Not long ago, cryptocurrencies were poised to take over the world and certainly change how we pay.

Consumers and businesses would, conceivably, embrace bitcoin and other altcoins, shouldering aside traditional finance — you know, bills and coins, credit cards and bank accounts too, got that matter.

Decentralized finance, or DeFi, as it is commonly called, has gained its share of adherents, it is true. After all, even with all of the volatility in the mix, the “market cap” of the crypto industry now stands at about $400 billion, which is a proxy for the “value” of the coins held across the globe.

But the jury’s still out as to just how far crypto can move the needle in terms of everyday spending — i.e., getting the morning cup of coffee, paying for gas, paying rent or maybe even buying a house — you get the picture.

The window of opportunity seems to be closing, at least a bit, and the road to mass acceptance of crypto as a payment choice will be a rocky one.

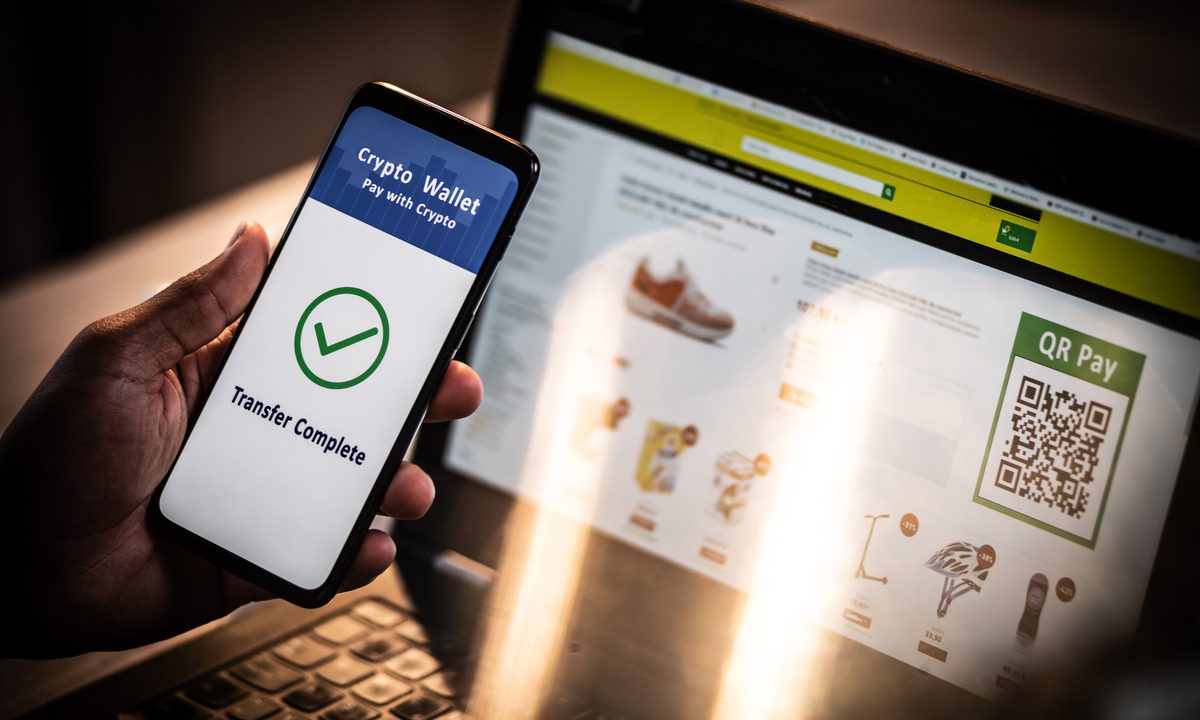

As noted in recent PYMNTS research, “Paying With Cryptocurrency: What Consumers and Merchants Expect From Digital Currencies,” a collaboration with BitPay, we see that familiarity with crypto — let’s face it, the sector dominates business and mass-media headlines — the number of crypto holders is not insignificant.

But they’re not using bitcoin and its brethren to spend. The data gleaned from more than 2,300 consumers and more than 200 merchants shows that 23% of consumers currently hold or have held cryptocurrency in the past 12 months.

Bitcoin as Shorthand

Drill down a bit and we can use bitcoin as shorthand for the group. Only 12% of those surveyed have held bitcoin, and roughly 74% have never held the coin but “know” the coin. It seems, at least to us, that knowledge is not necessarily translating into intent and action to actually get and use bitcoin.

And there may be a bit of disconnect in terms of use cases. PYMNTS found that about 55% of consumers hold their digital assets for investment purposes. That leaves about 45% who are holding cryptocurrencies for other reasons — which would include transactions, of course. It’s a significant percentage but hardly a tsunami of intent.

The merchants are getting ready, though boosting the points of acceptance is an important part of stimulating demand. Forty-two percent of businesses that do not accept cryptocurrencies for purchases plan to accept them and begin making payments within 12 months.

As reported in this space recently, there has been at least some growth in so-called passive investments, such as round-up and crypto-back rewards on credit and debit card spending. By way of example, Visa, Mastercard and recently American Express have gotten behind crypto rewards.

And in another recent example, Abra, the digital asset financial services company, announced a new crypto rewards card to transact in U.S. dollars, offering crypto back on its Abra Crypto Card.

Bit by bit, crypto may find its way into commerce’s mainstream — but the journey will be a fitful one.

Read Also: Bitcoin Buyers Are Bailing, but Crypto Rewards Haven’t Lost Appeal

Sign up here for daily updates on all of PYMNTS’ Crypto coverage.