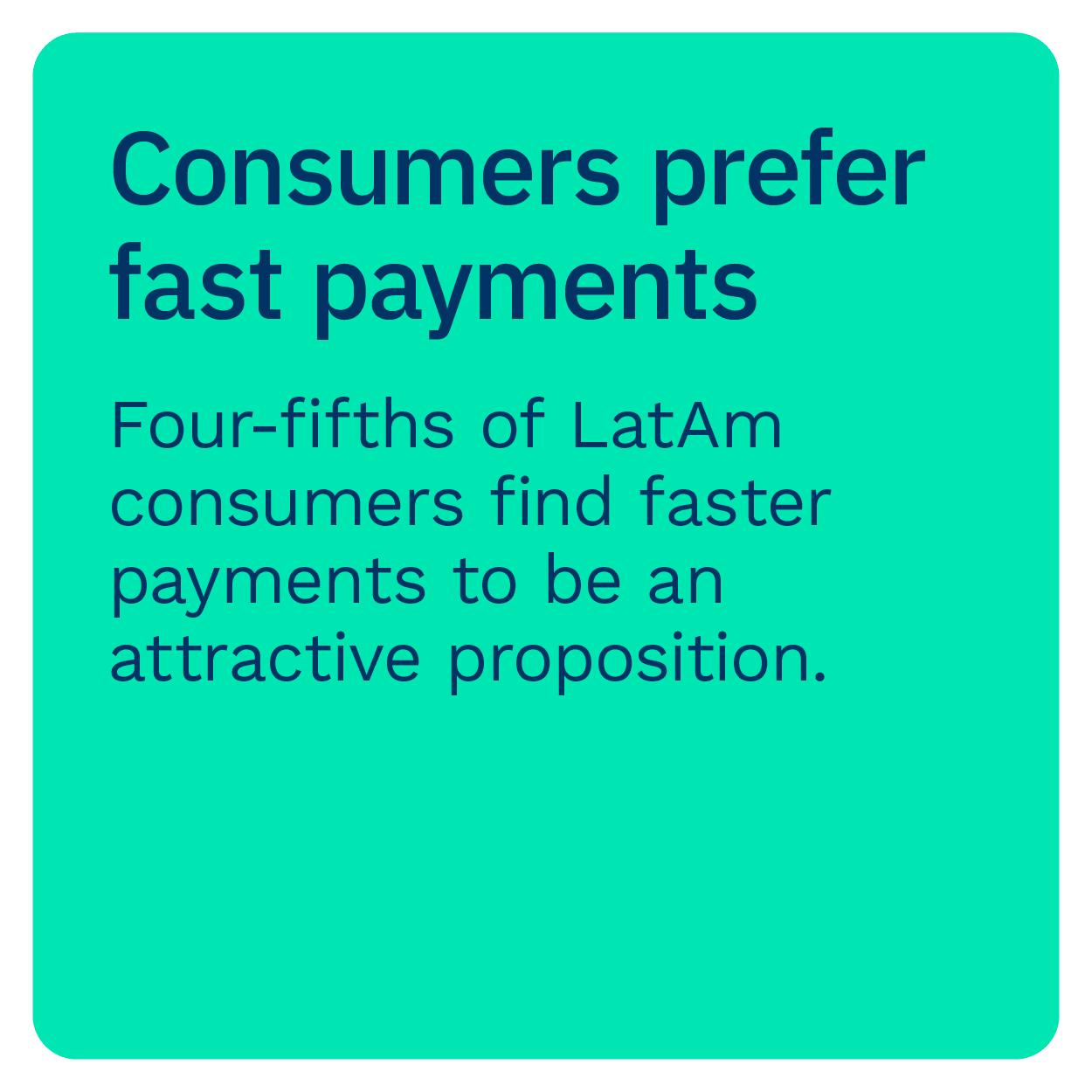

A growing number of Latin American consumers are turning to digital-first payment and banking solutions in the wake of the pandemic, with one recent report finding that 62% of consumers in the region stated they used less cash last year compared to 2019. The use of contactless credit and debit cards also rose during the same time frame, indicating a growing comfort and preference for digital options.

As alternative payment solutions have become more popular, however, Latin American financial institutions (FIs) are facing stiffer competition from emerging digital-first players to engage and retain customers. In the latest Digitizing Payments In Latin America Playbook, PYMNTS examines how Latin American consumers’ banking and payment preferences are shifting, and how legacy FIs must move to keep pace as the region’s financial ecosystem becomes more saturated.

Around the Latin American Payments Space

Legacy FIs are taking quick steps to roll out new digital solutions as banking expectations shift — for example, the Central Bank of the Argentine Republic (BCRA) Transferencia 3.0 program officially went live at the end of November. The program enables its customers to make QR code-based payments across different channels and devices, including through virtual wallets or digital banking apps that are tailored to fit users’ mobile devices. This is a move that could lead to more consumers leaving cash behind in favor of newfound digital payment methods as they become more widely available.

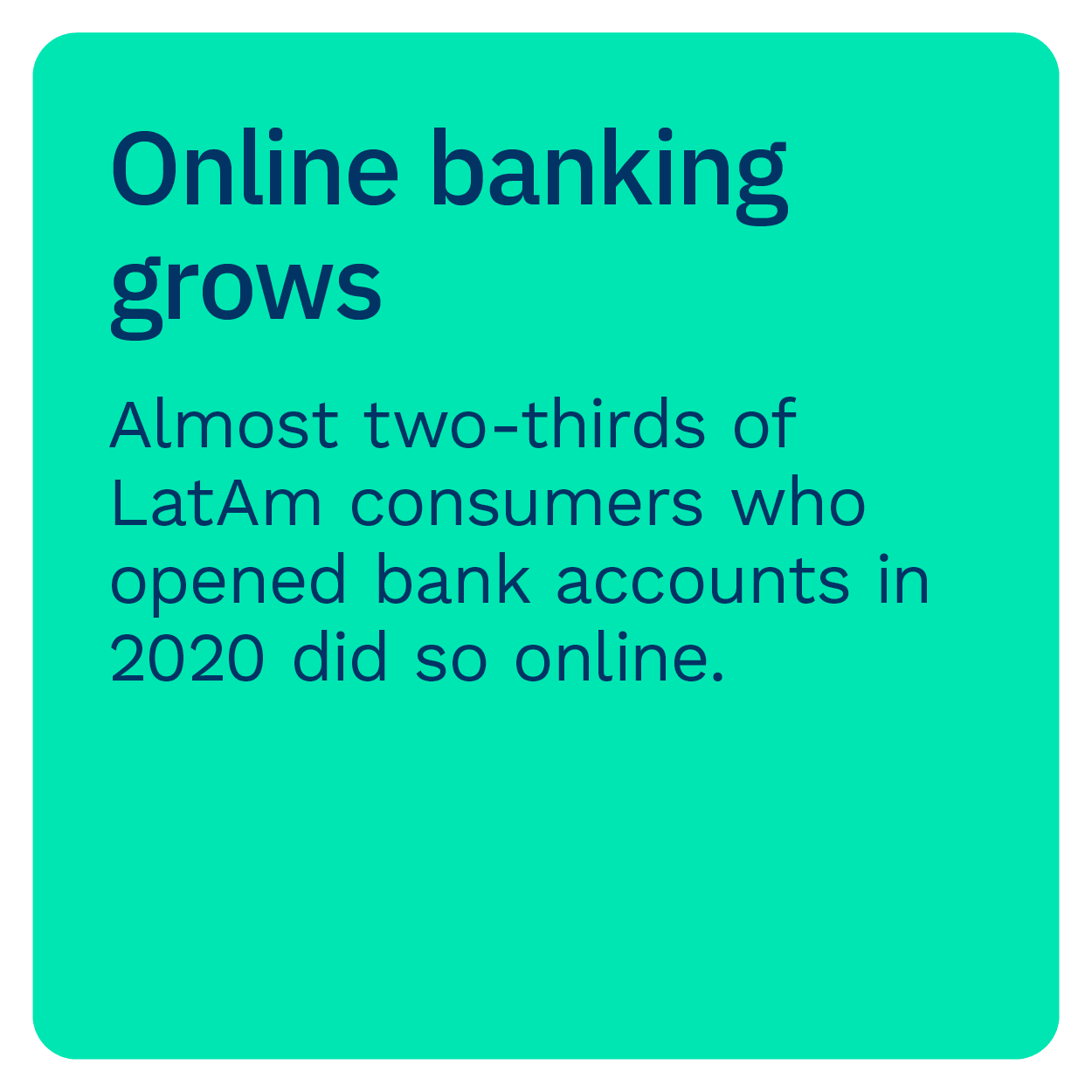

Both legacy FIs and FinTechs have a rising opportunity to engage and retain consumers’ loyalty in the region. One recent study found 40% of consumers opened bank accounts in 2020, with 60% stating they did so online. This growth in online banking sign-ups occurred at a time when many brick-and-mortar banks and businesses were shut down, but consumers have continued to gravitate toward digital channels even as public health and safety concerns eased. Keeping track of how consumers’ preferences and banking wants are continuing to shift and how they can accommodate them is therefore critical for both legacy and emerging FIs.

For more on these and other stories, visit the News and Trends.

Why Brazil’s Legacy FIs Are Struggling to Keep Pace With Consumers’ New Digital Banking Needs

The availability and popularity of digital services is expanding wit hin Latin America at a rapid rate, leading consumers who were previously dependent on cash to open bank accounts or utilize other online payment tools for the very first time. As such, a rising number of consumers are seeking out newfound digital financial experiences — but outdated infrastructure could be hampering legacy FIs’ ability to offer such solutions, explained Brad Liebmann, CEO and founder of mobile-only Brazilian FI alt.bank. To learn more about how legacy FIs may be struggling to meet Latin American consumers’ needs and what must be done for them to innovate, visit the Tracker’s Feature Story.

hin Latin America at a rapid rate, leading consumers who were previously dependent on cash to open bank accounts or utilize other online payment tools for the very first time. As such, a rising number of consumers are seeking out newfound digital financial experiences — but outdated infrastructure could be hampering legacy FIs’ ability to offer such solutions, explained Brad Liebmann, CEO and founder of mobile-only Brazilian FI alt.bank. To learn more about how legacy FIs may be struggling to meet Latin American consumers’ needs and what must be done for them to innovate, visit the Tracker’s Feature Story.

Deep Dive: How Legacy FIs Can Capture the Attention of Latin America’s Digital-First Consumers

Latin Americans may be growing more familiar with digital payment methods, but they may not be heading to legacy FIs to find them. A higher number of the region’s residents remain  unbanked even as mobile penetration ticks up, meaning many customers are interested in utilizing mobile-optimized payment methods that may run outside of the traditional banking sphere. This is putting increased pressure on legacy FIs, which must innovate their own features to keep pace with digital or mobile-first competitors. To find out more about how the payment preferences of Latin American consumers are shifting and how legacy FIs can keep pace, visit the Tracker’s Deep Dive.

unbanked even as mobile penetration ticks up, meaning many customers are interested in utilizing mobile-optimized payment methods that may run outside of the traditional banking sphere. This is putting increased pressure on legacy FIs, which must innovate their own features to keep pace with digital or mobile-first competitors. To find out more about how the payment preferences of Latin American consumers are shifting and how legacy FIs can keep pace, visit the Tracker’s Deep Dive.

About the Playbook

The Digitizing Payments In Latin America Playbook, done in collaboration with Kushki, examines the latest digital payments developments in Latin America, including how payment services providers can support consumer demands and gain a foothold within the region.