Digital-first businesses were better equipped to take advantage of new market opportunities unleashed during the pandemic. In the past year, 92% of consumers made an online purchase, while 85% performed banking activities online, according to PYMNTS research. In this rapidly evolving digital environment, banks are pressed to adopt technology with a digital-first and consumer-centric mindset. They need to meet customer expectations for secure access to basic services such as making money transfers via multiple digital and mobile channels.

In the December edition of the “AML/KYC Tracker®,” PYMNTS explores how anti-money laundering (AML)/know your customer (KYC) compliance requirements are changing with consumers growing use of digital banking services and how adopting biometrics, artificial intelligence (AI) and machine learning (ML) technologies are helping banks to remain AML/KYC compliant and keep customers secure.

Around the AML/KYC Space

Hong Kong’s banking regulator has levied a total of $5.7 million in fines on four banks — including local branches of Industrial and Commercial Bank of China and UBS — for non-compliance to AML rules. According to a statement from the Hong Kong Monetary Authority (HKMA), they failed to use appropriate AML measures for customer due diligence.

The Financial Crimes Enforcement Network (FinCEN) has released a list of its top priorities in fighting money laundering and the financing of terrorism. These priorities highlight the most prominent threats to the United States, including corruption, cybercrime, domestic and international terrorist financing, fraud, transnational criminal organizations, drug trafficking organizations and proliferation financing.

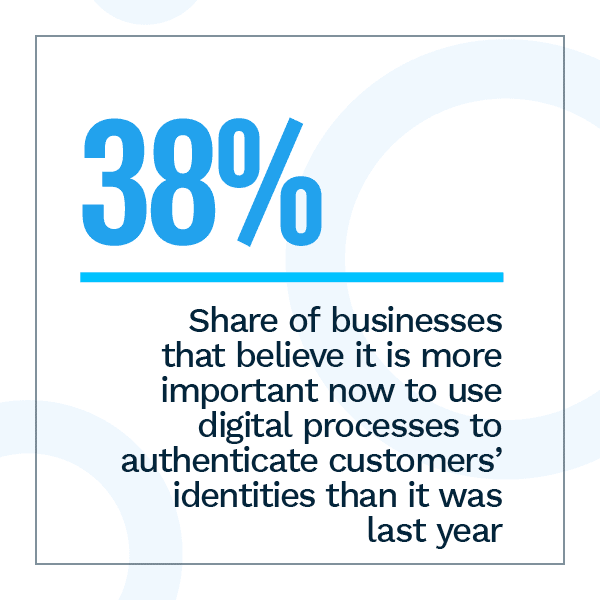

As the number of consumers onboarded remotely grows, so does financial crime, making digital identity verification crucial. Fraudsters are adopting more sophisticated scams, such as impersonating a business, which requires an upgrade in digital AML and KYC solutions. Financial institutions (FIs) are also scrambling to keep up with current AML/KYC requirements, a mandate made more urgent by the European Union’s sixth AML directive combined with stricter regulations in the U.S.

For more on these stories and other AML/KYC headlines, check out the Tracker’s News and Trends section.

Upgrade on How FIs and FinTechs Can Leverage Data-Centric AML/KYC Compliance to Secure Digital Banking

New security concerns include greater risks for identity theft and online fraud, as in-person onboarding procedures and account access give way to digital transactions.

In this month’s Feature Story, Upgrade Chief Risk and Compliance Officer Tom Curran explains how FIs and FinTechs can comply with AML/KYC regulatory requirements while ensuring customers have a frictionless digital banking experience.

Deep Dive: How AML/KYC Measures Are Evolving With Digital Banking’s Growth

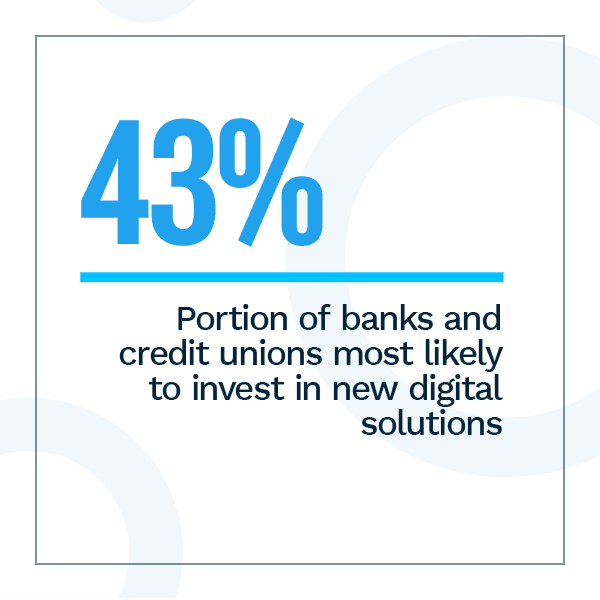

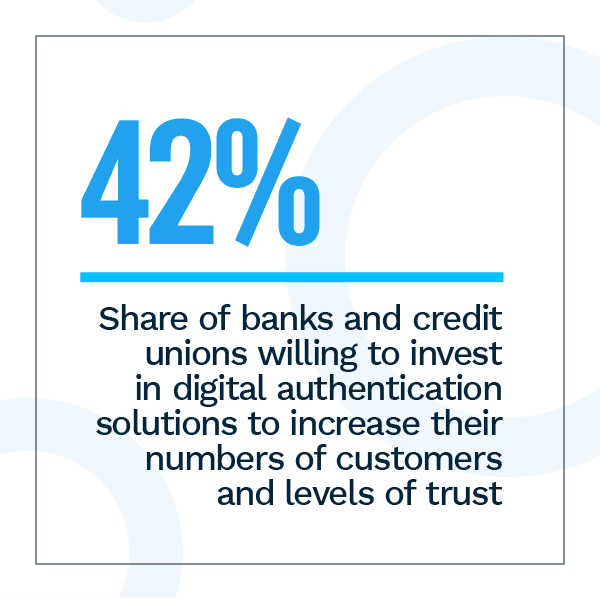

FIs are pressed to provide digitally-savvy consumers with convenient, streamlined and interactive digital banking experiences while keeping personal information secure.

This month’s Deep Dive explores the challenges FIs face in meeting AML/KYC regulatory requirements as digital banking becomes more popular and how investing in AI and ML technologies can help banks remain AML/KYC compliant and keep their customers safe from online threats.

About the Tracker

The “AML/KYC Tracker®,” a PYMNTS and Trulioo collaboration, provides an in-depth examination of current efforts to stop money laundering, fight fraud and improve customer identity authentication in the financial services space.