Emerging from the stock market rubble that was this past week, the Connected Economy stands battered and bruised, at least as measured by universal declines in stock prices.

If there was one overarching theme governing the decline, it would be: Inflation continues its inexorable rise, and recession fears are mounting.

And there’s a new 800-pound gorilla in the buy now, pay later (BNPL) sector, which roiled our “pay and be paid” names.

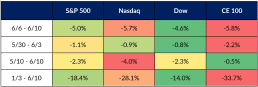

Overall, the CE100 Index skidded 5.8% on the week, topping the 5.7% decline in the Nasdaq, and now stands 33.7% lower for the year.

CE100 Relative Performance

Source: PYMNTS

The worst performance came from the Live pillar, which lost 8.7%, followed closely by the Banking segment, which lost 8.5%.

In the Live pillar, the performance was hurt by double-digit declines in Porch, which lost 15.8% and Zillow, off nearly 10%. Concerns over the state of the housing market, and specifically over interest rates (they’re set to rise again) and what will happen to mortgage applications, took a toll. The housing market boom faces headwinds, and those headwinds are being reflected in stock prices.

The banks? Well, they also suffered this week, and of course they have exposure to the housing market. Though the conventional wisdom holds that banks show better net interest margins amid higher rates — because they can make more money on loans — there’s still some uncertainty over what the credit environment holds over the near and longer term. Ally Bank was down 11%, JPMorgan by a bit more than 8%.

Apple Roils the BNPL Space

The Pay and Be Paid pillar had its own struggles, as Sezzle slid 20% and Affirm lost 18.6%. No surprise here: Apple’s entry into the BNPL space threatens to upend the competitive landscape.

As reported in this space, Apple, through Apple Pay Later, is handling the lending itself through its wholly owned subsidiary Apple Financing, which will oversee credit checks and make decisions. And, as we noted, Goldman’s role in Apple Pay Later is enabling Apple to access the Mastercard Network.

In terms of the mechanics, users in the U.S. will be able to split the cost of an Apple Pay transaction into four installment payments over six weeks, with no attendant interest charged or fees levied. The payments are done, tracked and repaid through the digital wallet.

Read more: Seven Years Later, Only 6% of People with iPhones in the US Use Apple Pay In-Store When They Can

As for Apple Pay, heading into the end of the third quarter of last year, PYMNTS’ own data showed that roughly 94% of consumers with Apple Pay activated on their iPhones did not use it in-store to pay for purchases. Seven years on, that stat might be seen as disappointing. It’s a rate roughly flat with the previous couple of years.

Getting a bit more granular, and moving beyond sector performance, some of the most notable declines during the past several sessions came from DocuSign, which sank more than 24% on Friday, on the heels of earnings results that showed slowing growth. Billings came in lower than the Street had expected. In announcing its fiscal first quarter results, the company said that billings were up 16% year on year to $613.6 million.

No easy week in the rearview mirror, no easy week of trading lies ahead.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More