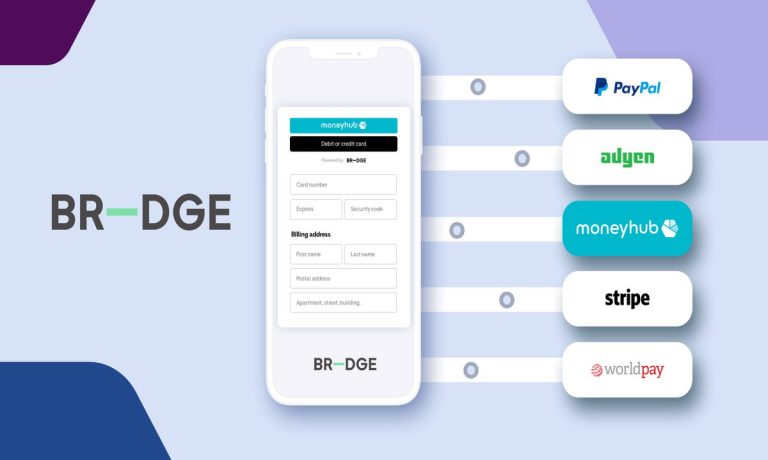

According to the two companies, BR-DGE will integrate Moneyhub’s open banking tech into its platform, which offers one point of integration for several payment options.

“This means merchants no longer need to pick and choose between one or two payment providers at great cost and administrative burden,” the companies said in a news release. “Offering greater choice and flexibility for merchants also increases the likelihood of payment success due to removing over reliance on a small number of payment providers.”

Meanwhile, merchants using BR-DGE can offer customers open banking as a payment method, allowing them to transfer funds straight from their bank to the merchant’s bank account instead of needing to use a card or going through PayPal.

The companies say open banking benefits both merchants and consumers by offering lower card transaction fees, instant payment settlements and increased security. Customers can make payments knowing their cards are protected, while merchants can take advantage of the strong customer authentication (SCA) compliant payment option.

“Providing access to a world of traditional and innovative payment solutions through the click of a button is the future of payments,” said Brian Coburn, CEO at BR-DGE. “Offering open banking as part of this is a key piece of this puzzle.”

Advertisement: Scroll to Continue

Coburn also notes that his company believes “the scale and impact of failed payments has largely been brushed under the carpet.”

Added Moneyhub CEO Sam Seaton: “Both merchants and consumers have so much to gain from bank-to-bank payments — security, speed, efficiency and cost. Scaling up payments is a truly vital task, and partnering with BR-DGE further enhances consumer options.”

Read more: The Days of Manual Credit Card Reconciliation Processes Are Numbered

PYMNTS spoke to Seaton last week about the reluctance some companies show in giving up their manual processes of digital reconciliation. She attributed this in part to lack of awareness of open banking’s capabilities, but also the time and effort needed to change existing and entrenched operation methods.

“We also mustn’t forget that people worry they or their entire departments might lose their jobs, [and] on top of that, people don’t like change,” she noted.