RIP Digital Transformation, We Hardly Knew Ya

It’s over. It’s done. Stick a fork in it.

All those digital habits that consumers developed and fine-tuned over the last two years — they were temporary, at best.

Ordering groceries online? An anomaly.

Having DoorDash or Uber Eats show up at the consumer’s doorstep two or three times a week? A blip.

Binge-watching Bridgerton on Netflix? No mas, as consumers head back to the theatres and binge-eat movie theatre popcorn instead.

Ordering stuff from Amazon? Seriously people, that’s so 2019.

Today, it’s brick and mortar, baby — all consumers, all the time.

And shop ‘til you drop in those same malls and retail storefronts that were gasping for life in 2019 as a result of a 20-year decline in retail sales growth (and their market caps) at the hands of those same online players that are today’s poster children for The Great Digital Demise.

The ‘new’ normal in 2022?

It’s the old normal that just took a two-year COVID timeout.

That’s certainly the sentiment you get when you read almost every media account about the “decline” in the consumer’s use of digital channels and the corresponding stock market drubbing the tech, FinTech and Big Tech company stocks are taking.

The so-called proof points are well documented.

The Nasdaq suffered its worst performance since 2008 in April. The basket of FinTechs that went public between 2020 and today has declined 40% in value. The CE100 Index of the 100 publicly traded stocks that represent the connected economy’s future has declined 30 percent this year, after outperforming the Dow and S&P in 2020 and 2021.

Related: Dismal Stock Performance Misses Mark on Connected Economy’s Potential

As of the market close on Friday May 13, 2022, PayPal’s stock was trading at levels not seen since April 2018, Shopify’s since December 2019, Amazon’s since April 2020, Block since July 2020. Teladoc is trading at levels not seen since January 2018, Uber at levels not seen since March 2020.

The market is treating these companies — and many others — as if the payments innovations and digital transformation of consumers and businesses witnessed over the last two years — en masse and everywhere in the world — was fleeting, a fluke buffered by habits that are unsustainable and now reversing course before our very eyes. This despite reported growth in users, user engagement and GMV from these companies.

For example: Aggregators’ Growth Shows Delivery Habits Buck the Great Reopening

Of course, no one who lives in the real world believes this is even remotely true, stock market drubbing and headlines aside.

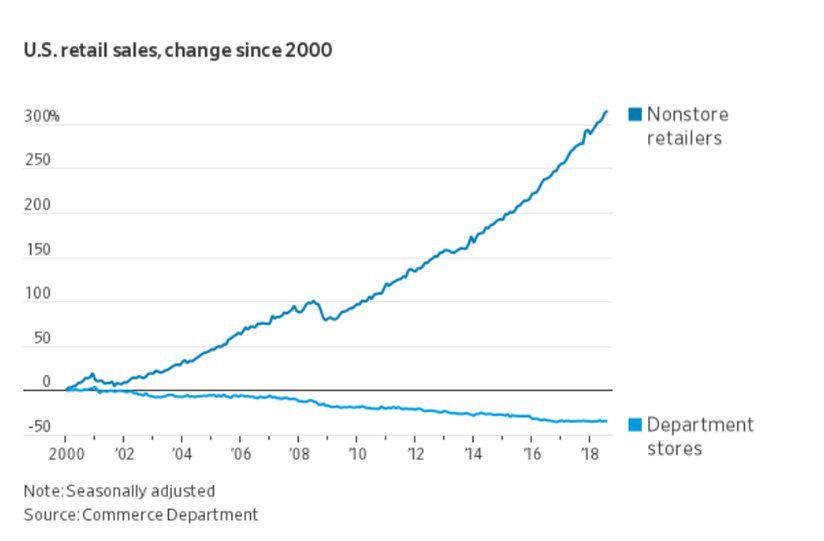

That’s because no one really believes that this chart of non-store retail sales over the last 20 years (courtesy of the Wall Street Journal) is now suddenly going to reverse course. That online sales will flatten or dramatically decline as department stores sales catch a massive tailwind as part of The Great Physical Retail Reawakening.

Or that consumers are going back to cash and taxicabs — or shutting down their video, music streaming and social media accounts.

Instead of more fancy models, maybe we need some good old-fashioned common sense to sort out the digital transformation storyline based on observations of the consumer’s digital preferences, now three years into the world according to COVID.

Let’s look at how great businesses are investing to make the physical world an integrated part of the digital experience consumers have spent two years perfecting — and now expect as they reengage.

The Great Digital Miscalculation

COVID created a jump discontinuity in consumer behavior starting in March/April of 2020 — for the obvious reason. With no vaccines and a rising death toll, people were afraid to leave their houses to do anything if they could do it online instead. When the physical world literally shut down, digital was the only way consumers could access many things.

See also: The Big Jump: Pandemics And The Connected Economy’s Bigger, Faster Future

And without the digital foundations laid by FinTech, BigTech, HealthTech and payments and commerce players over the prior decade, navigating this global pandemic would have been largely impossible.

But navigate and survive we did.

PYMNTS began to examine the consumer’s digital shift every month — the activities that had begun moving more online and less in the physical world before the world shut down — starting March 6, 2020. Even then, our data showed, consumers had begun to pull back from doing business in the physical world.

As the pandemic intensified, so did their shift to digital.

In 2020, we saw consumers doing three or four times more activities in the digital world than they did in the physical one: shopping and ordering food from grocery stores and restaurant aggregators online, working remotely, streaming videos and hanging out more with family and friends on social networks.

Yet, no one expected, nor should they have, that consumers would stay pinned to the max to those COVID-created digital-only behaviors when the world reopened, when consumers were vaxxed and boosted and as the pandemic receded.

Today we see consumers logically doubling down on the activities for which there are no great digital substitutes — traveling, eating out at their favorite restaurants, going to concerts, taking the kids to amusement parks and county fairs — the things that they couldn’t do or felt uneasy doing in the physical world for the last two years. We see a corresponding shift in how consumers spend their money — more on services and activities and less on sofas and barbeque grills. Yet there is not much of a shift in how they find, book and pay for those purchases: more and more digital and less and less cash.

Consumers are also returning to the physical store to buy retail products and groceries. But they’re not doing that to the exclusion of using online channels to make those purchases — and they’re using digital methods to pay for those purchases in the physical store.

See also: Digital Payments To Move The Needle For Retailers

Just like they did in 2019, consumers use a mix of digital and physical channels to get what they want. And despite the sensatio nal down-with-digital headlines, it seems they’re using digital channels to do that even more.

nal down-with-digital headlines, it seems they’re using digital channels to do that even more.

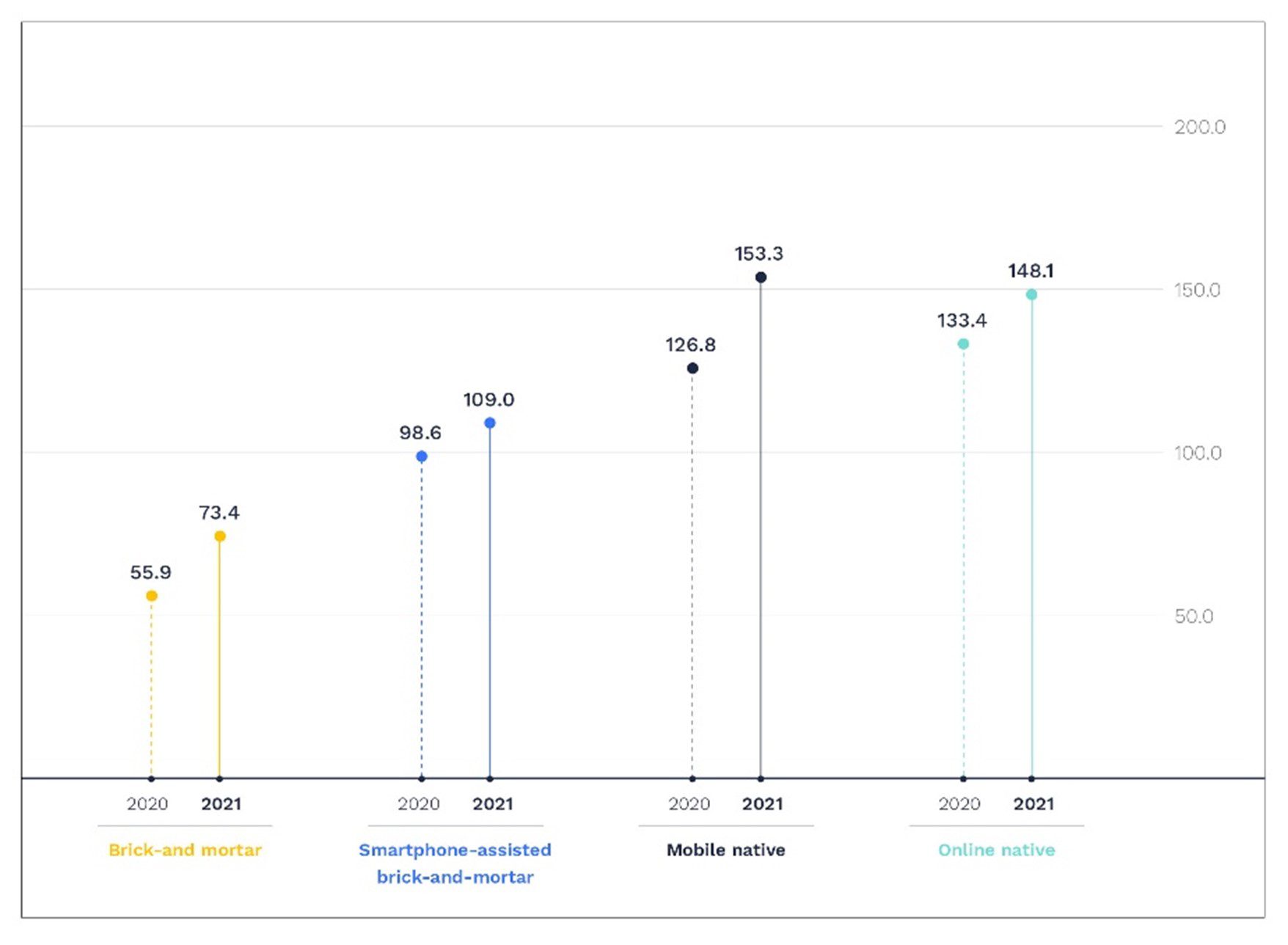

According to Mastercard March 2022 Spending Pulse data, retail sales growth in the online channel is nine times more than in-store, based on a comparison of March 2022 to March 2019.

That’s despite the 3 percent YOY decrease in online sales. Even a small decrease from a massive double or triple-digit increase is still an overall increase, as the Mastercard trend data shows.

PYMNTS April 2022 monthly consumer shopping data shows that 33% of retail purchases were made online, up from 29% in March 2022. PYMNTS data also shows nearly half of US consumers shopped online that same month. Not at the exclusion of shopping in the store — but not at the exclusion of ever using digital channels to buy things, either.

The same holds true for grocery purchases, as we see convenience continue to drive a bifurcation of how consumers buy their food.

PYMNTS April data shows 88 percent of consumers shop mostly for groceries in store, but 12 percent of consumers mostly don’t — a relatively steady state since November 2021. Think about that for a minute. In 2019, the percent of consumers who shopped for groceries online was in the anemic low single digits. Two years later, it is — and seems to remain — almost an order of magnitude higher.

Read more: Digital Economy Payments: How Consumers Pay In The Digital World

More telling, however, is the mix of physical and digital behaviors when making those purchases, shaped by the growing number of in-store shoppers who buy center-aisle grocery items online.

According to the PYMNTS Subscription Commerce Index, done in collaboration with sticky.io, roughly a quarter of consumers have retail subscriptions, with an average of roughly four retail subscriptions for each subscriber. Those subscriptions are for the things that consumers used to buy in the physical store — a small but a growing share of spend for items shifting to digital channels.

See more: Subscription Commerce Conversion Index March 2022

Fully one in 10 retail subscriptions held by U.S. consumers are for Amazon Subscribe & Save — mostly staples, classic center-aisle items for grocery stores. That’s been more or less consistent over the last year. There is every reason to think that even more of that spend will shift online as consumers shop at the grocery store to buy the items they would rather see before buying — and online to buy the things they don’t want to waste their time lugging around in the store.

The same digital behaviors are seen when consumers consider eating at restaurants.

Consumers’ appetite to dine in-person at restaurants doesn’t seem to be denting their use of online channels to order food for takeout or delivery that much. According to the PYMNTS and Paytronix study of consumer restaurant trends for April 2022, roughly a third of consumers are using online ordering options to get food, a percent that has been largely constant since September of 2021.

Read further: Digital Divide: The Key Factors That Drive Restaurant Choice

Digital is even a force when consumers eat inside. Menus are often QR code-enabled, even in hotels for room service, offering restaurant operators better staffing and operational efficiencies, menu and pricing flexibility and checkout opportunities when payment is integrated with digital apps or enabled via digital wallets.

The Great Physical Store Disappointment

Consumers’ use of digital is also shaping how they use the brick-and-mortar store.

The 2022 Global Digital Shopping Index, a six-country merchant consumer study done in collaboration with Visa’s Cybersource, shows that consumers increasingly use stores as pick-up points for online ordering — particularly in the U.S., where consumers over-index their use of online order and pickup, especially for groceries.

Merchants are embracing the consumer’s digital shift and investing to drive more sales using that channel. According to this study, 57% of merchants now allow consumers to use their stores as fulfillment centers because it is as good for the consumer who wants to “buy now and get now” as it is for their own store economics.

Merchants are embracing the consumer’s digital shift and investing to drive more sales using that channel. According to this study, 57% of merchants now allow consumers to use their stores as fulfillment centers because it is as good for the consumer who wants to “buy now and get now” as it is for their own store economics.

See the study: 2022 Global Digital Shopping Index

Merchants are also beginning to realize that just because consumers shop in the physical store doesn’t mean they love shopping there.

The 2022 Global Digital Shopping Index shows that consumer satisfaction when shopping in the physical store is roughly half that when they shop and take delivery online.

In fact, it is the least satisfying way consumers shop.

Hitting Reset

One observation about the digital transformation now seems quite clear: the definition needs a reset.

Digital transformation — at least as we at PYMNTS have written about it — was never intended to mean digital-only. It was always about the reality that, eventually, almost every physical-world interaction will have some kind of a digital connection. The great opportunity that innovators have to create those new experiences for consumers and businesses and to engage and monetize those interactions will power the digital transformation of the global economy.

Digital transformation’s focus, therefore, is making the physical world an extension of the digital experience — sometimes replacing it, but largely as a complement to it. This transformation is rooted in the inevitability that digital and physical will become one integrated experience as ecosystems emerge to streamline and simplify access to the many activities that define the consumer’s day-to-day. How consumers bank, maintain wellness, communicate, eat, have fun, live, move, shop, pay and work already reflects a blending of the online and offline experiences everywhere in the world. Technology will make it possible to move between activities and channels with a consistent experience, payments will make it possible to monetize engagement and digital identity credentials will make access seamless and secure. More innovation and innovators with new and creative use cases will only accelerate the transformation already underway.

Finding the Digital F.I.T.

This reset will take some soul-searching — and for many, a hard course-correction.

Flush with capital, many “me-too” innovators over the last two years focused on the red ocean of low friction/low inertia opportunities as they addressed a wholly captive audience of online consumers without a sustainable business model to support it. But this is also where we will see (and have seen) both massive digital roadkill and consolidation as larger, more successful digital platforms go shopping for features that could become suitable plug-ins. Others have been or will be forced to shut their digital doors.

The herd will also thin where there is high friction — many inefficiencies in how consumers engage in the digital and physical worlds — but the consumer’s interest in embracing digital alternatives remains strong. Here again, business fundamentals will rule as investors divert capital to those who solve real problems at scale. It’s also where digital platforms have already made strong inroads but see opportunities to extend their consumer engagement to new adjacent and differentiating cases.

More on the F.I.T. framework: How To Drive Success In A Digital 3.0 World

Digital transformation’s biggest opportunity, however, is wherever there is much friction in the interaction between consumers and businesses, but where the costs of switching are too high or the benefits too low, so it remains a tough sell.

In each of these cases, success and profits will be about saving consumers’ time. The “T” in the FIT framework is a critical box to check for consumers to overcome their resistance to change — and for entrepreneurs and business leaders to allocate their capital and resources to innovate.

The Great Digital Transformation

Pundits have likened the “Tech Wreck” to the dot com bust of the early 2000’s. Rather than focusing on the crash and the carnage, I’d like to reflect instead on the innovations that flourished in its aftermath. The iPod was born in 2001 and changed not only how music was consumed, but the structure of the music industry. The iPhone followed in 2007, the App store in 2008, creating — along with Android and Google Play — the foundations for the app-based digital innovations we enjoy today.

An examination of the digital behaviors of more than 15,000 consumers across the 11 countries that represent 50% of the global GDP shows digital transformation’s vast potential — almost three quarters of the 40 consumer activities we studied are largely untouched by digital. Some of the most exciting opportunities to explore are those that bring commerce to the consumer, in the many high-engagement digital activities that already have their attention. The low-hanging fruit is to simply make the digital experiences consumers have today, easier and better.

See more: 11-Nation Study: Deeper Engagement Key to Expanding Digital Transformation

Not only is the digital transformation not done and over — it has really only just begun.

Of course, now that people don’t have to do everything online, they are going back to physical — but that shouldn’t be a surprise.

In fact, back in early the 2020s we had every reason to believe we’d be back to normal by the Fall of that year. Instead, it would take more than two full years for most to feel comfortable reengaging.

But the trend lines towards digital-enabled experiences that we have had for the two decades before the pandemic will keep rising. And physical-only experiences will gradually wither as they had been doing even before the notion of a global pandemic became our reality.

The stock market seems to be living in its own world with hard-to-explain rises during the height of the pandemic and just as hard-to-explain nosedives now that it’s receding. Those of us who live in the real world may not know the right price for tech stocks, but we do know the digital transformation is happening under our feet.

To paraphrase Mark Twain, the reports of the death of the digital transformation have been greatly exaggerated.