Buy now, pay later (BNPL) has taken the retail world by storm, thanks in large part to its impressive array of benefits for merchants and enhanced customer experiences. PYMNTS research found that in 2021, 13.5% of consumers used BNPL services within the prior year, and another 44.7% know that it is an option even if they have not personally partaken. Nearly two-thirds of consumers say they are more likely to shop at stores that offer BNPL, and roughly two-thirds said that BNPL allows them to make purchases more frequently.

Both of those reasons for using BNPL are excellent news for merchants that offer it, as they directly lead to increased ticket sizes, conversion rates and overall revenue. Some merchants can face challenges in implementing these programs, however. The following PYMNTS Intelligence digs deep into the benefits of BNPL for merchants and how they can overcome implementation obstacles.

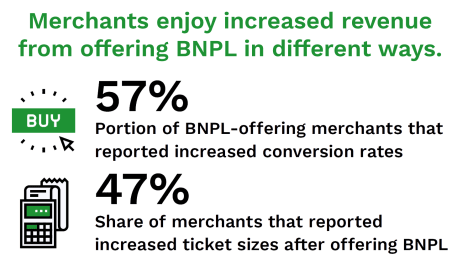

Businesses that leverage BNPL can raise revenue, brand awareness and customer loyalty.

Increased conversion rates are one of the most immediately evident benefits since customers who leverage BNPL are much more likely to complete a purchase than those who do not. Fifty-seven percent of merchants offering BNPL said they improved conversion, countering one of the most common struggles eTailers face in that most shoppers abandon their carts before checkout.

Retailers also report quantifiable benefits in the form of increased brand awareness, with 53% of merchants saying that BNPL providers exposed their brand to new customers. Forty-seven percent of merchants have also reported an increase in average order value, which, combined with the improved conversion rates, leads to a hefty overall increase in revenue.

BNPL is also valuable for attracting repeat customers. PYMNTS research found that there is a strong likelihood that customers who leverage BNPL will use it again and look more fondly upon merchants offering it as an option. Sixty-six percent of millennial consumers said they have a positive view of luxury and specialty retailers that offer BNPL, and 58% say they are more likely to patronize the store again to leverage BNPL payment options.

Legacy BNPL schemes increase the risk of merchant-shopper disintermediation.

Some merchants fear that using BNPL could potentially drive shoppers away from their website directly to the BNPL provider’s platform if they find it a more convenient experience when using these payment plans. This disintermediation process could potentially result in lost revenue as customers are not exposed to the rest of the merchant’s products and reduce their cart sizes.

Other merchants report that BNPL had complicated their return policies and disincentivized customers from leveraging the platform due to this added effort. Most cases involved the consumer contacting the merchant as well as the loan provider and continuing to make payments on the item until the return is fully processed. This, in turn, makes customers less likely to purchase items such as clothing that have a high probability of needing to be returned.

Solving these problems will require BNPL providers to simplify return protocols and reduce fees to further encourage the platforms’ use among merchants.