It goes the other way, too: Annoyed, frustrated and angry consumers can use the tools of digital life to complain about, and perhaps even take down, a business that fails to satisfy — and honor the virtue of loyalty. Few things travel as quickly as bad news, such as a negative story or juicy anecdote about rude or incompetent customer service (which, after all, gives people the basic human joy of shouting down real or perceived injustice, a long-standing use of popular narrative).

Woe to the merchant that fails to respect that.

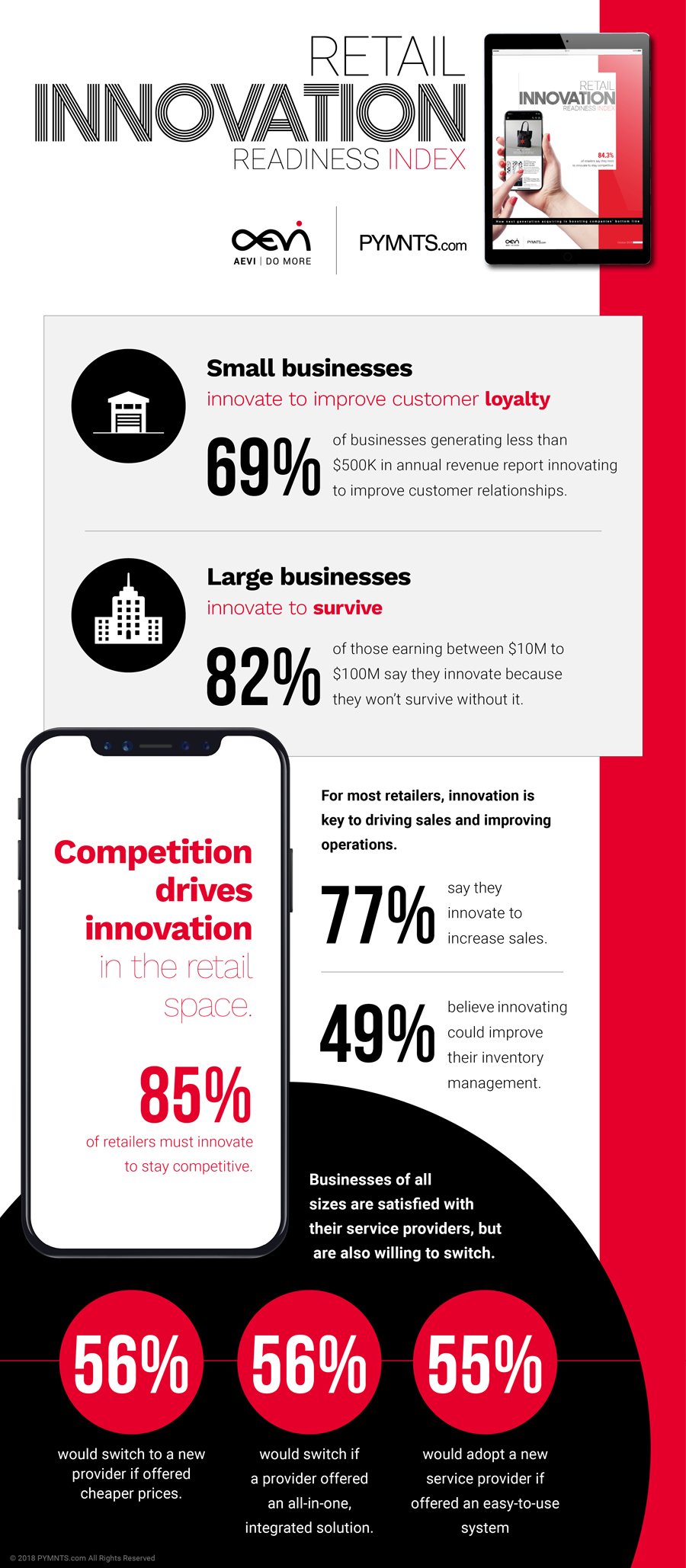

Still, it’s striking — or, perhaps, significantly hopeful, in a retail sense — that 65.4 percent of retailers have said they innovate to improve customer loyalty. That, in fact, is one of the main findings in the new Retail Innovation Readiness Index from PYMNTS, powered by FinTech firm AEVI.

As AEVI CEO Mike Camerling said during a discussion with Karen Webster that dug deep into the report, “Many businesses still have the [outlook] of years ago, when you could say, ‘OK, there will be another customer,’” if one leaves and breaks that tie of loyalty. Things have changed, though, he said — one reason why that innovation finding carries such weight.

“I think humans have become much more unforgiving, and will just say, ‘I’ll go somewhere else,’” he added, if a merchant does not pay proper attention to loyalty — and has not deployed or upgraded technology and business processes with that trait top of mind.

Innovation Divide

Easier said than done, of course, especially for smaller businesses (SMBs) — the PYMNTS-AEVI report surveyed more than 400 retailers across nine different sectors to gauge innovation readiness. There is still an innovation divide that is based on company size. That may carry a whiff of obviousness, but recent changes — again, mainly via digital retail, payments and marketing tools — make that divide seem different than it might have a generation ago.

“For many years, innovation has … been there for the Tier One and Tier Two” firms, Camerling said.

That’s because IT and other parts of innovation were expensive and out of reach for many smaller merchants, especially those who were experts in their core area of retail (say, a person who builds high-end bicycles, or a florist), but had little time or interest for the marketing and payments side of the operation.

“Times have changed,” he told Webster. “Everything now is about apps, and there is a huge choice of solutions.”

In fact, according to his view, the main innovation issue for these smaller businesses has changed from something along the lines of, “I can’t do this,” to a view that asks, “Which solution is best for my business, and how do I choose the right combination?”

That said, about 88 percent of smaller businesses surveyed for the Index believe that innovation is essential for survival. That means, at the least, the idea of innovation in this digital payments and commerce world has taken root, even among those businesses that might need more of a helping hand to achieve innovation than bigger retailers.

However, the ways to innovate can differ significantly — and that brings us to the relationship that payments have with retail innovation in 2018, and will have in the years to come.

Payments Drives Innovation

Take payments: Of the top 60 performing firms in the new report, 81 percent said they underwent innovation to meet customer demand for new payment methods — consumers are making moves beyond cash and cards, and merchants are responding to that. Only 47 percent of the middle 60 firms said the same, and not one retailer in the bottom 60 cited payments as fuel for innovation. Generally, 56 percent of business innovation is driven by customer demand for more payment options.

As Camerling explained, though, payments innovation is not just about payments (which, after all, represent the goal that all retailers are working toward). He proposed taking a wider, more comprehensive view that reflects the realities of the digital age, which can serve as a kind of north star for innovation: Instead of the term “point of sale,” why not “point of interaction?”

Viewing innovation and new technology that way — and the increasing shift to mobile is helping to make this possible — can, he said, “enable people to run the businesses the way they really want to run” them, instead of via the parameters of the retail and payment solutions they have bought or licensed from others. “Turn a point of interaction into a payments capable device,” he said.

Innovation And Security

Grand ideas often give way to nagging details, and that’s the case with this new innovation report, though the full implications are not yet clear.

The report found that only 37 percent of businesses have said their innovation efforts are driven by data security concerns. At first glance, that seems almost outlandish (reckless, even) — given the frequency of breaches and cyberattacks, the well-documented increase in the sophistication of fraudsters and other online criminals, and the clear financial and reputational damage that an attack can cause.

That finding, however, is probably more a reflection of awareness — or lack thereof, to be exact — than carelessness.

Webster and Camerling said many of the survey respondents might assume that security is locked up via the business relationships they have with their technology providers, or, as Camerling said, smaller firms “might think [data security] is more of a topic for big businesses.” Indeed, he talked about small business response to the months-old General Data Protection Regulation (GDPR) in Europe, and told Webster that many smaller firms don’t seem to think the new privacy and security regime will have any impact on them. (It will. It does.)

The new report paints a detailed picture of what is, and what will keep, driving retail innovation — a topic that involves not only merchants, of course, but payment service providers, marketers and other participants in the retail and eCommerce ecosystems. Payments and loyalty will continue as significant drivers, but the innovation story certainly contains more nuances and angles than that.

Key findings from the PYMNTS Retail Innovation Readiness Index: