LevelUp stirred the pot in 2012 when it launched with its “Interchange Zero” campaign. Moving money, said LevelUp’s Chief Ninja, Seth Priebatsch at the time, was pretty much a commodity and of little value. (Well, he actually said no value, but I sort of disagree with that. Moving money is really valuable, it’s just that a lot of people are in the business of doing it and so it has become a commodity.) Seth felt strongly that the real value of any mobile payments provider was in their ability to track customers and capture data about their transactions; data that could be mashed up with other data, like the weather, to deliver targeted campaigns that helped merchants drive more foot traffic – and therefore, more dollars, into their stores. And, of course using the mobile device to enable all of that, including payment at the point of sale.

So, LevelUp’s merchant proposition since day one has been “free” payment processing in exchange for merchants embracing a new business model, one that monetizes the face value of a loyalty redemption based on accrued spend levels at a particular LevelUp merchant. LevelUp’s pitch to a merchant was to pay them zero for processing and then something only when it was proven that LevelUp was delivering incremental customer spend to them. In the early days, that was 40 percent of the value of the redeemed offer.

So, it was on that premise that Seth and LevelUp waged a one company war on processing fees. Today, LevelUp announces a new strategic maneuver: a permanent and voluntary reduction in processing fees to its merchants. It’s a small one, from the 2.00 percent that its held constant since 2012 to 1.95 percent but one that LevelUp says makes good on its promise to permanently lower the cost of payments processing for its merchants.

The other real news here though is that for the first time, LevelUp isn’t under water in the payments processing fee department. They offered merchants a sweetheart deal from the start hoping against hope that they could drive their processing costs down enough not to lose money forever.

The other real news here though is that for the first time, LevelUp isn’t under water in the payments processing fee department. They offered merchants a sweetheart deal from the start hoping against hope that they could drive their processing costs down enough not to lose money forever.

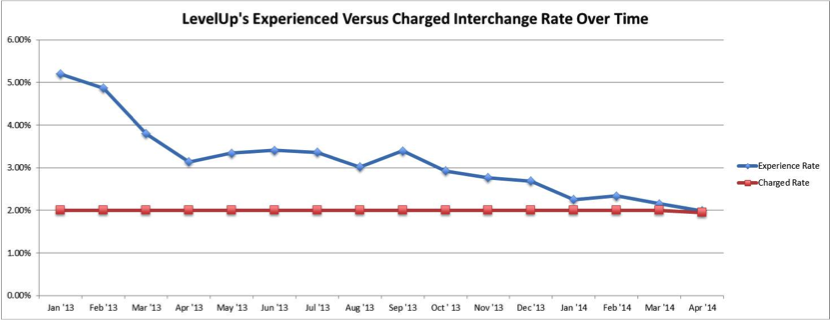

This chart shows real data from LevelUp. As you can see, it was sucking wind big time in the processing fees department while keeping a flat 2 percent rate to its merchants who wanted only to use LevelUp for mobile payments processing. As a (new/risky) merchant of record servicing (small/high risk) merchant segments, LevelUp paid the proverbial motherlode in processing costs which was ~ 5.5 percent back in 2013. It doesn’t take Warren Buffett to see that the spread between what LevelUp was paying (5.5 percent) and what its merchant customers was paying (2 percent) was not exactly the stuff that Boards, investors and otherwise sane business people would warmly embrace, much less tolerate for long stretches of time.

But Seth and team were convinced that they could refine their risk algorithms and do other clever stuff to reduce processing fees so that as he continued to pursue his “payments processing should be free” mantra his balance sheet wouldn’t be completely dominated by red ink.

So, he decided to do a couple of things.

First, he decided to take a page out of Apple’s book and started to bundle transactions. In order to do this well – basically take on this customer risk – LevelUp had to get really smart about its consumer users. And, it did. It knew that its typical user used the LevelUp app 5 times a month and its super users 4 times a week. It also knew how much they spent, on average. So LevelUp began to group LevelUp charges together and bill customers once a month, sort of like a subscription to LevelUp. It got its consumers into the habit of seeing charges for all of their LevelUp activity once a month around the same time instead of as the app was used.

That reduced swipe fees, which helped to chip away at his processing costs over time. LevelUp also observed, remarkably, that its customers most often attached their debit cards to their LevelUp accounts and not their credit cards. That helped a whole lot, too as did its tokenized security process that kept fraud in check.

LevelUp’s mission then became getting more merchants on its network, more consumers to use its mobile app more often and then more merchants to run campaigns. The little blips on the chart show what happens when a bunch of new users came into the LevelUp system – rates go up – and how once they get their LevelUp groove on, they head south again. Seth says that they know pretty much right away if a consumer will be a super user or just a regular user, and that within 4 to 8 weeks if LevelUp isn’t driving 20 percent of the business at that merchant then something is seriously wrong – that’s at the low end of what he says merchants experience.

LevelUp’s mission is, of course, to get merchants to run campaigns –that’s their only and big money maker. It now earns 25 cents for every dollar of promotional credit that a customer redeems. But running campaigns isn’t mandatory. In fact, Seth says that he no longer has his sales guys go into the merchant with the advertising sales pitch as the “be all/end all” proposition. He says that small merchants are flipping burgers with one hand while managing the books on the other and a 2 percent, now 1.95 percent processing fee is about all they can absorb and more than enough to get them interested in signing on and getting consumers to adopt. The up-sell – the pitch for campaigns that drive lunchtime users in for breakfast and customers off their keisters on a rainy day and into the store for a cuppa joe come after they’ve gathered a little bit of data on users and can help the owner organize something relevant.

Helping drive volume and campaigns is also LevelUp’s hope for its relatively newly launched developer platform which allows LevelUp to be white labeled to merchants and/or anyone with a desire to tie rewards and payment to a connected device. There are now something like 100 apps in the Apple apps store running the LevelUp application and, they say, more to come.

Seth says that this brand new payments processing fee reduction, while small, is a tangible sign of what he views as his commitment to keeping his promise to make payments free. Now, there are, of course, a bunch of things that could really mess things up for LevelUp’s grand plan. Like a raft of new users with American Express cards that swarm the LevelUp network or a new Congress that repeals Durbin so debit rates climb again – both seem a bit unlikely. Or that it turns out to be a lot harder to move consumers longer term to an ACH model which really would reduce LevelUp’s costs.

What could really throw the kahuna of all monkey wrenches into the works is if too many merchants or its white label partners decide that LevelUp is the cheapest payments processor in town but don’t ever run campaigns. That “I’ll always be the cheapest” strategy works for Amazon for web services and Walmart for consumer products because there are other things in their vast arsenals that they can monetize. LevelUp, at least now, is mainly banking on the fact that merchants will go for the upsell and pay for a turnkey mobile solution that helps them acquire and retain customers.

It’s no secret that everyone now is tinkering with new business models for payments, especially those that leverage mobile devices and data analytics to basically replicate what Seth and LevelUp pioneered a couple of years ago. LevelUp is still a young pup though – two years old with 5,000 merchants and 1 million consumers. LevelUp may need to grow a bit more to gain enough real scale and perceived heft in the marketplace to force others to reprice (or repackage) their services in order to compete effectively in the merchant category that Seth and LevelUp are targeting – QSR’s. But, since most third party players have chosen the QSR space to launch their digital wallets, they will have to work harder to convince merchants that they have a strong value proposition.

What’s novel though about the LevelUp proposition is how it could sort of get merchants, collectively, in a geography to rally behind LevelUp for the common good – getting processing costs down forever. LevelUp’s strategy is all about getting dense concentration in a geography. Maybe this “all ye merchants in Boston/Philadelphia/Minneapolis, etc. bring me your volume and I’ll bring you zero processing fees” becomes the digital age’s version of the Boston Fee Party without the nasty boycotting. It’s clearly one way to get the door open pretty wide to a bigger discussion about what mobile and targeted campaigns wrapped around a slick mobile payments experience can do to deliver just the sort of thing that small merchants want: more customers and incremental spend.