However, women, who are responsible for managing daily expenses, have a better sense of what can and can’t be cut when it comes to improving the monthly cash flow.

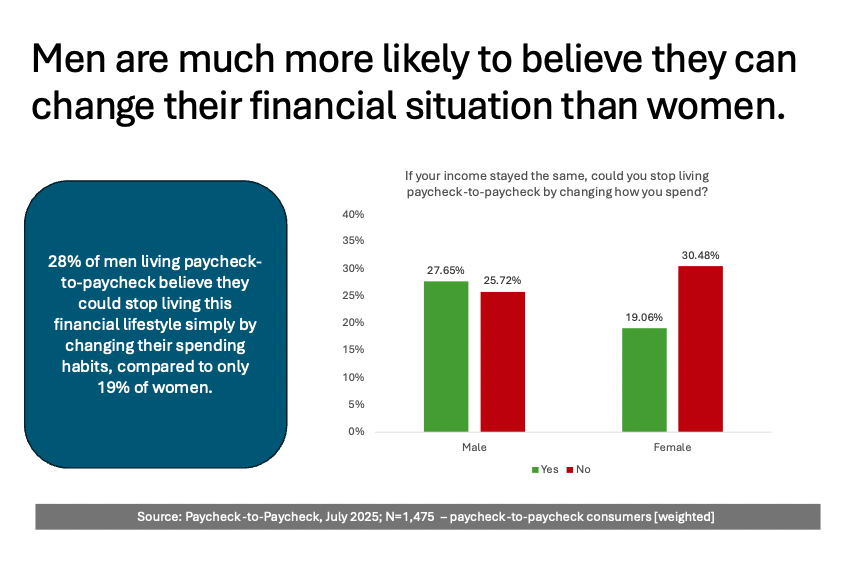

A PYMNTS Intelligence “Paycheck-to-Paycheck” analysis of 1,475 U.S. consumers found that the gender gap is wide enough to drive a budget spreadsheet through. Asked whether they could stop living paycheck to paycheck if their earnings stayed flat but their spending changed, nearly 1 in 3 men said “absolutely.” Fewer than 1 in 5 women said the same.

The split persisted even after leveling the family expense playing field. Married men maintained their conviction in the money makeover, and dads with kids under 18 were no less bullish than bachelors.

However, optimism must often crash up against reality, especially in an environment where inflation is stubborn and price increases are fueled by tariffs. The data showed that more than two-thirds of consumers live paycheck to paycheck, so finding some way to improve the ebb and flow of cash flow is paramount.

Women often quarterback day-to-day household finances and caregiving budgets, so they see the hard limits on discretionary cuts. Men, by contrast, may underestimate fixed costs.

Advertisement: Scroll to Continue

PYMNTS Intelligence researchers drilled down into two statistically subsamples: 804 married respondents and 541 parents with children under 18. In each sample, participants answered the same core question: “If your income stayed the same, could you stop living paycheck to paycheck by changing how you spend?” Response options were a simple “Yes” or “No,” enabling a clean measurement of financial self-assessment.

Key Data Highlights:

- Overall Consumers Living Paycheck to Paycheck: Twenty-eight percent of men said they could break the cycle through spending changes alone, compared with 19% of women — an optimism gap of nine percentage points.

- Married Consumers: Thirty-six percent of husbands said belt-tightening would do the trick, versus 21% of wives — showing that shared mortgages and grocery bills don’t do much to erase women’s views that cash flow pressures persist.

- Parents With Children Under 18: Thirty-six percent of fathers living paycheck to paycheck were sure that spending tweaks would suffice, but only 23% of mothers agreed, underscoring that caretaking costs — tied to everything from school to recreation — weighed more heavily on women’s calculations.

The disparity is not merely about who shoulders more fixed expenses. Instead, respondents’ commentary suggested a behavioral explanation. Women more often manage family budgets and caregiving outlays, giving them a clearer view of non-negotiable costs. Men, who are less likely to run the household balance sheet, may assume more wiggle room than actually exists.

For banks, FinTechs and payments players, there’s a key takeaway and an opportunity to work with their customers to shore up the status of the household finances. Financial wellness tools, including budgeting apps, must account for gendered perceptions, not just gendered pay gaps, to improve cash flow and financial security.