Consumers are increasingly dependent on digital channels for financial accounts but often still want to use nondigital channels when dealing with complex or unfamiliar areas. While 71% of surveyed consumers said they would be comfortable opening a new credit card account digitally, just 23% said the same about opening a new buy now, pay later (BNPL) account. In the case of checking and savings accounts, 62% said they are comfortable with digital account opening.

At the same time, digital banking tools are essential for many consumers, with 39% of consumers saying they rely on mobile budgeting apps to keep track of their finances, and 35% saying mobile check deposit is the most valuable feature of their primary banking app. A lack of digital savviness is not a significant issue among those reluctant to open new accounts through digital channels. The answer may be in finding ways to educate consumers about digital account-opening tools and the types of accounts they are opening to ensure a greater level of comfort.

In the latest Money Mobility Tracker®, PYMNTS examines why FinTechs and neobanks will have to be adept at navigating not only the regulatory and logistical hurdles of financial systems but also at finding the right financial partners and opportunities to enhance their own capabilities.

Around the Money Mobility Space

As workers struggle under continuing economic pressures, the idea of receiving more frequent paychecks is growing in popularity. Seventy-six percent of surveyed hotel and food workers say they would consider changing jobs if another employer offered payment options that allowed them to get paid more frequently. The same is true of 51% of all surveyed workers. A 7.5% inflation rate coupled with other economic factors has 62% of respondents saying that they are concerned their wage increases will not keep up with the growing cost of living. When workers feel insecure in their financial situations, things that give them a greater sense of control, such as being able to choose when they get paid, may help in handling that added stress.

Workers are not the only ones who would like more predictability in when they are paid. Small to mid-sized businesses (SMBs) are still combating late ad-hoc payment problems in business-to-business (B2B) transactions. SMBs collectively spend $28 billion providing discounts and other incentives to encourage on-time or early one-time supplier payments. At the same time, one-third of ad hoc vendor payments for which discounts are offered still arrive late, and another third are paid on time rather than early to secure discounts. Even in the case of invoice payments for consulting services and products solely to other businesses, which are the most likely SMB B2B ad hoc payments to be made on time, more than one-quarter are still received late.

Workers are not the only ones who would like more predictability in when they are paid. Small to mid-sized businesses (SMBs) are still combating late ad-hoc payment problems in business-to-business (B2B) transactions. SMBs collectively spend $28 billion providing discounts and other incentives to encourage on-time or early one-time supplier payments. At the same time, one-third of ad hoc vendor payments for which discounts are offered still arrive late, and another third are paid on time rather than early to secure discounts. Even in the case of invoice payments for consulting services and products solely to other businesses, which are the most likely SMB B2B ad hoc payments to be made on time, more than one-quarter are still received late.

For more on these stories and other Money Mobility developments, check out the Tracker’s News and Trends section.

Wise on Powering Instant Transfers in a Non-Instant World

There is often no straightforward path when moving money into accounts, and that problem is only exacerbated when the money needs to move across borders.

In this month’s Feature Story, Sharon Kean, global expansion senior product director for Wise, talks about how the money transfer FinTech speeds up global money transfers while navigating disparate financial schemes and partnerships.

PYMNTS Intelligence: Navigating the Money-In Side Of Money Mobility

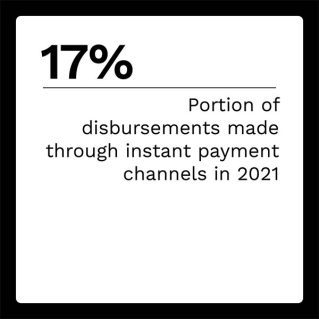

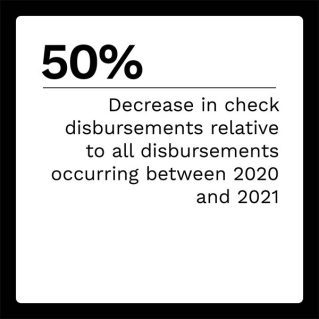

As instant disbursements become more common, even promising to surpass same-day automated clearing house (ACH) disbursements, consumers also face rising economic pressures that add urgency to their desire for speedier and more reliable money mobility. Additionally, consumers have a growing variety of options for account types and do not want to wait days to fund one account from another. With consumers able to access various account types from a single mobile device, the inability to move funds easily between those accounts is thrown into stark relief when they can instantly transfer money to someone else’s account.

This month’s PYMNTS Intelligence looks at the money mobility developments and consumer preferences that are mutually shaping one another and the challenges FinTechs and neobanks face ensuring money-in mobility keeps up.

About the Tracker

The Money Mobility Tracker®, a PYMNTS and Ingo Money collaboration, examines the latest trends and developments shaping the money-in side of the Money Mobility space, from consumer habits and preferences to the regulatory and logistical hurdles of getting money into accounts.