The pandemic’s onset made routine ways of conducting daily business challenging for merchants, consumers and their payment partners alike, and the impacts linger one year into the crisis. All three parties moved swiftly to adjust to this new reality, with 76 percent of businesses in one report saying that the pandemic had made them more digital and 82 percent noting that the crisis prompted them to improve how they sent or received money. The pandemic’s effect on manual payments is not the only factor that continues to drive this digital migration, however. Global revenues declined by 7 percent from 2019 levels, meaning that slow or outdated disbursement processes are no longer merely frustrating for many businesses and consumers — they now present a clear financial danger.

The global health crisis has placed a higher premium on payment speed, even above concerns such as cost. One recent PYMNTS study showed that 20 percent of consumers are now willing to pay fees to receive non-government disbursements instantly, for example, while 68 percent of payors — those sending out these funds — would also be willing to pay fixed amounts to offer this capability to their customers. This signals a rising need to access incoming funds as quickly as possible, but bringing instant payment services into the financial mainstream remains difficult as financial institutions (FIs) and payment providers look to shake off outdated payments infrastructures.

The following Deep Dive examines the progression of instant payments one year after the pandemic began as well as how consumers’ and merchants’ attitudes toward these payments have shifted. It also analyzes the remaining challenges to instant payments’ ubiquity and how merchants, banks and payment providers can work cohesively to overcome these obstacles.

Examining The Instant Payments Landscape

The pandemic had an intriguing impact on instant payments over the past year, highlighting not only their importance but also — and more notably — their absence. Consumers and businesses have expressed growing frustrations with slower disbursement methods under the pandemic’s pressures, as evidenced by a decline in the use of paper-based methods and a surge of interest in digital and real-time replacements.

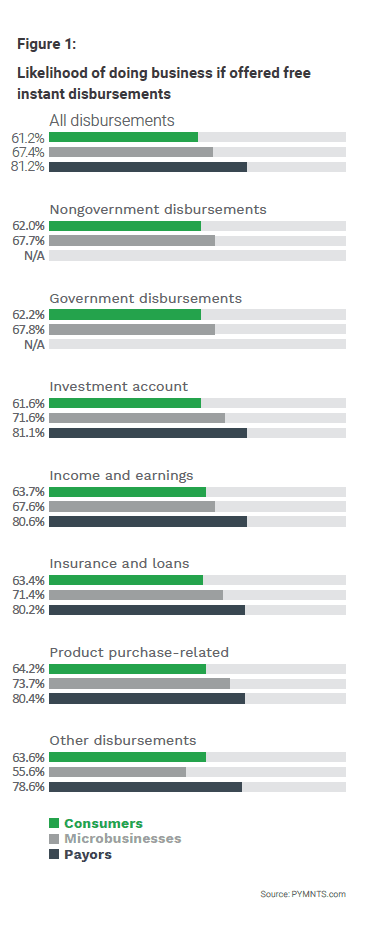

Seventy-three percent of businesses in one recent study agreed that digital payments were the “new normal” for future transactions, for example. Sixty-seven percent of small to midsize business (SMB) business owners opined, in fact, that one upside of the crisis was the push it gave them to adopt online or electronic payment solutions, with 81 percent saying these methods have increased their customers’ satisfaction. Another 67 percent of microbusinesses in a recent PYMNTS report said that access to free instant payment methods would increase their own loyalty to payors, and 61 percent of consumers said the same.

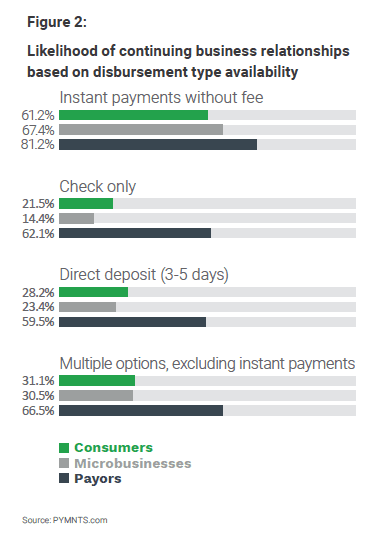

The pandemic has brought instant payments further into the financial spotlight for these groups, and this has not been lost on payors. January 2021 PYMNTS data showed that 81 percent of payors agreed that offering instant disbursements was critical to maintaining client relationships. This looks to be correct, as the study found that only 31 percent of consumers would likely continue their relationships with entities that did not offer such methods.

The pandemic may have forced payors to acknowledge instant payments’ value, but there is still a significant gap when it comes to the method’s availability. The same PYMNTS report found that only 6 percent of U.S. consumers who received disbursements in 2020 did so via instant payment services, despite all parties agreeing on their importance. Respondents also stated they were given a choice of disbursement payment methods — instant or otherwise — for only about half of the disbursements they received over the course of the year.

This is a critical gap as the pandemic continues into 2021. Addressing the lack of instant payments’ availability will require careful strategizing not only by payors but also by their FIs and payment partners.

Clarifying Instant Payment Misconceptions

There are multiple reasons why instant payments’ availability has not risen to meet their expanding popularity over the last year, including the fact that consumers may have differing ideas on what constitutes an instant payment. Recent PYMNTS data found that more than 36 percent of consumers claim to have used real-time payments even though the payments were not actually made in real time. It then falls to payors and their FIs to educate consumers on the distinction between payments that appear instant and those that truly are.

Education is only one key to true instant payment ubiquity, however. Another problem is that instant payment features are often tailored for one company’s users but not another’s, as in the example of mobile wallets. Apple Card rewards pay instantly only to Apple Cash users, just as gig employers pay their workers instantly to their own prepaid cards. This inflexibility makes collaboration difficult among payors and financial entities and slows down the payments process for users.

Addressing these gaps will be essential to supporting instant payments’ growth. Payment providers and FIs will need to work closely to determine exactly how they can weave their approaches together to present one cohesive option for clients and keep money moving at the speeds expected in the shifting payments landscape.