How Apple Can Reverse Their Revenue Curse

Not many companies can lay claim to losing as much value in 12 months as the entire market cap of the world’s largest retailer and still remain standing. But that’s exactly what’s happened to Apple over the last 12 months.

Apple has subtracted $234 billion from its market cap – about $20 billion more than Walmart is worth.

With a market cap today of $502 billion, Apple’s clearly no slouch either. But instead of talking about its potential to become the first trillion-dollar company, the conversation has suddenly shifted to Apple’s next act – and how it will keep its mojo moving along in a post-Jobs world.

I laid out my thesis last week, with respect to Apple’s struggles, by giving you my take on why Apple seems to now play fast and loose with the numbers.

Mostly because the Apple story over the last year isn’t all that great.

iPhone unit sales – down 16.3 percent.

Advertisement: Scroll to Continue

iPhone revenue – $7.4 billion less in 2016 Q1 than 2015 Q1.

iPad sales – down 18.7 percent.

Overall, the sales of Apple’s flagship products, all products sprung from the genius of Steve Jobs, are down 17.4 percent.

The growth engine that Apple imagined would be China is also tubing – down 25.8 percent or $4.3 billion. This, along with the Chinese government’s decision to shut down iTunes and iBooks caused Carl Icahn to sell every last one of his 46 million shares in a down market. And prompt Tim Cook to fire up the corporate jet and pay a visit to Chinese President Xi.

The other growth engine – services – that everyone touted as “promising” really wasn’t all that great either. Yes, Tim Cook reported that Apple Services posted a 19.9 percent increase from 2015 Q1 to 2016 Q1 with an extra billion in revenue quarter over quarter. But he glossed over the fact that 50 percent of that revenue was thanks to a one time patent settlement with Samsung.

Promising? Maybe not – at least not this quarter.

So what’s an Apple to do?

It’s tough. Their margin comes from the sale of devices. iPhone 6 was a home run, until it wasn’t. People are holding onto their phones longer and there has to be a real “WOW” factor for people to trade their $600+ phones in every year or two – even with the Apple installment plan. For anyone who bought an iPhone 6 two years ago to think about buying an iPhone 7, it needs to do something hugely different than what is available via a software upgrade.

And Apple learned with Apple Pay, how hard that is to do. And with Apple TV how hard it is to make all the content providers toe the line.

The hill that they have to climb every year, year in and year out is slaying it with new versions of the iPhone.

Unless they find new ways to make up the difference.

And here are a few of the ideas that I’d be kicking around if I were in Mr. Cook’s shoes.

MAKING APPS (REALLY) PAY

Everyone knows that Apple controls a massive apps ecosystem. More than 1.5 million apps are in its Apps Store, which have been downloaded more than 100 billion times since it launched in 2008. Last year, App Annie reported that even though Google Play had twice as many downloads as Apple did, (200 million to 100 million) Apple racks up 75 percent more in sales. Developers like the Apple platform for that reason: they stand a better chance of making money.

That means that even though most apps are free and ad supported, more of those that aren’t are downloaded by people with iPhones willing (and able) to pay a few bucks for a premium version of their favorite (gaming, weather, business) app.

We also know a couple of other things about apps and how people use them.

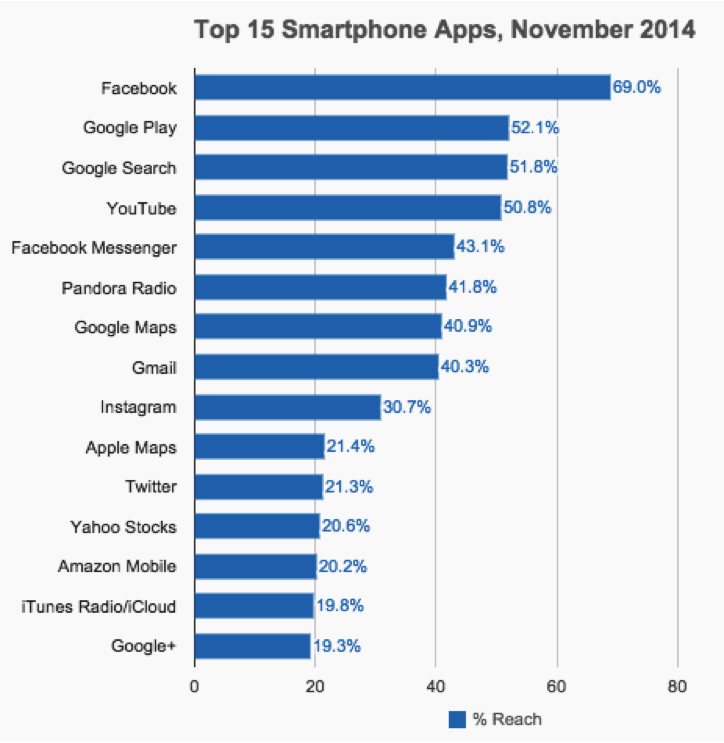

Apple said that last year, on average, iPhone users download 119 apps. The latest Nielsen study tells us that most people only use 27 of them – and concentrate 80 percent of their activity in five – Facebook, Google Play, Google Search, YouTube and Messenger.

The 27 that people tend to use are those that are also aligned with routine activities – and in some cases are also daily habits – such as checking email, the weather and stock prices, tracking bank transactions, downloading boarding passes, getting the news, paying for coffee, ordering an Uber, finding places to eat and making a reservation.

The 27 that people tend to use are those that are also aligned with routine activities – and in some cases are also daily habits – such as checking email, the weather and stock prices, tracking bank transactions, downloading boarding passes, getting the news, paying for coffee, ordering an Uber, finding places to eat and making a reservation.

And, of course, social activities like checking Facebook, posting pics to Instagram, texting, etc.

At the moment, Apple only monetizes digital apps – taking 30 percent of the sale of games, digital content, photos, etc.

But there’s nothing stopping Apple from deciding that the quickest path to filling their very large market cap hole is by taking a small piece of the apps in their very large apps ecosystem.

One possibility is that every time someone orders an Uber, uses their Starbucks or Dunkin’ app to pay for coffee and a jelly donut, orders a Domino’s pizza with extra pepperoni from their app, buys something from eBay, Amazon or Walmart.com, booked a hotel room via the Hotels.com app, bought a round trip ticket to Cupertino from the American Airlines app, Apple could decide that it would like a piece of those transactions. Just like it did when it launched Apple Pay. The big difference though is that unlike Apple Pay, consumers actually use these apps and conduct commerce using them.

Take Uber for example. They had about $11 billion in revenue in 2015 that occurred on apps on either Apple or Android devices.

Let’s say Apple wanted to be nice and only charge 1 percent — instead of the 30 percent it charges digital apps — for using its wonderful device and app store. That would be a cool $50 million a year just from Uber and all pure profit.

A few more of those, if Apple could get away with it, would go a long way to filling the revenue gap and boosting market cap.

But that’s just one scenario.

WHY NOT CHARGE AN ENTRANCE FEE?

Suppose Apple charged every app just for being part of the app ecosystem. So, Facebook, Messenger, OpenTable, The Weather Channel, banking apps, third party wallets like PayPal – any and all apps — just for the ability to be in an ecosystem that’s used by people who have the potential to drive revenue their way.

For example, Facebook reported just last week that consumers are now spending nearly an hour a day on their platform – which is of course, on the home screen of hundreds of millions of people’s iPhones. Facebook has worked diligently over the last several years to be much more than just the place where people keep in touch with their friends. It’s increasingly where people get news, discover new products, and even buy stuff.

Suppose Apple decided that it was going to charge Facebook for taking up residence on the consumer’s home screen? Apple, today, decides who gets real estate on their phone. Ever wonder why you don’t get junky apps on the iPhone like you see on Android phones, including ones from the carrier that provides the service? Apple said they couldn’t be there. Wonder why you can’t delete Wallet or Music – even if you can’t or don’t use it? Apple has decided that, too.

So, they could just as easily decide that to be on the home screen, apps need to pay up even if they aren’t directly making money like Pandora does. Here’s a calculation for you. In 2016 Q1 Facebook earned $4.2 billion in mobile ad revenue. Let’s suppose half of that was on Apple devices, which is likely. That’s $2.1 billion and annualized it’s about $10 billion. Let’s suppose Apple insisted on a per user charge that added up to $500 million. Would Facebook blink? Maybe not — and if everyone was paying the tax, they would all just pass it on to advertisers. After all, Apple charges Google about $1 billion to be the main search partner for the iPhone.

Perhaps Apple could decide to be less obvious and start charging for other things – like having access to its toolkits each time there is an upgrade for the more established apps like Amazon and Facebook. Or for preferred placement in the Apps Store. It’s rumored that Apple will add search to its App Store. With that search, may also come the opportunity for Apple to monetize preferred placement, like Google does with AdWords.

And given the heavy dependency that all of these apps have on being accessible within the Apple ecosystem, there wouldn’t be much any of them could do but pay the tariff. At least in the short term and probably in the long term as well, unless Android really improves its app game and gets a lot better clientele.

The apps at greatest risk of being charged, of course, are those where consumers spend most of their time and use the most as part of their daily routines – Facebook, Google Play, YouTube, Messenger — or spend the most money with – eBay, Amazon and Walmart on the retail side.

Of course, these are also the same players that have options of their own to pursue.

BUT LOTS OF THE BIG GUYS HAVE OPTIONS

Facebook could decide to get into the devices business too and fork the Android operating system just like Amazon has done. It could create its own app store. Facebook, by the way, just hired a hardware expert from Google, which makes you wonder if they might be thinking along these same lines too. On that phone would be Messenger, with its own commerce engine, Instagram and WhatsApp. With 1.5 billion people coming to Facebook each month, 900 million to Messenger, 800 million to WhatsApp and 400 million to Instagram, who knows, Facebook could become the hot new mobile ecosystem.

Then there’s Amazon.

The Fire Phone was a big bust. Amazon decided that it wanted to create a forked version of Android and force developers to write apps to it. The classic chicken and egg dilemma revved into high gear. No consumers, not a whole lot of developer interest. No developer interest, not a lot of consumer appetite for the phone. But it’s early days, and one bust doesn’t mean that Amazon is out of the game.

Because Amazon is still very much in the ecosystem business. It’s got a content ecosystem with its streaming media platform, a marketplace ecosystem that includes Amazon and multiple third parties, a B2B ecosystem that’s driven $1 billion in sales between buyers and sellers, a device ecosystem with Echo, Dot, Dash, and a software and AI ecosystem with Alexa and the Dash Replenishment Services and a logistics system that enables the efficient delivery of products purchased.

Amazon seems pretty focused on reinventing commerce, never mind retail. Today its marketplace drives about 50 percent of all products sold, and some estimate 20 percent of its revenue. But it seems to be thinking about marketplaces in a very different way – by enabling commerce using a consumer’s Amazon’s credentials on other sites that provide access to a curated collection of goods and services. Its latest tie up with Moda Operandi – a designer marketplace – makes it possible for a consumer to access that site and pay with her Amazon credentials in one click is an example of how Amazon is stretching the definition of “marketplace.”

Alexa is leveraging the power of voice to enable contextual and conversational commerce to happen. Now totally unbundled from the Echo device, Alexa is using the power of AI and voice to contextualize data that is input into apps or via the Web via any device. As commerce expands to a variety of endpoints in the home, the office, the car and on mobile devices, Amazon could redefine ecosystems and apps and devices to access both.

Google could just keep on keepin’ on, doubling down on making all handset manufacturers their BFFs, including persuading Samsung to ditch its own OS. The appeal of Apple is the status associated with owning an Apple device – it’s why China is so attractive. But there’s nothing like the thought of making less money on Apple via an Apple tariff for apps and developers to decide that a spiffy new [Fill in the blank brand of] handset that provides access to the apps they want to use is all they want and need.

And for Google and retail, a potentially extra value add to pursue. Google Search may in fact be the most powerful app around.

THE APP AND THE ECOSYSTEM MAY NOT RULE THEM ALL

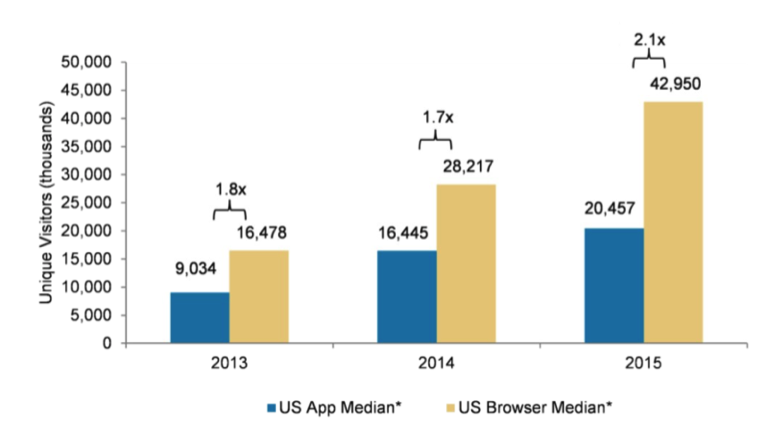

Despite what Apple would like to be the reality, according to research done by Morgan Stanley, the mobile browser audience is anything but declining – in fact it’s growing, on average, two times faster than app audiences across the Top 50 mobile Web properties that they examined.

Where this is most relevant is retail, where the browser/app divide is most stark – and for the obvious reason.

Where this is most relevant is retail, where the browser/app divide is most stark – and for the obvious reason.

Consumers may download the Walmart, Amazon or Target app because they use them the most, but most consumers shop at many more stores, or at least want to browse at more than just those three. For a consumer who is looking for “black linen dress, bracelet sleeves,” she’ll pop over to Google to search since it gives her the entire world to search from.

The Morgan Stanley data supports that, too. Ninety-five percent of the mobile traffic to retail sites is being driven by the mobile browser – not apps – and browser audiences are six times larger than app audiences.

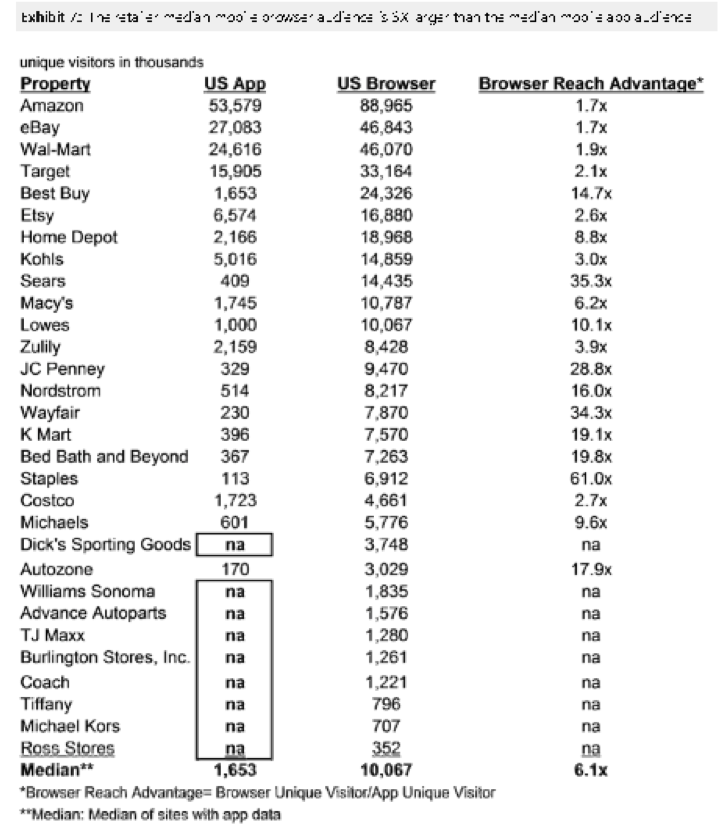

Take a look at this chart. Even the big guys like Nordstrom, Macy’ s, Kohl’s, and Staples — who recognize that mobile is what’s driving their traffic and sales — are getting that traffic via the mobile browser, either because the consumer typed in the name of the store or a product and found her way there.

s, Kohl’s, and Staples — who recognize that mobile is what’s driving their traffic and sales — are getting that traffic via the mobile browser, either because the consumer typed in the name of the store or a product and found her way there.

Now you know why Apple is working furiously on a mobile browser solution. Apple Pay in app isn’t really cutting it, since most retailers outside of Amazon (not Apple Pay), eBay (not Apple Pay) and Walmart (Apple Pay) aren’t driving a lot of sales via their mobile apps.

It also explains why the Checkout Conversion performance of most retailers is so poor. Their consumers are using mobile to get to their sites, but not to close the loop since checking out is too painful.

But back to Apple and its revenue reversal.

SAY HELLO TO THE (APPLE) TAX MAN!

Nine years ago, Apple introduced the world to the notion of a device and a software platform that put a bunch of useful tools called apps at our fingertips. Nine years and 1.5 million apps later, the iPhone has become an access device to a few of those apps that consumers use a lot. Some of them, like Facebook and Google and Amazon for commerce, have powerful ecosystems of their own, that today are accessed via another very powerful ecosystem – Apple’s.

Apple, no doubt, has noticed. My guess is that Apple will start looking to the App Store for more revenue — they have got to be thinking of ways to diversify their risk if the iPhone 7 doesn’t save their bacon and the Apple Watch keeps struggling. They won’t be as brazen as to hit all the apps at once, but I would bet we will see more and more steps to make money from the app ecosystem.

Then there’s another play which we’ve seen with Apple Music. If there’s a great profitable app that runs on the iOS platform — like streaming music — maybe Apple can muscle its way into the business and get some profit that way. Apple Music was partly a defensive move given the impact of streaming on their download business. But there are lots of other areas Apple could get into where it can leverage all the advantages of owning the home screen and — importantly — not pay the tax everyone else has to pay to be on the platform. Maybe that’s a travel app or a finance app or a competitor to Uber, a restaurant reservations app – something that has universal appeal and represents a way into a revenue opportunity that Apple can control and negotiate a hard bargain.

But as much as Tim Cook claims the recent revenue decline is much ado about nothing, investors think it is – and he probably does as well. So don’t count anything out. And if you have a business that depends on an app that depends on iPhone users, be forewarned — we may be well past April 15th, but the tax man cometh.