Nearly one-third of the U.S. population is either underbanked or unbanked, according to the FDIC. And over 20 percent of employees in the U.S. do not have bank accounts, often leaving their employers without an effective way to pay them. For SMBs in particular, payroll affects every aspect of operations, but the traditional distribution approach involving costly paper checks or even direct deposit is in need of a change, according to First Data. PYMNTS got the scoop on how First Data’s Money Network® Service offers a painless payroll process for businesses across the nation.

Nearly one third of the US population, or 106 million people, are either underbanked or unbanked, according to the FDIC. And out of 146.7 million people in the U.S. who are working, 20 percent do not have a bank account, often leaving their employers without an effective way to pay them.

For SMBs in particular, payroll affects every aspect of business operations, including employee moral and financial stability. Without a payroll process that is cost effective, and easy to implement, SMBs may find themselves taking on a larger burden than necessary.

Traditional paper payroll check distribution approaches involve high costs associated with processing and distribution– an average of $2 per employee pay period, says First Data. Compliance with complex state and federal regulations as well as check fraud (are among some payroll check distribution issues that businesses and employees currently face.

There has been little change over the years to this traditional approach, according to First Data, Some companies have been slow to change their more traditional approach to payroll. Companies are still looking to meet compliance regulations with company-issued paper checks and offering direct deposit to employees with bank accounts but then where does that leave the unbanked?

According to Mark Putman, SVP of Prepaid Solutions at First Data, the company’s Money Network Electronic Payroll Distribution solutions “are really helping the underbanked become financially mainstream, giving them a product that does not overdraft and offers extremely low fees.”

“Our current average cardholders pay less than $5 per card per month, across millions of cardholders, which is a shear benefit to the consumer,” said Putman.

To find out how a well-designed payroll card program can benefit both SMBs and their employees, download First Data’s free guide below.

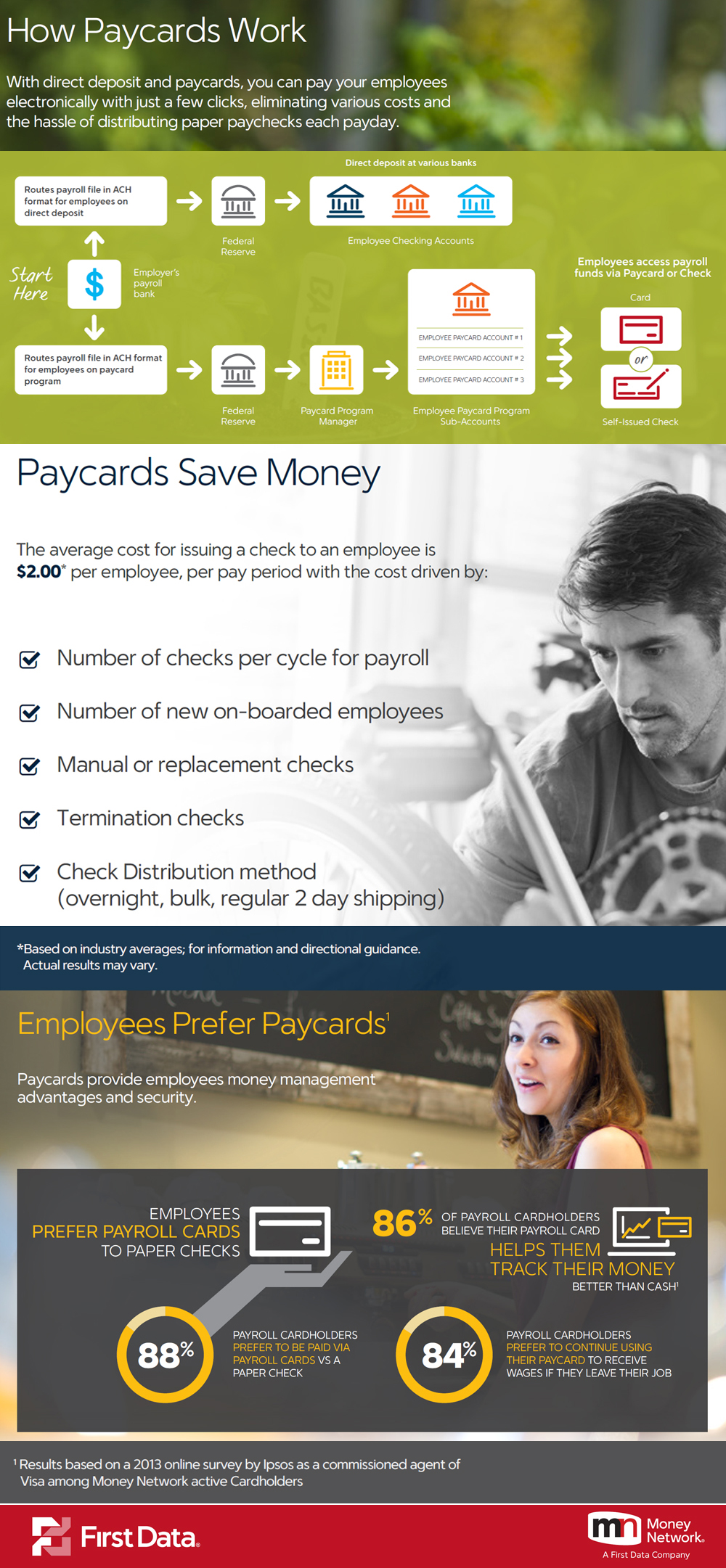

How Paycards Work Infographic:

To find out how a well-designed payroll card program can benefit both SMBs and their employees, download First Data’s free guide below.