The Paycheck Protection Program (PPP) has a problem with its forgiveness program, according to the Credit Union National Association (CUNA), which wrote to the House Small Business Committee for its hearing on SBA pandemic response programs. A lot of funds have gone out, CUNA affirms, but there is a significant backlog of forgiveness applications still waiting for a response from the Small Business Administration (SBA).

“Under the SBA’s own Interim Final Rule, the SBA is required to issue a decision within 90 days after a forgiveness application has been received. Despite the Interim Final Rule, businesses and financial institutions are waiting well past the deadline for a response,” the letter reads.

“While we understand there is a high volume of loan forgiveness applications, small businesses and financial institutions need certainty on the status of their applications. We urge SBA to address these delays with loans forgiveness applications and to ensure that SBA has adequate staff in place to provide customer service in the upcoming months.”

CUNA also recommended the fast passage of bipartisan legislation that would exempt credit union member business loans from the cap for up to one year past the declared national emergency. Removing that MBL cap, according to CUNA will provide more than $5.5 billion in capital to small and informal business ventures. Said infusion of additional funds, the organization wrote to Congress, could create as many as 50,000 jobs over the course of the next year.

“Providing credit unions flexibility to temporarily exceed the MBL cap would not only provide small businesses and consumers with the assistance they need immediately, but also stimulate the economy in the long term.”

CUNA’s letter is the latest in a string of issues springing for the latest round of PPP funds to flow out to small and medium-sized businesses (SMBs) nationwide. Late last month, the Senate voted to extend the Paycheck Protection Program until the end of May, giving businesses more time to apply and the government more time to process the requests.

The legislation, which went on to be signed into law by President Biden, gave the SBA another 30 days beyond May 31 to complete processing loan applications, Reuters reported. Changes to the program when the second round went out in February made the PPP more accessible to gig workers and sole proprietors, along with the smallest of SMBs, PYMNTS reported.

That was a response to complaints about earlier rounds of the PPP, which often ended up excluding the truly small businesses, as they were disadvantaged when it came to collecting. Despite representing 98 percent of U.S. SMBs, the businesses with less than 20 employees only got 45 percent of the funds.

Though how much funding actually got into the hands of SMBs during this second round, according to PYMNTS data, seem to be another issue entirely. The government’s clear intention with the changes made for the second round was to make the funding more easily available to SMBs — but PYMNTS SMB survey data indicates that availability was still pretty narrow.

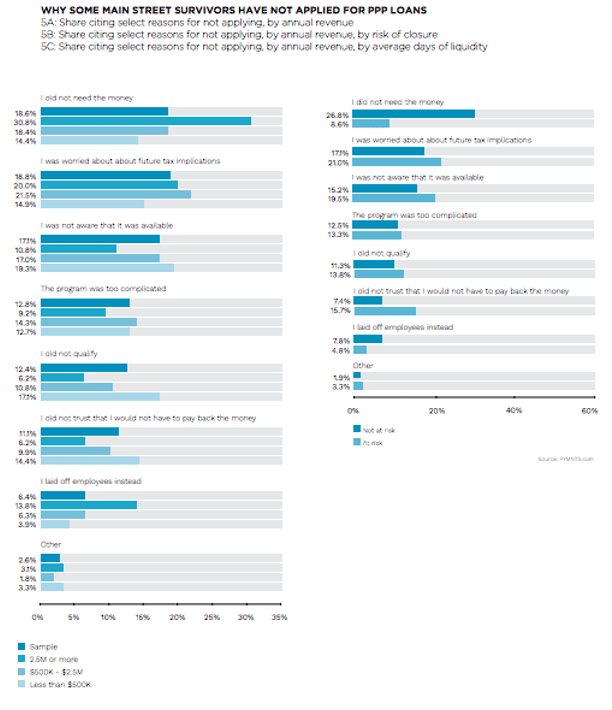

Only 16 percent of Main Street Survivors reported having applied for PPP assistance in early 2021, compared to an average 21 percent that had done so since March 2020. The 84 percent of Main Street Survivors that have not applied for PPP loans cite several reasons as to why they didn’t.

PYMNTS research shows that 19 percent of survivors did not apply for PPP loans because they worry about the implications it might have on their future taxes, while 11 percent are simply unsure whether they will make enough revenue to return the funds they might receive from such programs.

In addition, many do not realize PPP loans are available at all — with 17 percent of surveyed survivors reporting being unaware such loans were available.

There was also the reality that many of those survivor merchants surveyed felt they did not need the money. This reasoning is particularly common among Main Street Survivors that generate more than $2.5 million in annual revenue, with 31 percent reporting they had not applied because they feel they are financially stable enough to not need PPP loans. In comparison, 14 percent of Main Street Survivors that generate less than $500,000 in annual revenue and did not apply felt the same. Many merchants, according to the data, also opted to lay off staff rather than take the loan funding. This is especially common among those generating less than $500,000 in annual revenue, 14 percent of which opted to lay off their employees instead of applying for a loan.

And as PPP reimbursement is being called out as in need of a tune-up by CUNA, it is worth remembering that as of this week Federal Reserve economists in a new report have concluded the number of businesses that permanently closed during the first year of the pandemic fell short of widespread concerns.

“Relative to popular discussion, then, our results may represent an optimistic update to views about pandemic-related business failure,” the authors wrote.

Closures, the authors note, are hard to track in a timely way, but by leveraging alternative data sources they were able to conclude that the worst predictions made in the pandemic’s early days have not been borne out in the data.

“Business electricity accounts show little imprint of the recent economic stress while vacancy rates for office and retail are reaching levels last seen during the Great Recession. Similarly, defaults have jumped, but both ‘going out of business’ search queries from Google and 30-day defaults have returned to trend after brief elevation,” the report said.

The authors estimated that fewer than 200,000 businesses beyond the number that normally would close shut down during the first year of the pandemic. The failure rate for businesses was between 25 percent and 30 percent above normal, they concluded. A disturbing outcome, but not quite the apocalypse forecast early on, and as data from PYMNTS and elsewhere demonstrates, it is an outcome SMBs are starting to walk back from.

Read More On Loans: