They may have startled Wall Street investors, but for consumers, merchants and retailers, Affirm’s results are the latest affirmation that the seismic shift towards buy now, pay later, (BNPL) is continuing to bear fruit with customers using the payment option more often.

As much as the current economic outlook has muddied the near-term waters, BNPL’s long-term uptrend is still very much intact.

Transacting More Often

The company’s total transactions were up 139% in the latest quarter, while its transactions per active user rose 31%, compared to an 8% growth rate a year ago, as the typical BNPL user did three transactions during the quarter, up from two a year ago.

To get a sense of just how pervasive and persuasive BNPL has become, consider this stat fresh out of the latest PYMNTS monthly BNPL Tracker.

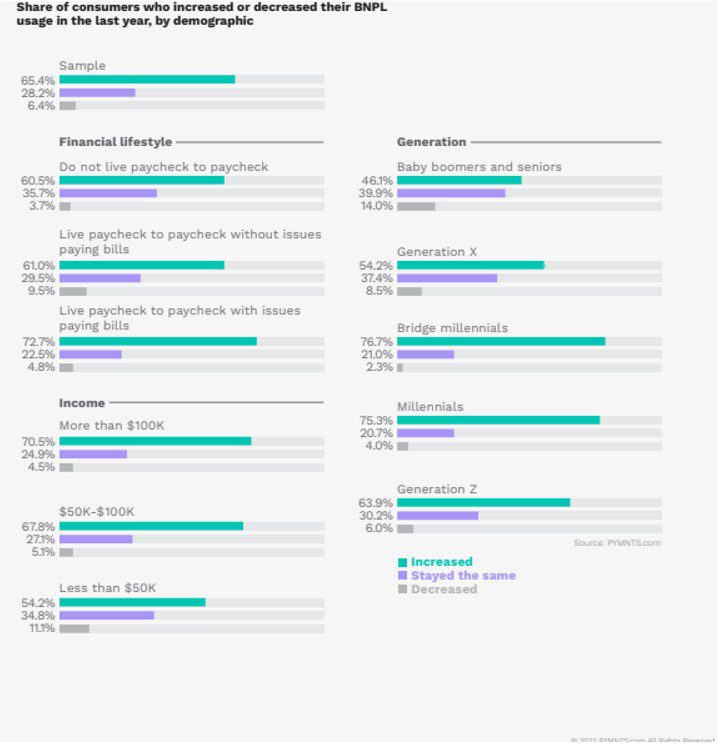

More than 46% of baby boomers and seniors and 71% of BNPL users with incomes over $100,000 increased their use of BNPL in the last year.

Those are the wealthiest consumers, the ones with relatively more financial firepower than other cohorts.

We’re well beyond the days when BNPL might have been described as being a bit, well, down-market, a credit tool used by those who might not have access to traditional credit.

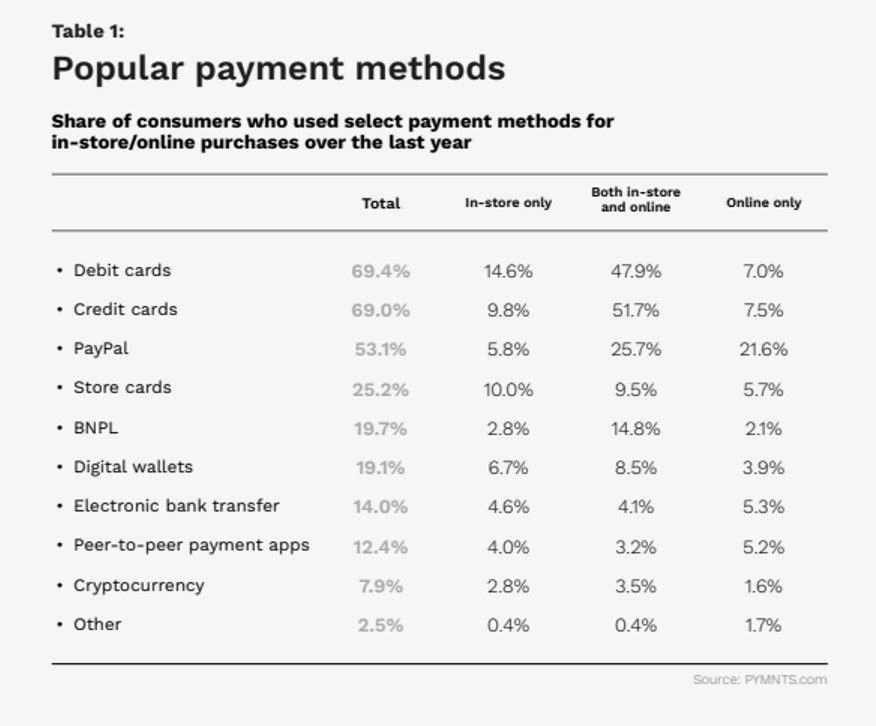

As is well known to readers of this space by now, we’re a nation that, by and large, lives paycheck to paycheck (about 61% of us do).

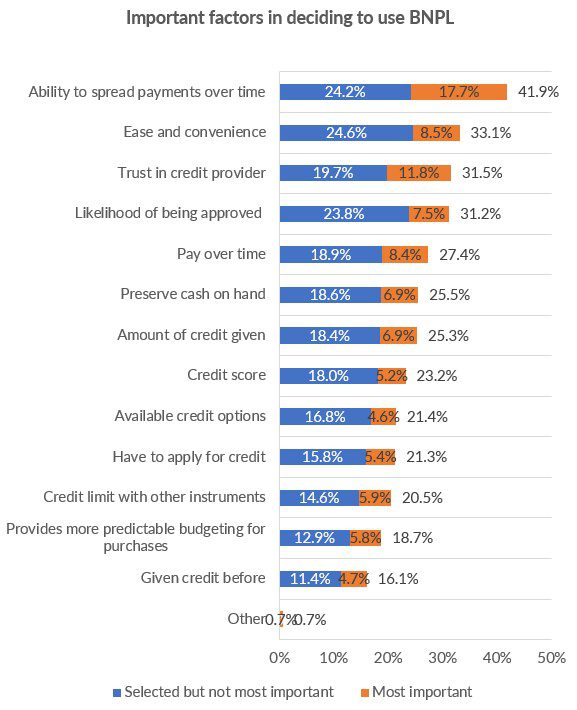

Staggering monthly payments out over time gives some breathing room to get what we want or need, and be able to pay for it all. Ease and convenience are top of mind in spurring consumers to use BNPL.

Source: PYMNTS.com

Ease of use leads, naturally, to a comfort level of using the offerings again and again.

Industrywide, per the Affirm information, gross merchandise mix was skewed to general merchandise at roughly a quarter of the $4.4 billion gross merchandise value, where GMV was up a staggering 477% year over year in the quarter; and fashion and beauty (19% of the mix), gaining 68%. Eighty-five percent of the consumers transacting across the company’s platform, Affirm said, are repeat customers.

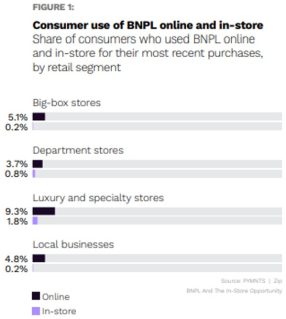

The mix dovetails with the accompanying PYMNTS chart that finds most of the activity taking place at general merchandise operators — but also spotlights the relatively low penetration that BNPL has, at least for now (i.e. low single-digit percentages).

The mix dovetails with the accompanying PYMNTS chart that finds most of the activity taking place at general merchandise operators — but also spotlights the relatively low penetration that BNPL has, at least for now (i.e. low single-digit percentages).

And CEO Max Levchin said on the earnings conference call that the numbers have been buoyant, though home wares have declined. Travel agencies offering BNPL have soared amid the great reopening, and Affirm noted on the call that travel and ticketing, at 14% of GMV, gained 87% year on year. Merchant count stands at more than 234,000, per the company data, up 13% year over year, driven in part by Shopify.

The urgency for merchants to offer BNPL at the desired point of sale is there, given the inroads BNPL has made as a popular payment method, as seen below.

As for the outlook:

“Despite what you may have heard elsewhere people are still buying things online,” he said. But the economy is likely in the beginning of a downturn, he said, and credit performance remains a “non-negotiable guardrail” for the company.

Credit quality — a key, much-watched metric — is still strong, said CFO Michael Linford, though management also said that there were signs of stress among certain low-credit consumers. Delinquency levels remain healthy, he said, and the earnings release shows allowance for credit losses as a percentage of loans held for investment at 6.2%, up from the 3.8% seen a year ago but lower than the 9.2% seen two years ago in the depths of the pandemic.

Levchin and Linford said they feel confident about the current state of the credit portfolio and also indicated that there remain a number of levers that can be adjusted, such as requiring larger down payments at the initiation of a BNPL loan.

And yet: Macro headwinds show up in the look-ahead. The estimates of growth assume continued momentum with Amazon and Shopify, and there will be holiday driven, seasonal spending trends in place that have been seen in the past. Seasonality will result in a decline in revenue as a percent of GMV. GMV guidance of $20.5 billion to $22 billion would imply 20% to around 41% growth from the most recent fiscal year, where that rate had been 77% in the most recent quarter.

Investors sent the shares down by more than 12% in after-hours trading.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More