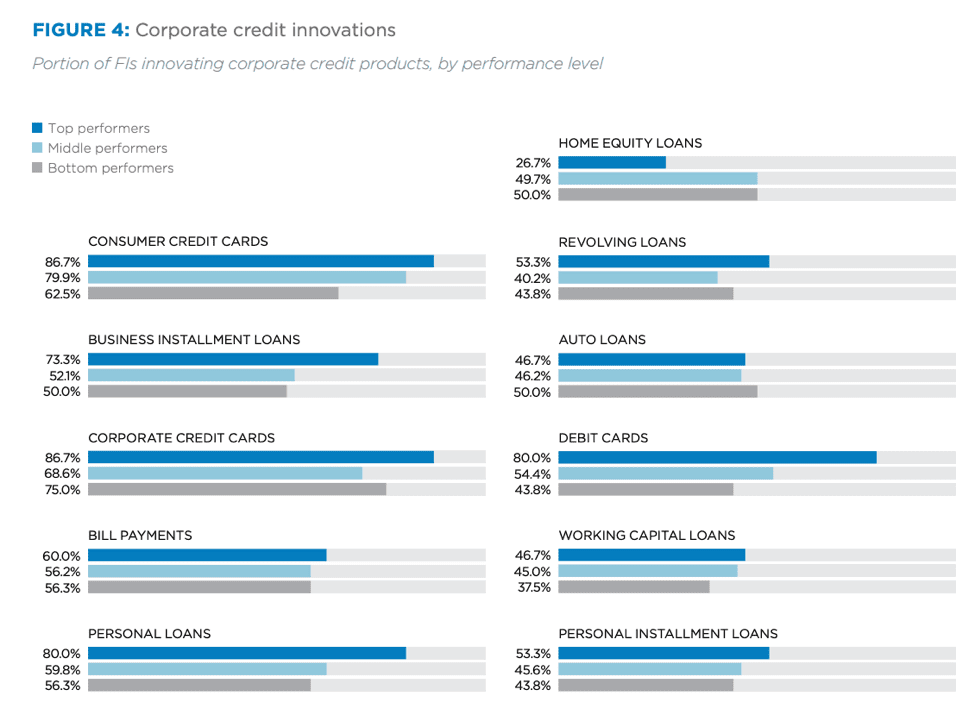

According to the latest Innovation Readiness Playbook, corporate credit plays a pivotal role among FIs and is an innovation priority, especially among top performers; 86.7 percent are investing in corporate credit cards.

Firms earning more than $500 million annually were investing more in credit products than lower performers. They also had high levels of innovation in personal loans and debit cards (both at 80 percent).

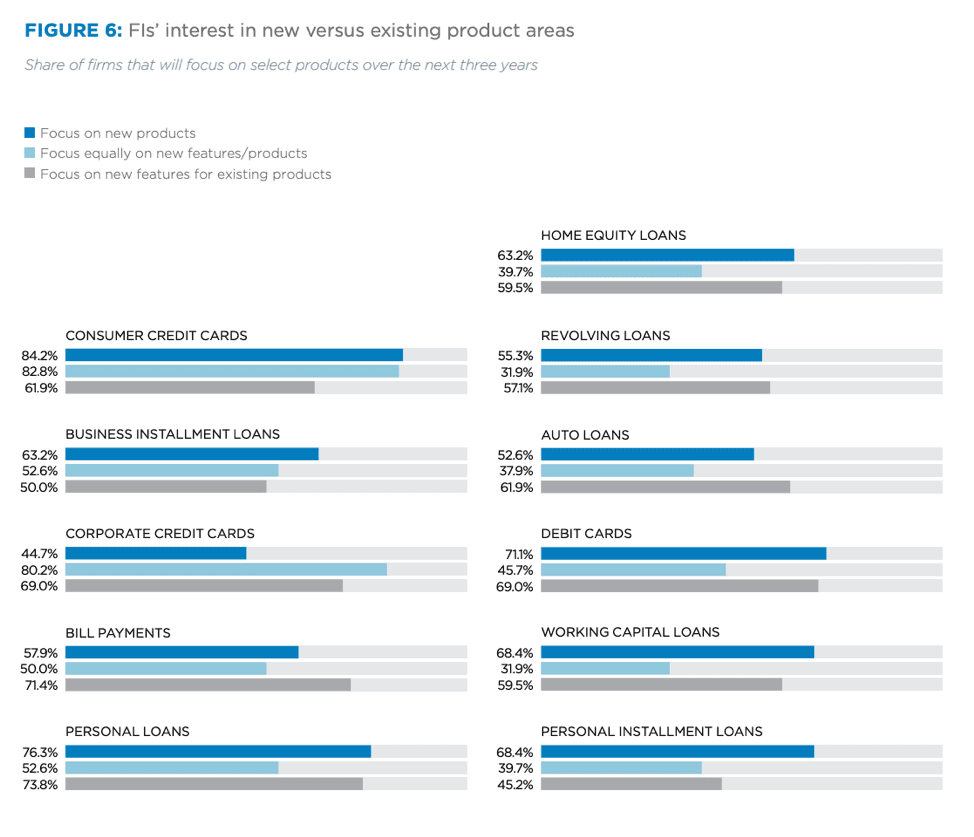

Whether FIs place priority on new products or new features is determined by business size. In the past three years, just 6.7 percent of top performers said they have focused on new products, indicating a slowdown of the pace of innovation. More top performers (8.8 percent) reported focusing equally on new products and new features. Bottom performers (13.3 percent) were more likely to invest in new features for existing products than firms at the top (3.3 percent).

Consumer credit cards were the product type with the most interest in launching new products (84.2 percent), followed by personal loans (76.3 percent) and debit cards (71.1 percent). Personal loans had nearly the same level of interest (73.8 percent) among FIs focusing on new features for existing products, while bill payments had a high level (71.4 percent) among those focused on new features for current products.

Over the past three years, interest levels in innovative features have shifted. Among digital wallets (56.7 percent) and mobile offers (53.3 percent), a majority focused on new products, and half focused on P2P payments as new features for existing products. Mobile clearly is top of mind for all levels of innovation.

Over the past three years, interest levels in innovative features have shifted. Among digital wallets (56.7 percent) and mobile offers (53.3 percent), a majority focused on new products, and half focused on P2P payments as new features for existing products. Mobile clearly is top of mind for all levels of innovation.

Looking forward three years, there is more future interest in offering new P2P payments (68.4 percent) and contactless payments (34.2 percent) products than in the past.

Digital wallets remain a popular area for new products in the near future, as 52.6 percent plan to focus on them.

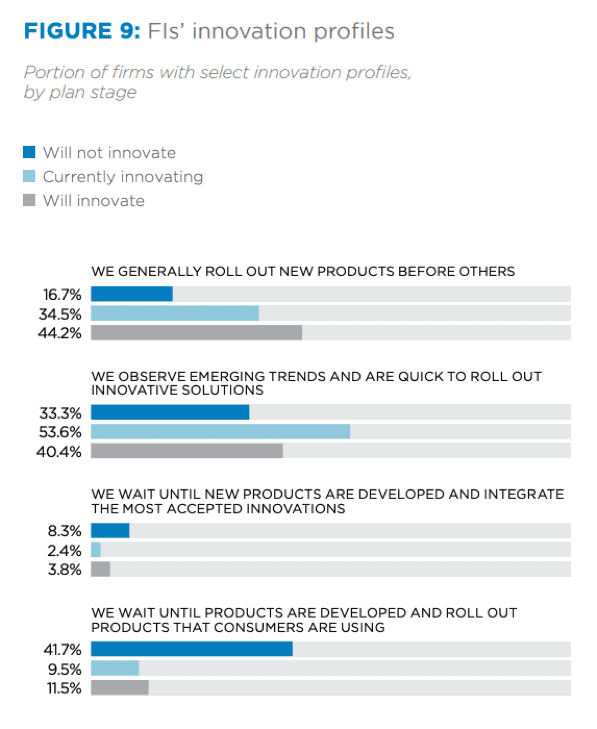

Despite pressure to innovate, many FIs are taking a slow, measured approach. More than half (53.6 percent) of those currently innovating said they observe emerging trends before rolling out innovations. Far fewer (34.5 percent) said they prefer to launch new products ahead of the competition.

Not surprisingly, FIs with no innovation plans were also the most likely (41.7 percent) to wait until products are developed and to launch products consumers are already using.

What’s driving this innovation? Among those with future innovation plans, 75 percent are motivated by changing consumer behaviors. Responding to existing client needs was important to this group (49 percent), as well as the current innovators (45.2 percent). Looking forward, both current (61.9 percent) and future (66.3 percent) innovators were more motivated by potential clients’ needs, though. The firms more amenable to innovation were also more forward-looking, and wanted to anticipate what future clients might want.

What all FIs had in common was IT infrastructure as the leading barrier to innovation. Budgetary constraints were a larger challenge (36.4 percent) for FIs with no innovation plans.

By institution type, credit unions were more likely to cite inflexible tech systems (56 percent) than commercial banks (26.1 percent) or community banks (44.2 percent). Commercial banks were more likely to be hampered by regulations (32.6 percent). Community banks cited lack of management focus (23.1 percent) more than the others. Even so, community banks have been innovating on the corporate credit front.

All of these factors are important, but the shared technological barriers are particularly notable. Banks will have to overcome those to stay competitive with FinTech firms that are encroaching upon traditional financial institutions’ space.

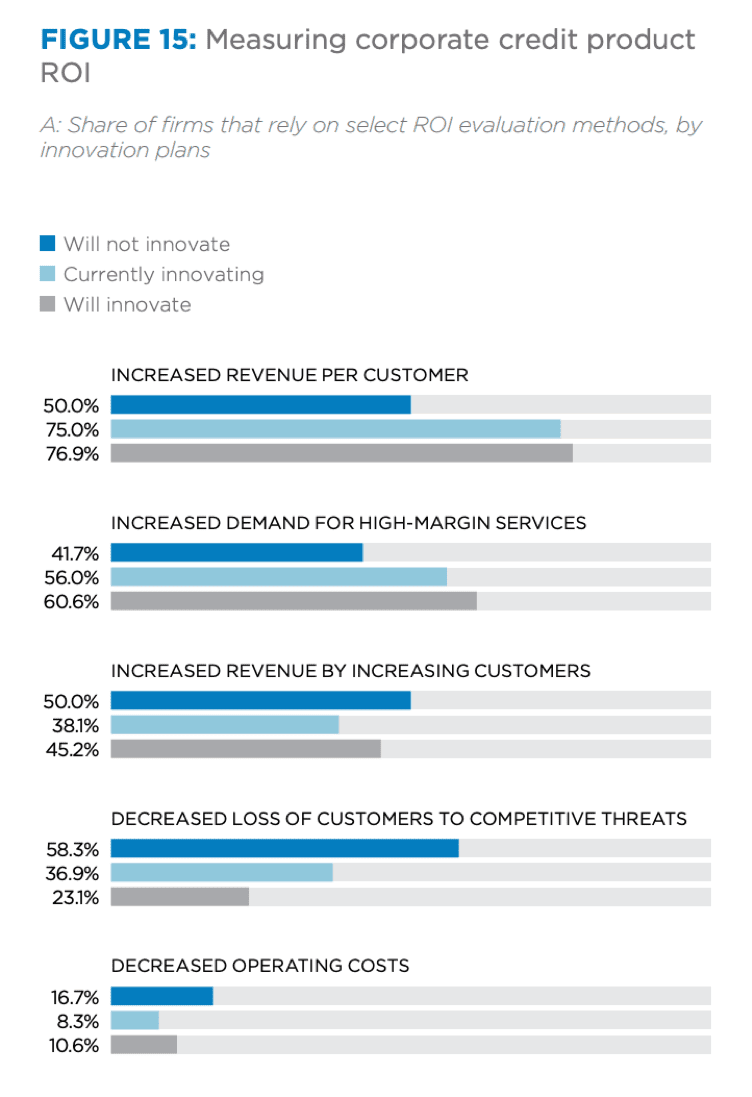

FIs across innovation levels were also on the same page for measuring ROI. The increase in revenue per customer was cited by 75 percent of current and 76.9 percent of future innovators as the most common indicator of success. Increased demand for high-margin services was also a measure of success for a majority of current (56 percent) and future innovators (60.6 percent).

FIs with no innovation plans had more passive criteria for success; half cited increased revenue by growing customers, and 58.3 percent named decreased loss of customers due to competitive threats. Losing fewer customers might seem more like treading water than as a true sign of success. Firms that embrace innovation appear to hold themselves to higher standards.