Businesses and consumers are returning to their pre-pandemic norms, but some of their behaviors have changed. Banking customers are less likely to visit banks now than they were 18 months prior, and nearly all consumers have an online or mobile banking feature at their disposal. The push to digitization highlighted the advantages of online banking, with 46 percent of United States consumers becoming “digital shifters.” Only 9% of former branch loyalists said they visited a branch more since the pandemic started.

Customers are more willing to try new technology, whether it is opening a bank account digitally or downloading a new mobile app. Some consumers, however, particularly older generations, still hesitate to adopt fully digital financial profiles. Concerns about stolen identity and discomfort with new, unfamiliar technology feed their hesitance. Overall trust in banks and other financial institutions (FIs) decreased during the 2020 digital shift, a fact that may be attributed to the dehumanization of the banking space.

Customers are more willing to try new technology, whether it is opening a bank account digitally or downloading a new mobile app. Some consumers, however, particularly older generations, still hesitate to adopt fully digital financial profiles. Concerns about stolen identity and discomfort with new, unfamiliar technology feed their hesitance. Overall trust in banks and other financial institutions (FIs) decreased during the 2020 digital shift, a fact that may be attributed to the dehumanization of the banking space.

In the latest Digital-First Banking Tracker®, PYMNTS examines how banks can personalize digital banking channels to increase customer satisfaction while still maintaining a digital-first mentality.

Around the Digital-First Banking Landscape

Many consumers rely on mobile tools to manage their finances. Increased adoption of new banking technology started out of necessity during the pandemic, but a growing number of customers plan to keep using those banking tools even after the threat has passed. A Chase survey showed that 89% of respondents used their mobile app to deposit money by the second quarter of 2021 after physical branches reopened. Mobile banking also offers customers perks such as money-saving tools and fraud alerts, making users feel more in control of their personal finances.

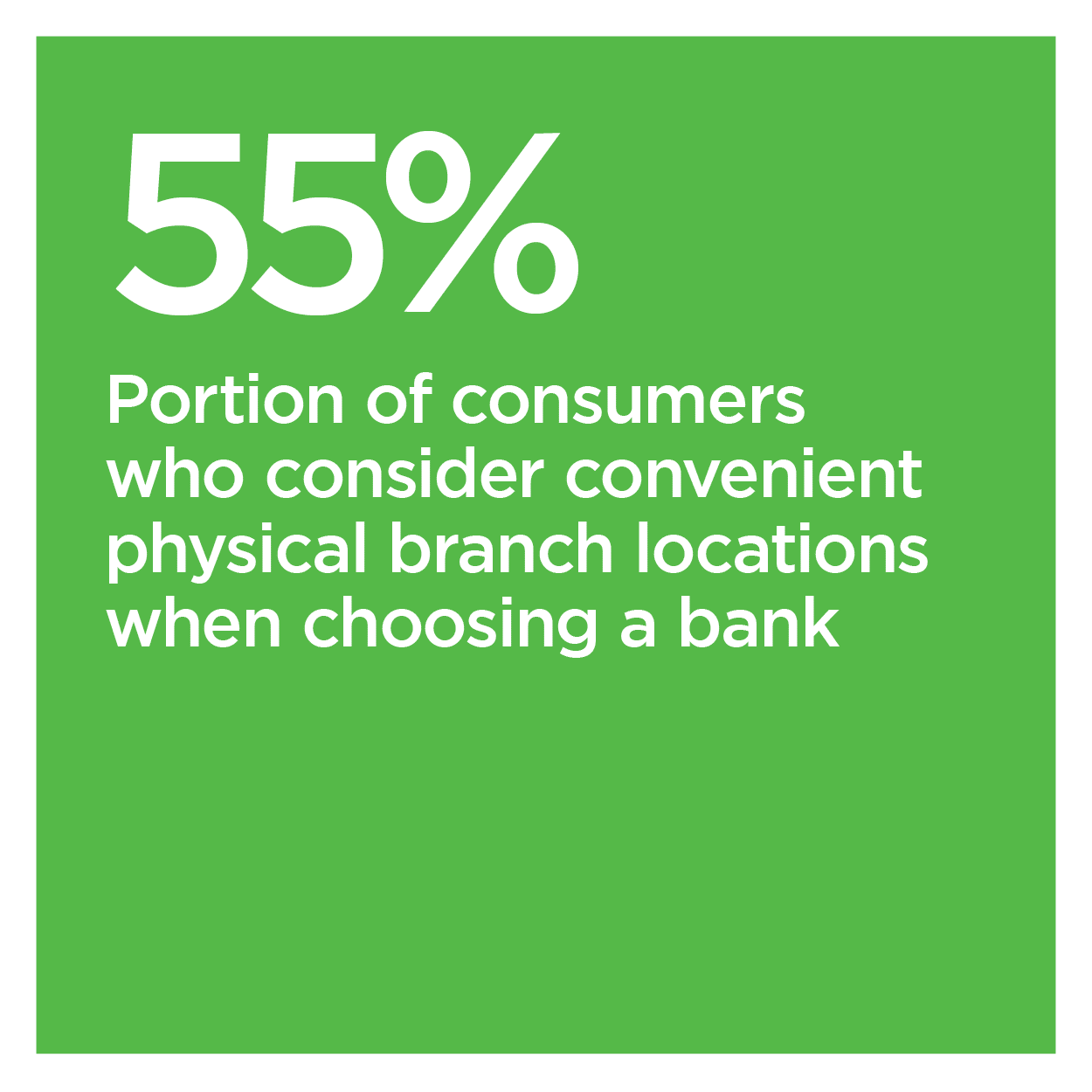

Before the pandemic highlighted the need for digital options, some banking services were available exclusively at a physical branch, and others were only online. Eighty-seven percent of consumers trust their FIs, according to a PYMNTS survey, and access to branch services helps to reinforce that trust. Amid the digital-first push, customers still want the option to visit a physical location and communicate with a human teller if any autonomously unresolvable issues arise. A mix of digital offerings and human interactions will lead to higher customer approval ratings.

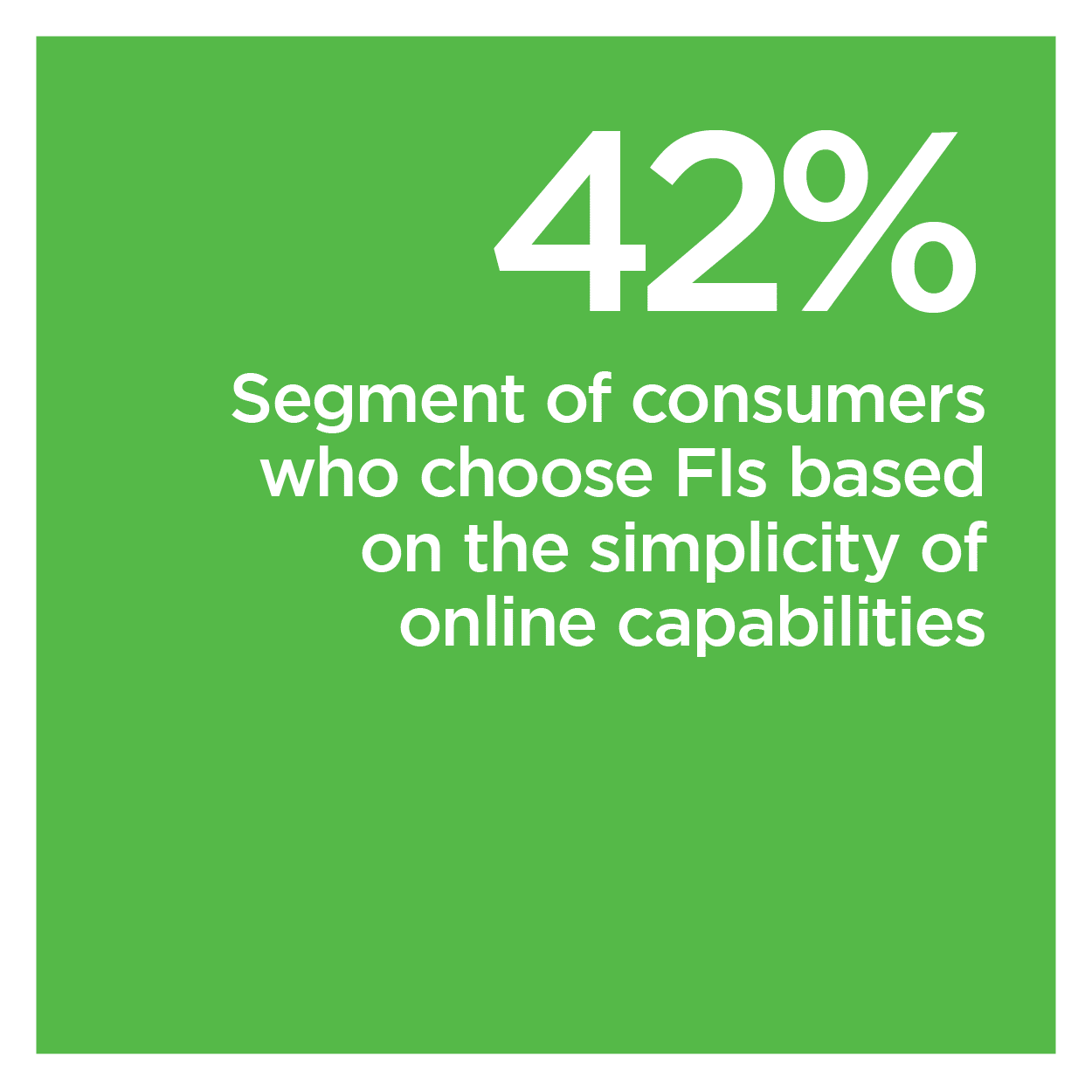

Banks and FIs are usually slower to innovate their technology than other institutions, but they had to accelerate their digitization tactics due to the global pandemic and the subsequent increase in challenger banks and FinTechs. Nearly all financial firms believe next-gen technologies are valuable, reported a Broadridge survey. Next-gen technology can improve risk management, decrease time to market and enhance informed decision-making. Using this new technology in addition to traditional banking practices is the most effective way to increase customer efficiency.

For more on these and other stories, visit the Report’s News & Trends.

How Banks Can Humanize Digital Offerings to Satisfy Diverse Customer Demands

FIs have offered mobile and online banking options for many years, but some consumers, particularly older demographics, were hesitant to use digital tools for their finances. The pandemic limited access to physical branches, however, forcing branch stalwarts to reevaluate their outlook on technology. Safety concerns and fear of viral contraction also contributed to the adoption of mobile apps by traditionally-minded customers. While technology-enthusiasts and fundamentalists have both reported being satisfied with recent innovations, they still want the option to interact with a human should any issues arise. Humans have seen the convenience banking technology provides and will continue to want that, said Sabrina McDonnell, executive vice president and chief customer experience officer at Simmons Bank, but that does not mean they do not want human interaction. To learn more about why banks continue to offer human-based services during a time of increased digitization, visit the Report’s Feature Story.

Safety concerns and fear of viral contraction also contributed to the adoption of mobile apps by traditionally-minded customers. While technology-enthusiasts and fundamentalists have both reported being satisfied with recent innovations, they still want the option to interact with a human should any issues arise. Humans have seen the convenience banking technology provides and will continue to want that, said Sabrina McDonnell, executive vice president and chief customer experience officer at Simmons Bank, but that does not mean they do not want human interaction. To learn more about why banks continue to offer human-based services during a time of increased digitization, visit the Report’s Feature Story.

Deep Dive: Banking Customers Need to Feel a Personal Connection

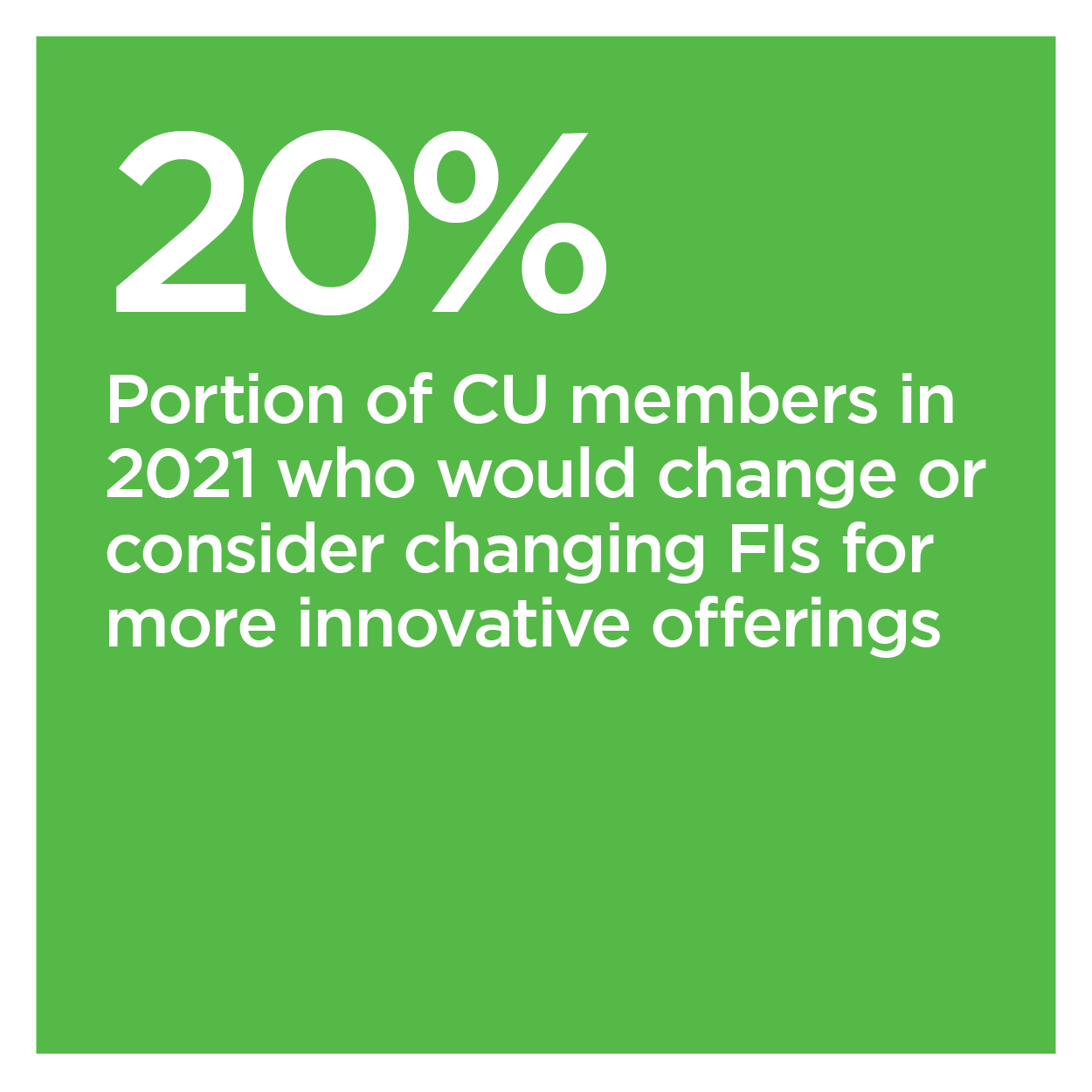

A large portion of consumers shifted their banking services from in-person to online platforms in 2020. The shift made everyday tasks like paying bills or cashing checks more accessible amid COVID-19 lockdowns and restrictions. Adoption of digital banking profiles extended across all demographics, and 26% of branch loyalists reported using online banking more now than before the pandemic. As a result of the shift in consumer behavior, many physical branches around the globe closed their doors. To learn more about how digital adoption during the pandemic modified the online habits of customers and what their new expectations are, visit the Report’s Deep Dive.

About the Tracker

The Digital-First Banking Tracker®, a PYMNTS and NCR collaboration, examines the digital banking sector. The September issue highlights recent developments in the digital-first space, including how lenders are expanding digital access for customers.