Inflation is changing the ways in which we eat, whether buying food at the grocery store or dining out.

The PYMNTS Intelligence Paycheck-to-Paycheck report titled “Navigating the Shifting Sands of Consumer Spending Amid Rising Prices and New Tariffs” found that, with the responses of 2,280 U.S. consumers in hand, and extrapolating the data to the larger population, more than 50 million consumers would shift their spending, and in some cases would freeze spending on certain categories outright, should price tags rise by 10% or more.

The pressures are widespread, given the fact that the data show that 65% of U.S. adults live paycheck to paycheck. A significant 22% of consumers find it a struggle to meet their monthly obligations, which means that even keeping the fridge full or the pantry stocked is no easy task.

The Pressures of Earning the Daily Bread

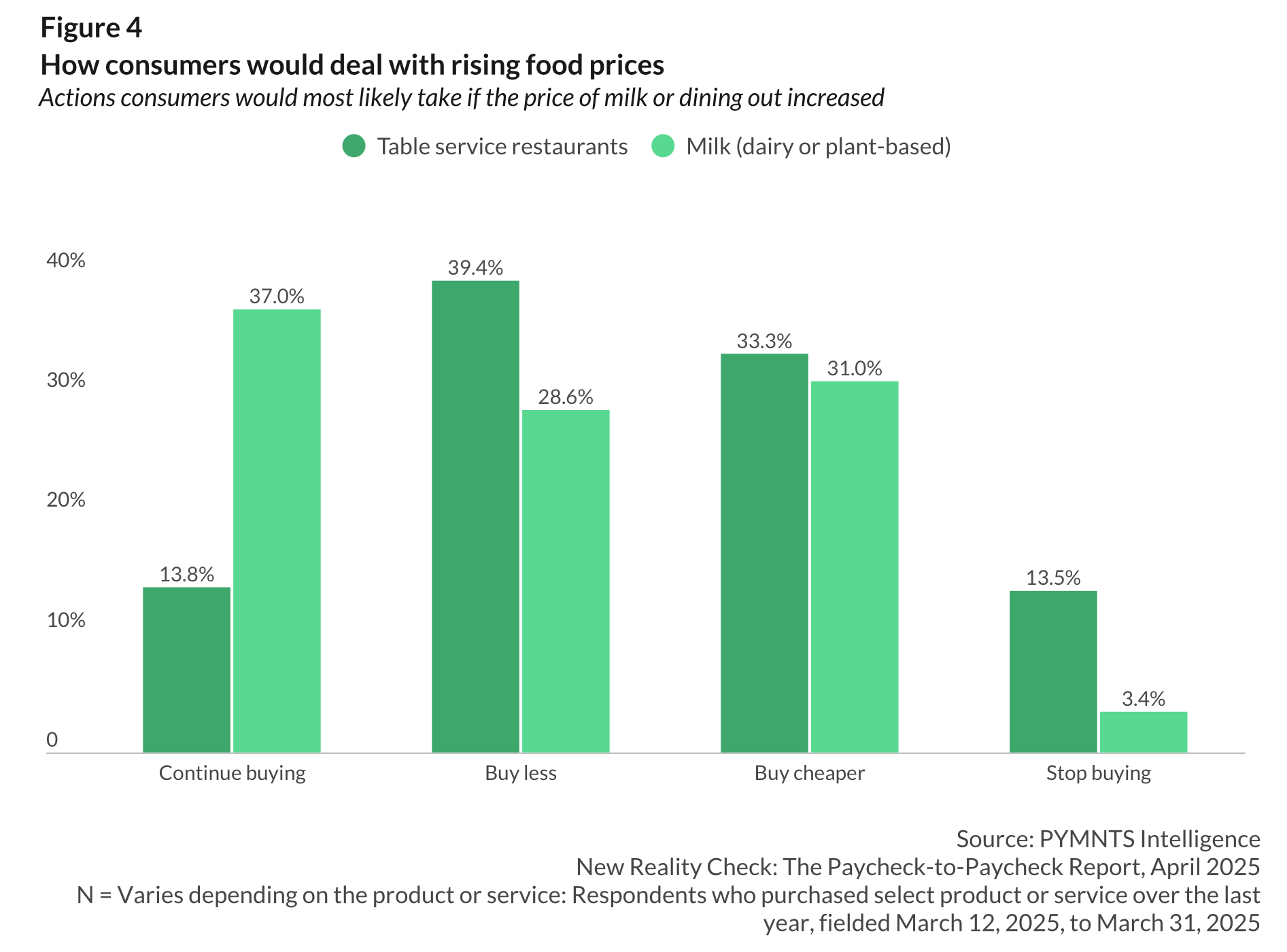

The data show two-thirds of consumers would fine-tune how and where they spend their dollars on groceries or when going out to eat. Of that percentage, half of the respondents say they would buy less, in terms of quantity, and half would opt for cheaper options.

There’s at least some resilience and reluctance to move to forgo dining out with the family entirely, despite inflation. It is indeed the case that restaurant dining is viewed as discretionary; just 14% of consumers are willing to eliminate it entirely after price increases.

Juggling Higher Prices at Local Eateries

But the willingness to move toward less frequent visits to the restaurant or to move to cheaper establishments may signal bumpy times ahead for the local establishments that may lose customers to the fast food joint down the street — and we’d note, they might wish to examine promotions and offers as ways to incentivize repeat business. When surveyed about whether they would keep spending on table service at restaurants — in other words, going out to eat, 39.4% of individuals indicated to PYMNTS that they would “buy less,” which is a nod to the fact that the ticket size of what’s spent at the table would decline; they could also opt to dine out less frequently.

As for groceries, staples are staples. Only 3.4% would stop purchasing milk (dairy or plant-based), demonstrating its essential status in household budgets.

No matter the setting, the data show there’s a wide gulf between how consumers live and what they’re willing to change when it comes to commerce. Another 31% of financially secure consumers reported they would continue buying at their current quantity and frequency. By contrast, only 13% of paycheck-to-paycheck consumers with issues paying their monthly bills indicate the same. Financially stable consumers are 169% and 150%, respectively, more likely than more financially pressured peers to keep their groceries and dining out purchasing behaviors intact.

There are other data points that show consumers may be inclined to “front load” some of their dining out where they can, or even to stock up on goods where they can too. As PYMNTS reported late last month, the latest University of Michigan gauge on consumer sentiment detailed that short-term inflation expectations (one-year expectations) surged from 5% in March to 6.5% in April, the highest level since 1981. Long-term inflation expectations (five-year expectations) increased from 4.1% to 4.4%, the highest since 1991. Inflation expectations shifted in response to significant trade policy developments last month.