The problem with building financial inclusion — particularly in a developing world context — is that it is a tough goal to pursue directly. While there isn’t much in the way of disagreement that more should be done to connect the approximately 2.5 billion adults who are totally (or nearly totally) detached from formal financial services, actually implementing a plan that actually makes a difference is often a very separate matter.

Unlike financial inclusion efforts in the more developed world — where there is a good deal of existing financial and commerce infrastructure to leverage — the developing world financial inclusion issues are threaded throughout a host of other local issues. Which, according to John Sheldon, Senior Vice President, Innovation Management for Mastercard Labs, means that solving for financial inclusion in the developing world often means working somewhat laterally on the problem.

“What we are trying to do is impact big populations and solve big problems. You aren’t going to just solve financial inclusion by just offering better financial products. Those products have to exist in a context. You have to go after big problems and embed financial tolls in the solutions.”

Which is how Mastercard finds itself announcing the launch of the 2KUZE platform. Named for a Swahili phrase roughly translated to “Let’s grow together,” 2KUZE is a mobile marketplace for East Africa’s agricultural sector.

So, what is it, and how does it work?

2KUZE

Developed at the Mastercard Labs for Financial Inclusion in Nairobi and funded by a grant from the Bill & Melinda Gates Foundation, 2KUZE is designed to reach the 80 percent of farmers in Africa that are currently classed as smallholder farms, working one to two acres of land. Farmers who are at something of a disadvantage in the marketplace today, according to Sheldon.

“In some cases, the farmers are getting less than 50 percent of the wholesale value of their goods,” he noted. “And actually this problem hits female-run farms much harder because they often have other household duties that prevent them from getting to the marketplace, so they are pretty much stuck with whatever price someone comes by and offers.”

Plus, Sheldon noted, the farmer sellers aren’t the only losers in this equation. Buyers are often unable to get the goods they want in the volume they want because middlemen agents in the process are depressing what goods locals grow. 2KUZE is meant to open up another option, and it is is being launched in partnership with Cafédirect Producers’ Foundation, a nonprofit organization working with 300,000 smallholder farmers globally.

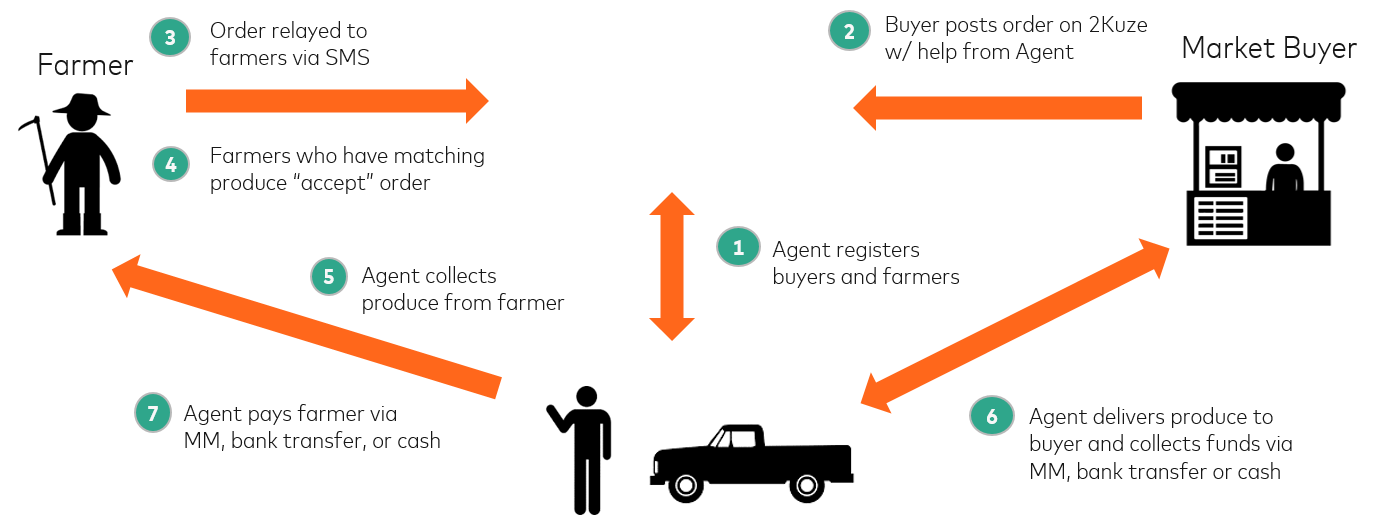

“The way it works is we’ve registered a number of buyers on the system who can then post their demand through the system. The agent can then send an SMS to the farmer. The farmers can then respond they have materials and accept the bid. The agent then does the aggregation piece and handles the collection points for the buyer.”

The goal is that everyone takes something. The agent gets paid — but a fair commission. The seller gets their goods sold — without having to make a trip to the market. And the buyer gets access to the sellers through an easy-to-use digital market.

“A key element in this is that we aren’t disrupting one of the key elements of the current supply chain. We are working through an agent in this process, and the agent does have a smartphone,” Sheldon explained. “But because we are working with vetted and trusted farmer family agents, who have as a mission the maximum value to farmers, we are seeing much better outcomes as opposed to where middlemen are taking out a disproportionate amount of value.”

Solving The Bigger Problem

The 2KUZE platform uses financial services to solve a nonfinancial service problem by making it possible for farmers to conduct the entire transaction of selling produce and receiving payments via their feature phones.

It makes the commerce easier, Sheldon noted, but it also makes it smoother because it makes the process more transparent.

“What I like is that a farmer is going to see the price that it was bought for and sold for. And if an agent wants to rip the farmer off once, they can, but doing it again won’t be so easy.”

And more than solve that problem, it also helps the farmer develop something that smallholder farmers have a difficult time creating in an environment with a dearth of financial services options — a financial history.

“For the first time ever, we are logging these transactions for the farmer. The farmers have been invisible, and it becomes a problem when they are, say, looking for a microloan to plant a new crop. They now have a history of transactions that they are able to build up. This is now a trusted financial system, and that can be used for risk assessment.”

Because, much though we might like it to be otherwise, financial inclusion, particularly on a global scale, has no easy answers on offer — just a series of problems to be solved with better tools.

But Mastercard Labs is all about the solutions, and Sheldon noted that its work with African farmers is just the beginning of what’s coming in 2017.

We promise to keep you posted as it unfolds.