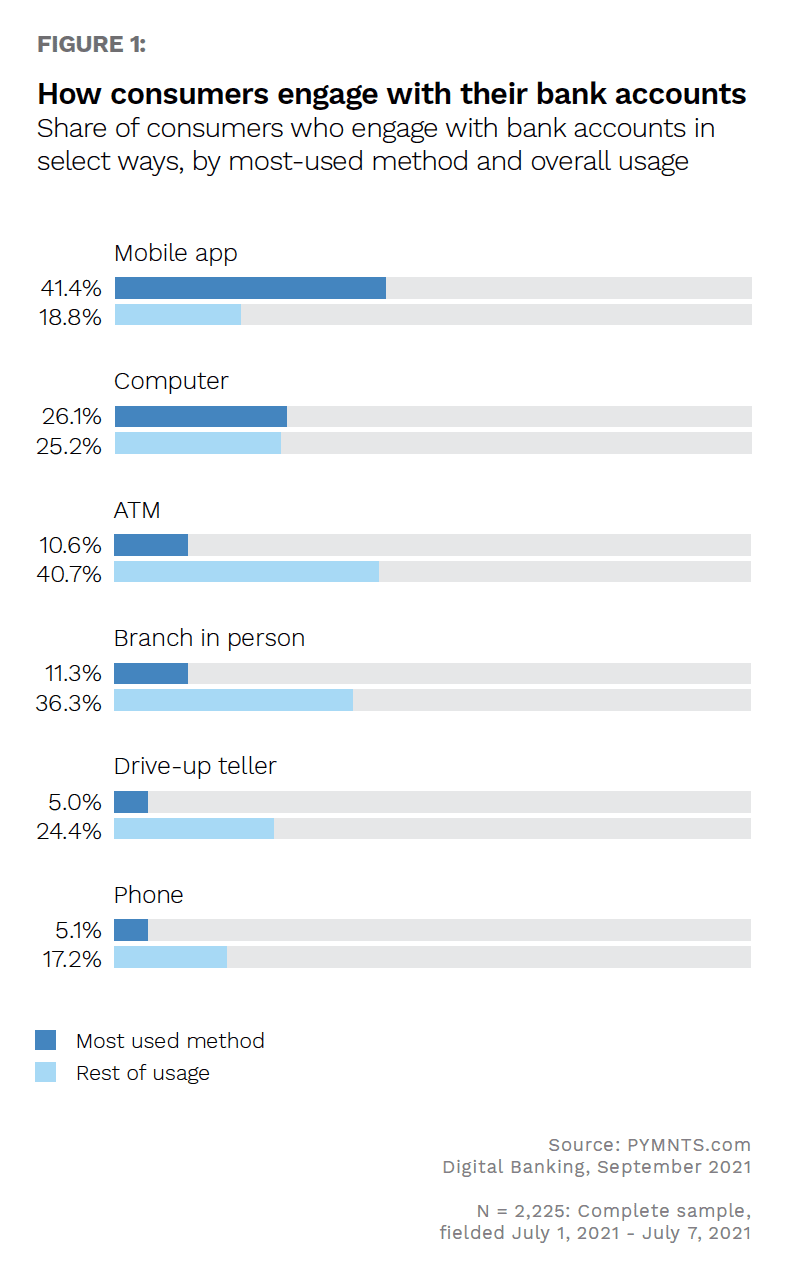

The accelerated digital transition that accompanied the pandemic has contributed to greater reliance on digital banking tools. While 48% of surveyed consumers still use branches, just 11% say branches are their primary banking method, in contrast with 41% who bank primarily using mobile apps. More than 80% of consumers connect with their accounts digitally, including 26% who most often access their accounts with a computer. At the same time, just 7% of consumers use a digital-only bank. This is possible because digital banking access has become nearly ubiquitous, regardless of the type of financial institution (FI).

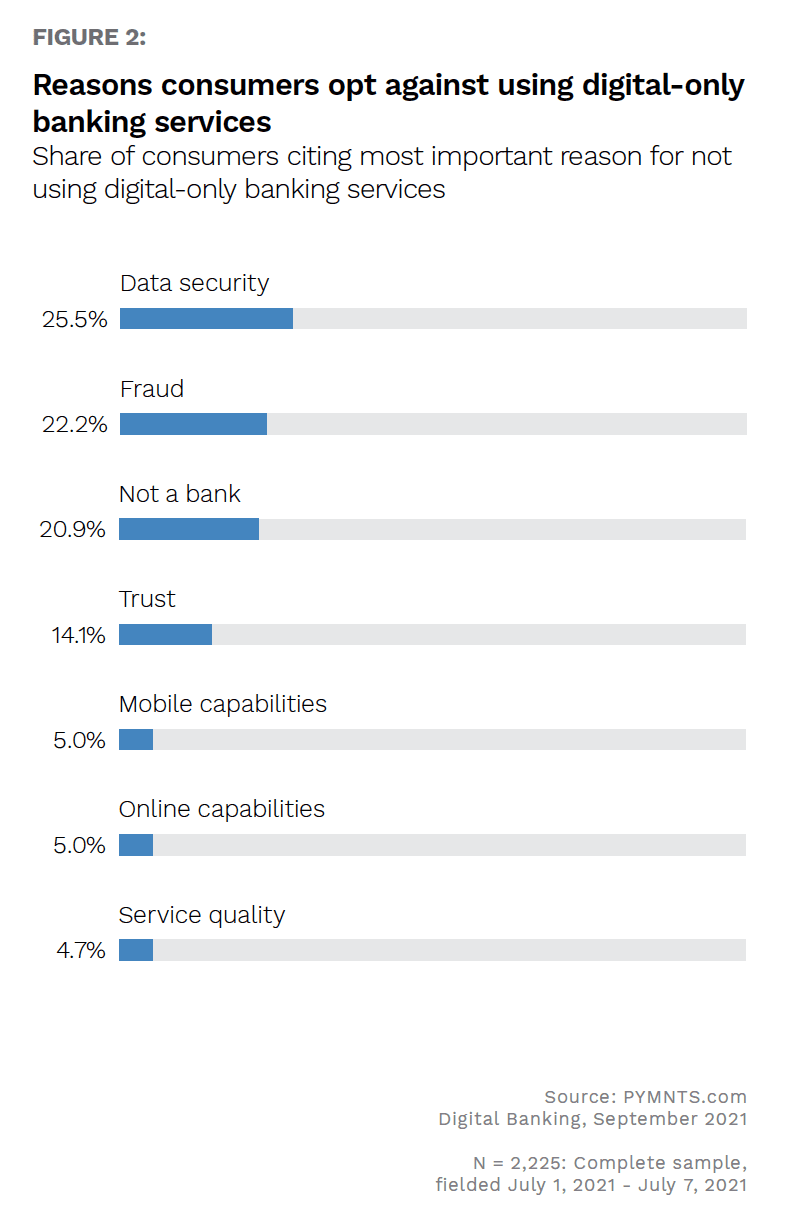

Digital banking is available to consumers from a wide variety of FIs, FinTechs and neobanks, with even the most local institutions no longer restricted by geography when it comes to gaining and retaining customers. As such, all digital banking services are offered against a field of competitors that is nearly limitless. With so many digital options from which to choose, digital-only entities’ low usage may not appear to be surprising. A deeper inspection, however, reveals that data security concerns are driving down consumers’ primary usage of digital-only banking, with 47% citing this factor as a deterrent to banking primarily with a digital-only provider.

This month, PYMNTS Intelligence takes a closer look at data security in digital-first banking, including how technology makes it more difficult to breach security and how raising consumer awareness of digital security measures could generate greater trust.

Technology Progress in Data Security

Consumers’ concerns about digital data security are well-founded. Data breaches reached unprecedented levels in 2021, with the personal identifiable information (PII) of approximately 300 million victims exposed, while identity fraud grew by 79%. With all this happening, 62% of United States consumers say they are either very or extremely concerned about the danger data breaches pose.

Nevertheless, technological solutions are making substantial progress in data security. Overall, 92% of data breaches are related to cyberattacks, and several startups are addressing this problem through behavioral biometrics. By combining multiple behavioral characteristics, companies can create a behavioral biometric profile that is nearly 100% accurate in distinguishing fraudsters from legitimate users. At the same time, behavioral biometrics do not have to be the only factor securing user data against breaches but can contribute to improved accuracy of anti-fraud stacks that include physical biometrics plus passwordless authentication.

Artificial intelligence (AI) algorithms offer another promising solution for data security by improving fraud detection. Anti-money laundering (AML) and know your customer (KYC) fraud detection are among the top use cases seeing the greatest investment. The number of FIs deploying AI for fraud detection jumped from 10% to 31% in 2022, and 75% of acquiring banks use AI to detect card transaction fraud. Along with ML, AI is one of the main technologies utilized to enhance data security without downgrading the user experience.

Consumer Trust in Digital Data Security

PYMNTS’ research points to data security as a leading concern among those consumers who say they have little or no interest in digital-only banking. This concern is especially high among baby boomers and seniors, one-third of whom cite security as a reason to opt against digital-only banking services. Moreover, 26% of all survey respondents who were uninterested in digital-only banking ranked data security as their top reason for this lack of interest. Despite this, there is still strong interest in digital-only banking among younger consumers, with 42% of bridge millennials and 41% of millennials very or extremely interested in having primary accounts with digital-only banks. Convincing consumers of digital-only accounts’ security is likely the key to making the most of this interest, however. Offering at least one security-enhancing feature was the single most important factor inspiring consumers’ trust in a financial services provider, at 83%.

PYMNTS’ research further suggests that one way to gain consumers’ trust in digital-only banking is through the use of advanced security techniques such as biometrics and passwordless login. Sixty percent of surveyed consumers said that having information about how their transactions are secured has a very or extremely big impact on their trust, and 44% said the same about the ability to log in without passwords. While 40% of consumers want easy onboarding in their online banking platforms, 30% demand biometric logins and 19% prefer no-password logins.

Digital-only banking service providers have a powerful opportunity to expand their presence in the banking market if they can demonstrate data security as well as ease of use. A failure to convince consumers of a digital-only platform’s security, however, could hinder its acceptance.