those family hours fetching water. The invention of the washing machine reduced the amount of homemaker time to do a load of laundry from 4 hours to 41 minutes. E-commerce companies, from online retailers to meal delivery services, save people the time from traveling to and from physical locations or from cooking their own meals.

2. Making Time. Delaying the Grim Reaper’s visit as long as possible.

Innovations like indoor plumbing created cleaner water and prevented the spread of disease. Vaccines largely ended many deadly diseases. The development of antibiotics saved lives. Surgical advances, imaging innovations, and drug development do too.

Saving lives means extending the amount of time people have.

Globally, average life expectancy increased from 32 years in 1900 to 73 years in 2023, more than doubling the amount of time people have. In the U.S., life expectancy increased from about 50 to almost 80.

A perfect human specimen, with the best circumstances and the greatest luck, could make it until 125 based on the upper range for demographic studies. Using that data, in the U.S., we’ve reached only 64% of our potential.

3. Enriching Time. Packing more into the time you have.

Electrification expanded the portion of the day people had light. That gave them more time to read and do things that are impossible to do in the dark. The printing press, and communication technologies from the telegraph to radio to broadband, have expanded the ability to benefit from our auditory and visual senses. Smartphones, powered by fast cellular, make those experiences on the go and on demand.

Today we can listen to an audiobook, a podcast, or the radio while we’re driving, taking the subway or vacuuming the floors.

4. Monetizing Time. Using time to work to make money for people and their families.

Innovations can change the amount of time people work. The time people spend working depends on whether they participate in the labor force, how many hours they work, and when they decide to retire. People can then use that money to buy goods and services, which they combine with their time (think about eating) to create value.

The labor force participation of women has increased in the last century in part because household chores, which disproportionately fell on them, took up less time. People can work later in life because they are healthier and have more years available to them. Platforms make it possible for people to pick up gig jobs, participate in side hustles and work-from-home using their available time.

Innovations often result in people being paid more because they are more productive. With higher incomes and savings, people can decide to work less and retire earlier, with greater incomes and more wealth.

5. Enjoying Time. Spending more time on leisure activities.

The disruptive innovations for time saving and improving innovations have made leisure cheaper, because less time is needed for household chores, and more valuable, because sensory-related innovations provide better ways to spend their time.

In 2024, the average American, age 15 and over, spent an average of 5.5 hours a day “in some sort of leisure and sport activity, such as watching TV, socializing, or exercising.” That’s about 37% of waking hours (the average number of hours sleeping was 9.0 hours).

An economic study found that adults spent 6.75 more fewer hours a week working for pay or at home, and instead on leisure activities, between 1965 and 2003. This time was worth roughly 8% to 9% of GDP based on how much people could have made from paid work

6. Trading Time. Giving people things for free, or at a discount, in return for them giving some of their attention.

Since newspapers were first invented, advertisers have been paying for people to pay attention to them. The idea is simple: advertisers buy space in media, hoping that audiences will notice their ads. People might not enjoy the ads, but they do enjoy the content. In exchange for free or cheaper access to that content, they let advertisers try to capture some of their attention.

New media innovations have always created huge value by making leisure more enjoyable. Families in places like Hill Country, for instance, could spend hours listening to the radio or watching TV, paying nothing beyond the cost of the equipment and electricity.

My 2020 paper on attention markets estimated that Americans spent about 500 billion hours consuming ad-supported content in 2019. That made the content they were consuming worth roughly $7 trillion, given the opportunity cost of their time.

7. Investing Time. Using time to learn and thereby increasing the value of time later in life.

People, in most developed countries, invest a large part of their time through their teens, and often beyond, learning. This increases the value of their time, for working and themselves, later in their lives.

A 2020 U.S. study by Fed economists found that kids, from kindergarten through high school, spent 36% of their waking hours over the week on class time and enrichment activities, including homework. (The data are from 1997, 2002, and 2007.)

Investing in time differs in two main ways from the other levers of innovation.

It’s not like choosing to watch TV, clean the house, or pick up hours with side hustles. In the U.S., and many countries, kids are compelled to invest time in learning by the government and by their parents. The logic is that it’s good for the kids and good for the country.

Education hasn’t had a true disruption in centuries. Public schooling and standardized curricula were the last big innovations, and online learning has yet to deliver on its promise, with the exception of foreign languages.

In 2024, grade 12 reading scores in the U.S. were the worst in three decades and math scores the lowest since 2005.

8. Accelerating Time. Shortening the time between the generation and delivery of information.

People can make more and better decisions when they get information more quickly. Disruptive innovations have sharply decreased the time needed to convey information and, therefore, the choices people can make at any moment in time.

Cheaper paper helped transmit information easily over long distances. The speed increased with the development of horse-based delivery services. In the U.S., sending mail on the stagecoach took weeks. The short-lived specialty Pony Express could move mail in days. It was replaced with the telegraph, which was nearly instantaneous aside from going to telegraph offices to send and retrieve messages.

Economists have examined the value of faster time in commerce. Before the successful launch of the transatlantic telegraph on July 28, 1866, it took 7 to 16 days to send information between the U.S. and Great Britain. It was almost immediate after that.

The faster transmittal times reduced the price spread for cotton between New York and Liverpool by 35%. By reducing price distortions, it resulted in economic efficiencies that were worth about 8.4% of the value of the exports.

Of course, the internet and related communication technologies have massively accelerated time.

Now it can take just a few seconds to buy from sellers around the world, to take just one example.

9. Multiplying Time. Increasing the total of the collective hours of everyone’s time, including their working time.

Setting the warm and fuzzies aside, societies depend on the collective hours people spend working, creating, and paying taxes. People make the goods and services we consume or trade with other countries. People come up with the ideas that power innovation. And workers ultimately pay most of the taxes to finance everything from national defense to basic research to social welfare.

Europe now faces an “existential crisis” in part because people work fewer hours and have fewer children, who will supply working time in the future. Most developed countries have increasingly severe time shortages and will eventually face crises too.

Countries can multiply time by encouraging later retirement, higher workforce participation, longer hours, and immigration. The eight other innovations in time are important drivers. Countries can also try to encourage families to have more babies, but there’s not much evidence that works.

Advanced applications of artificial intelligence might be the disruptive innovation we need to solve the great time shortage: it could create human substitutes and increase the productivity of human working time. We’re not ready to count humans out, though.

Making a Fortune from Time

Entrepreneurs, innovators and investors searching for their next breakthrough should treat time as a resource class: measurable, improvable and ripe for disruption. That goes for governments, too.

The addressable market isn’t literally $4.5 quadrillion. But that is a proxy for the enormous potential of the nine levers to innovate time. And how even small gains in how we create, extend, or enhance it can generate enormous economic returns.

Economists have developed clever data-driven methods for estimating the value that people place on their time that can help size investment opportunities and ROIs.

When Time Is Literally Money

We have put rigor into the old saying that “time is money.”

Economists look at how much people have to be paid to give up time, say, for work. Or how much people will pay to save time, like for a faster commute. These aren’t ivory-tower exercises. They drive federal cost-benefit analysis of proposed investments.

The simplest approach is based on wages. A person could go to the beach or do some chores around the house instead of working another hour.

If they are willing to take $20 to work an extra hour for a gig job, then that must be more than the value of an hour doing something else. The wage-hour tradeoff is hard to pin down in practice because many people have fixed salaries or must work a set number of hours. But the after-average after-tax wage, about $17.83 now, turns out to be a good proxy for the value of time for the average person.

Instacart claimed it saved people more than 700 million hours between 2012 and 2023 because they didn’t have to go to the grocery store. At $17.83 an hour, it saved people more than $1.2B.

The value of time depends on the situation. An hour of work may be more or less pleasant. The time spent on a subway ride isn’t as costly if a person can listen to music on their smartphone. People hate standing in line at checkout, which is why many opt not to and order things online.

To get context-specific estimates, economists conduct surveys that try to get people to reveal how much they value time spent in various activities. The U.S. Department of Transportation used these surveys to value savings in local personal travel at about $12.50 an hour. Recent studies estimate the value of spending time using social media. They find that you would have to pay people a lot to go without.

The Longevity and Money Tradeoff

Economists have also developed data-driven methods for putting a dollar value on extending life.

People make many decisions that result in small changes in the probability of their dying. Many involve making tradeoffs between money and risk: paying extra for a safe car with lower fatality rates in crashes or taking a job that pays more but poses a great risk of a fatal accident. People don’t act as if their lives are worth an infinite amount of money.

Most of the studies, and the most robust, look at job decisions.

A review, based on 2017 data, found that an employer would have to pay a typical worker another $100 a year to take a job where 1 in 100,000 workers die from a work-related injury. To summarize these results, economists calculate the “value of a statistical life” as the total amount of money that a group of people would pay to avoid one death: 100,000 people would pay $10 million to save one life.

The federal government uses this approach to estimate the benefit of investments in activities that could save or cost lives. They currently adopt the $13.1 million per life figure I used earlier. Economists have found that this figure varies across ages. Younger people have more years to value than older people.

Economists also use this approach to value innovations in healthcare.

A seminal economic study found that the increase in life expectancy between 1970 and 2000 “added about $3.2 trillion to national wealth per year, an uncounted value equal to half of average annual GDP over the period.”

Not surprisingly, AI innovators are chasing improvements in healthcare.

There’s Clock Time, Then There’s Brain Time

The real frontier of time isn’t just looking at a clock. It’s looking inside the brain, too.

If you buy the Audible version, you can listen to my book, “Matchmakers,” with Richard Schmalensee. It will take you 6 hours and 53 minutes. We were surprised at how many people chose to do that.

But the thing about audiobooks is that you can do lots of other things while you are listening. One survey found that 70% of listeners multitasked. A different survey found that 74% of audiobook listeners listen while driving. People also listen while engaging in lots of other activities, like running or doing household chores.

They are packing more things into their heads at the same time.

Lots of other time innovations do the same.

When we talk about people’s time, we’re really talking about the mental processes that happen within a unit of time. What people do with their brains to consume media, work, learn, view ads and more.

Economists and psychologists call these processes “attention.” That term covers what regular people call attention, but much more. (An excellent recent survey has the details.)

Like money, attention is limited. Using it for one thing means giving it up for another. But unlike money, it’s powered by cognition and choice, and we can decide to engage in more mental activity. We decide what to do with our brains and senses and then do it.

We can think of human time along two dimensions.

One is clock time, the steady march of seconds. The other is attention per unit of time, which is the variable flow of mental energy that determines how much we accomplish within those seconds. (This is a simplification since attention has many dimensions itself.)

Brain time is the flow of attention through the flow of time.

This is where the nine levers of time innovation create immense value. Some of those levers give us more clock time, while others enrich attention. Often, they do both. And the beauty of brain time is that multiple levers can be processed during the same unit of time.

Clever innovators can make a lot of money from brain time.

Google search saved people clock time from going to the library and on other resources to get information. People could even listen to loud music or talk to their colleagues without getting yelled at by the librarian, which enriched their attention.

People ended up spending a lot of time doing search queries and looking at search results pages. And they didn’t have to pay a penny.

Google built its business on selling slivers of brain time to advertisers. Advertisers can put an ad on the page and have a chance that some people will pay attention.

With Facebook and a smartphone, people could interact with friends anywhere anytime, including while watching TV or on the treadmill.

Alphabet and Meta are worth about $5 trillion. They make almost all their revenue from the small percentage of visitors who divert brain time to ads.

It’s About Time

Focusing on time as an improvable asset, and the nine levers for increasing its value, gives entrepreneurs, innovators and businesses a rigorous, disciplined way to identify and size opportunities. It also hands governments a guide to make investments that will maximize the value of human time.

The economics of brain time provides a new lens to help shape the innovations and value their potential.

Some economists say the era of unprecedented growth has come to an end. After all, it’s hard to top indoor plumbing.

I don’t think it’s over.

The potential to improve and extend human time is enormous. The financial incentives are powerful. And AI and other new technologies provide the foundation for new leaps forward.

It’s about time.

David S. Evans is an economist who has published more than 10 books and 200 articles, many related to entrepreneurship, platforms, the digital economy, and competition policy. He is the chairman and co-founder of Market Platform Dynamics. He has taught at the University College London and the University of Chicago Law School. For more details, see davidsevans.org. This article is part of Evans’ Catalyst Series and extends insights developed in his book Catalyst Code: The Strategies of the World’s Most Dynamic Companies, co-authored with Richard Schmalensee.