Digitizing legacy onboarding processes calls for banks to enable online account opening while simultaneously adopting identity verification solutions to protect new customers’ information. FICO’s Consumer Digital Banking study revealed that just 16 percent of U.S. and Canadian banks offer the ID validation tools required to securely open accounts online. The study also showed that while 75 percent of consumers would be willing to open a bank account online, 23 percent would abandon the onboarding process if ID verification proved to be too inconvenient or complex. The other challenge financial entities face is that customers have to be willing to help protect themselves for banks’ identity protection strategies to be most effective. Only 18 percent of FICO respondents said they used password management software, and another 18 percent said they simply write their passwords down, leaving much room for improved security.

This month’s Deep Dive examines the current state of the customer banking experience and how banks are leveraging innovative identity verification tools to modernize their onboarding processes and prevent users from abandoning account setup.

How Biometrics Help Narrow The ID Verification Divide

Making sure that customers’ identities are genuine when they sign up for new accounts is the main factor driving most banks to revamp their digital ID verification strategies, with 51 percent of bank executives in one recent study stating as much. There are several challenges that financial institutions (FIs) must first address before putting robust tools into place, however. Banks have strict compliance standards they must meet for onboarding and managing customer information, for example. Meeting those requirements was the top concern of 53 percent of banking executives in one recent study when innovating their ID verification strategies.

FIs thus need identity solutions that allow them to comply with digital privacy guidelines and updated financial regulations without adding friction to the onboarding experience. This means moving away from branch visits and paper documents to tools that can identify consumers based on data they have readily available, such as their fingerprints or voices. Biometrics could add the necessary security and speed to ID verification to keep up with both regulatory requirements and consumers’ demands.

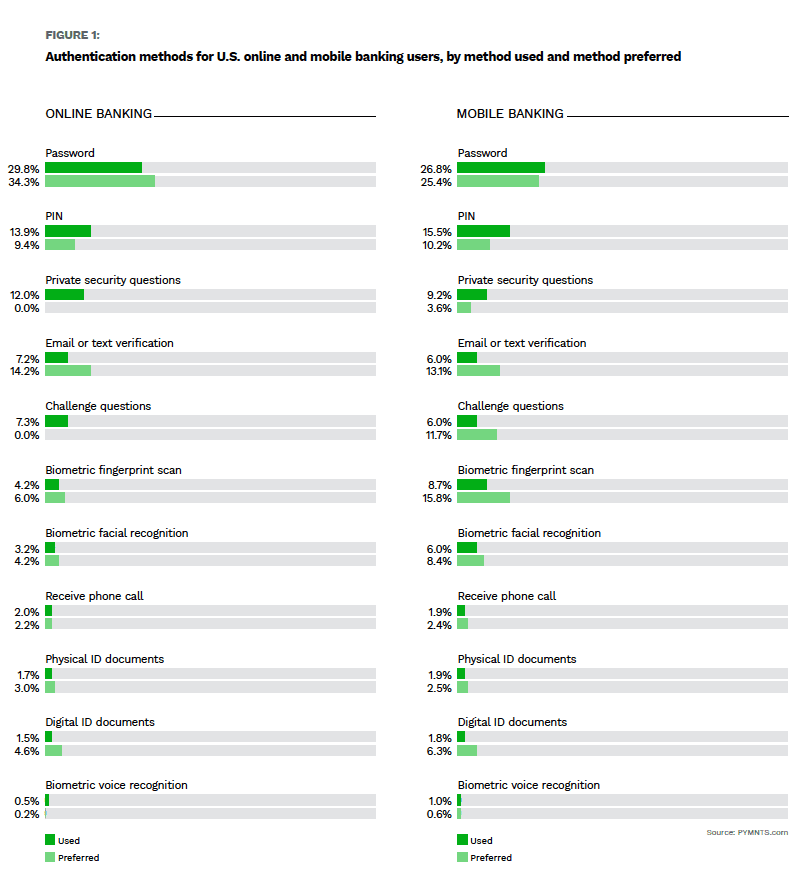

The good news is that consumers globally are becoming more comfortable with biometrics as their method of choice when verifying their identities online. One recent study of banking users in the U.K. indicated that 71 percent would provide biometric data to their chosen FIs. The most popular biometric method appears to be fingerprint scans, with 48 percent of U.K. consumers saying they would be comfortable providing their fingerprints to banks to access their accounts or verify their identities.

This comes as more smartphone manufacturers graft fingerprint scanning capabilities into their devices, making biometric tools more accessible to the growing number of consumers who are banking via mobile. American consumers are less enthusiastic about biometrics than their U.K. counterparts, but the technology’s popularity is slowly increasing among mobile users. Nearly 16 percent of U.S. mobile banking users in a recent PYMNTS study stated they preferred to authenticate themselves using fingerprint scans, though only about 9 percent said they actually used this method to access their accounts.

This gap between preference and actual usage may exist for several reasons, including the possibility that available biometric options do not offer the speed or security that users would like. Closing this gap could be critical for FIs looking to engage and onboard consumers digitally in the coming years. Many FIs may still face barriers in doing so, however, because consumers are asking not just for biometrics but instead for a whole fleet of digital options from their banks when signing up for new accounts.

Optimizing ID Verification For A Mobile-First World

Focusing solely on biometrics could be the wrong move for FIs, as consumers appear to be requesting a variety of emerging ID verification solutions from potential financial partners. One of the most important factors driving consumers’ choice of verification type and choice of bank is whether the method is optimized to the banking channel they are using to onboard. Consumers are searching, in other words, for solutions that are not only digital but also mobile-first.

Tailoring ID verification solutions to run seamlessly on mobile could give FIs a key advantage over their competitors. Consumers are even willing to provide the typical documents FIs need when onboarding as long as they can do so via their phones’ cameras. One recent study found that two out of three U.S. consumers would be willing to take photos of their ID documents as long as doing so would make the onboarding and verification processes safer, faster and more secure.

Staying on top of this rising preference for mobile-first banking requires that FIs approach their ID verification and onboarding strategies so that they work together in a cohesive way. Failing to do so will see banks fall behind on the digital banking curve.

The pandemic has driven more consumers to seek the safety and convenience of online banking, yet new data has revealed that banks in Canada and the U.S. may not be doing enough to protect against identity theft or money laundering for the increased volumes of digital banking users. FICO recently reported that a majority of U.S. and Canadian banks still require customers to prove their identities by visiting branches or submitting documents when opening accounts online. The requirements were similar for 25 percent of mortgages and 15 percent of credit cards opened online as well.

The pandemic has driven more consumers to seek the safety and convenience of online banking, yet new data has revealed that banks in Canada and the U.S. may not be doing enough to protect against identity theft or money laundering for the increased volumes of digital banking users. FICO recently reported that a majority of U.S. and Canadian banks still require customers to prove their identities by visiting branches or submitting documents when opening accounts online. The requirements were similar for 25 percent of mortgages and 15 percent of credit cards opened online as well.