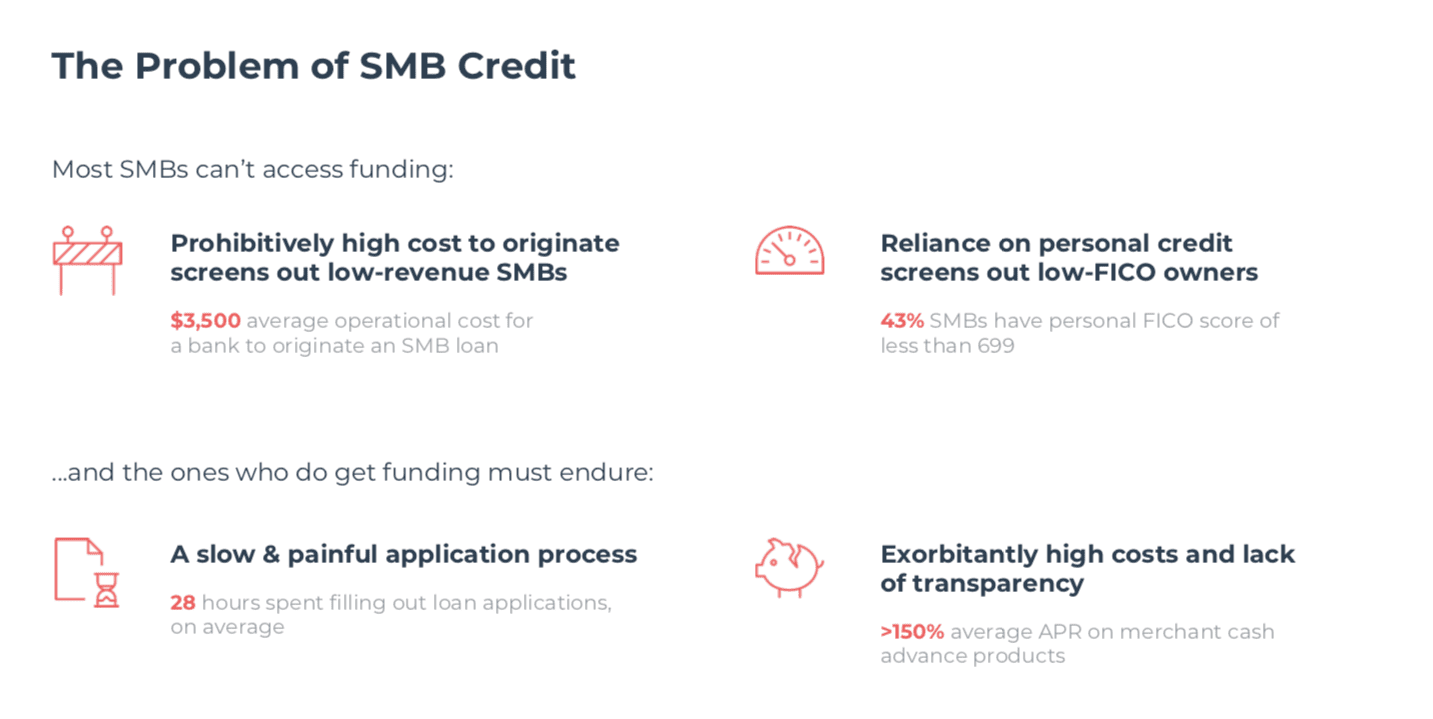

The $24 trillion global B2B commerce opportunity, as PYMNTS readers know, is continually — and has been historically — plagued by the paper chase. The flow of commerce and capital gets bogged down in phone calls, applications, emails and inefficient risk profiling based on traditional credit models.

In terms of payments technology and alternative lending, B2C and B2B may be respectively seen as digital versions of the hare and tortoise. Consumers are used to having any number of payment options on offer when they’re ready to push a buy button onscreen, at any time of day. The gap, though, is narrowing when it comes to linking buyers and sellers, and making sure the deals done between them are as frictionless as possible.

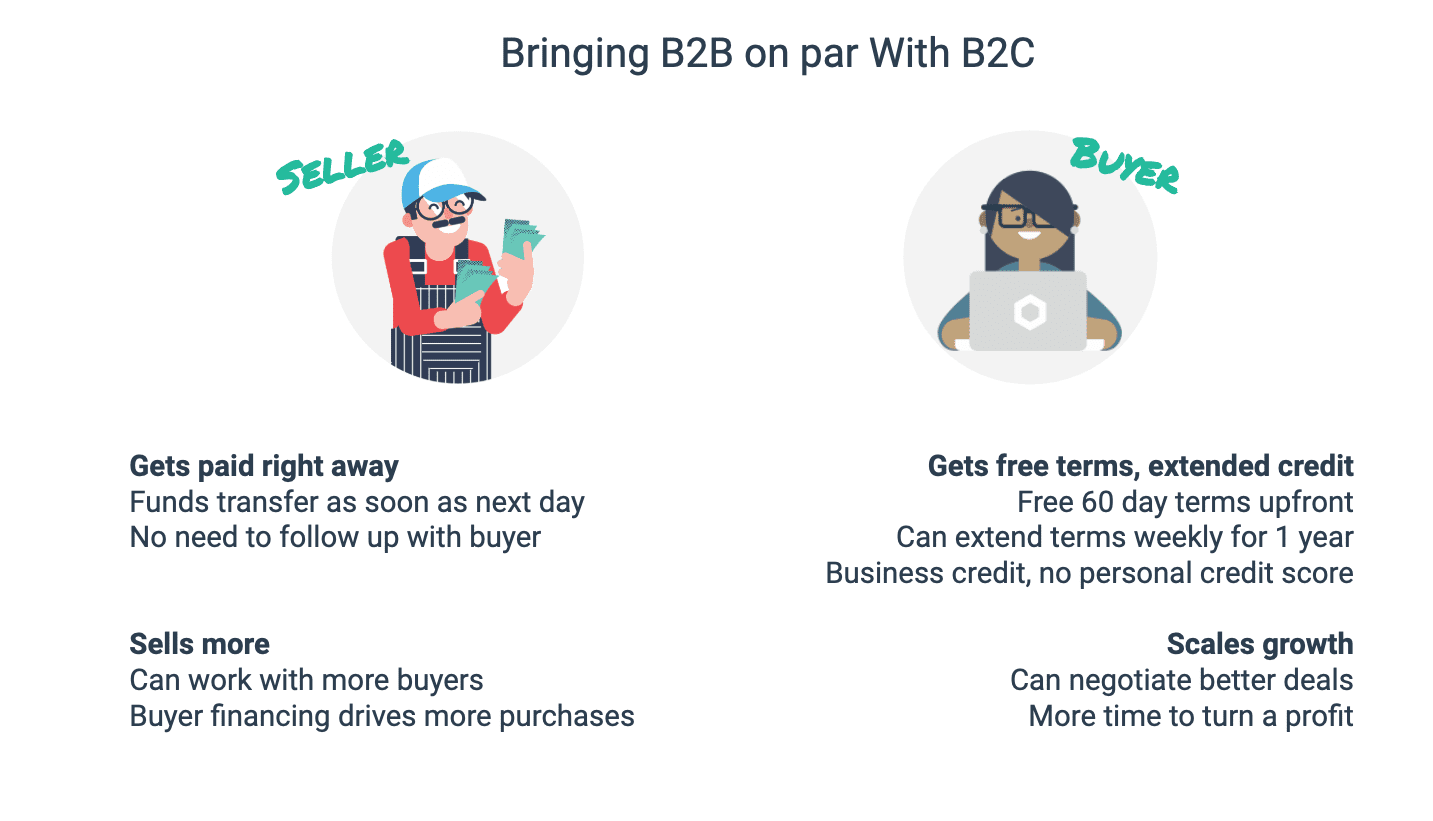

B2B-focused FinTech firms have been eyeing what’s available from consumer-focused companies. Credit offered at the point of sale (POS) is a concept that, done successfully, can help smaller firms move away from inefficient processes rooted in paper, and can mean the difference between taking on a project and growing … or not.

Picture an HVAC maintenance firm that needs to buy equipment before installing it into a building, or the retailer that wants to buy a truckload of sweaters, anticipating the coming season’s “must have” offering. Credit can bridge the gap as companies run their day-to-day operations, and help them capture top- and bottom-line growth.

To that end, Fundbox said in a release on Friday (Jan. 25) morning that it has expanded access to its business credit solution Fundbox Pay. Now, the company is offering capital so as to finance B2B payments at checkout, or — as Fundbox Chief Business Officer Sebastian Rymarz termed in an interview with Karen Webster — the “point of transaction … and the point of need.”

Credit decisions can be made within three minutes, he said.

The company said the focus on smaller firms and eCommerce comes as its own internal data has shown that as much as 24 percent of monthly revenues by small- to mid-sized businesses (SMBs) are tied up in accounts receivable or trade credit, which stymies cash flow. Fundbox noted that the opportunity within eCommerce is sizable. Forrester Research found that, in the U.S. alone, B2B eCommerce transactions will reach $1.2 trillion within two years, and will account for 13 percent of all U.S.-focused B2B sales.

Extending Fundbox Pay into checkout mirrors the B2C commerce experience that offers access to capital, which can cement the deal for sellers and offer terms for buyers tailored to their individual risk profiles. Rymarz explained that the concept behind Fundbox Pay (and now its extended availability) recognizes that — for retailers, restaurants or consumers — credit card networks exist to serve as a bridge to commerce.

Businesses get paid today, and credit allows for buyers to have a grace period to pay back what they’ve borrowed.

A Major Gap

That consumer-focused network has been around for decades, said the executive, who added that “it’s amazing to us that nothing like that has happened in the B2B space.”

In B2B, the SMBs that wait to get paid — and see receivables stretch out before getting turned into cash — are, in effect, acting as bankers to their trade counterparts. For those firms seeking access to credit, lenders will often start with the SMB principal’s FICO score or tax returns from the past few years, which can be an inefficient barometer of credit risk.

“This is a major gap in a market that is three times the size of B2C,” he told Webster. “These are blunt tools, and they are expensive because someone has to manually gather that information, and it takes time” — and some of the forms submitted can be erroneous ones. As a result, many small businesses find their credit needs unmet, namely in the form of being able to finance their payments.

Trends Are Converging

Trends Are Converging

The trends are converging to make this credit offered at the B2B POS possible, he said. Among them, “the tectonic shift in the data landscape” can let sellers provide credit and promotional financing to their small business customers.

Rymarz stated that far-flung data used in credit-decisioning comes to Fundbox from accounting systems, invoicing platforms and bank data. “All of this valuable financial information that can tell you about the creditworthiness of a business is available online in the cloud — and, most times, it is available for free,” he said, pulled in through application program interfaces (APIs) and fully automated — integrating all that information.

“Credit is just a natural extension of that [cloud-based workflow] platform,” he continued, adding that Fundbox Pay’s artificial intelligence (AI)-driven model, built over a period of years, can offer credit at a point of need, such as payroll or when an invoice is due.

Fundbox Pay, extended into checkout, he said, offers a “turnkey way … to offer credit.” Firms that offer cloud-based workflow solutions “can be a powerful place for presenting credit at the point of need, and to ‘contextualize’ that credit.” Context comes from machine learning, which examines thousands of data points and entities, spanning transactions and even IP addresses (where, for example, fraud tied to a specific IP address can set up a “red flag” in credit-decisioning that would be missed by conventional means).

The Process

The Process

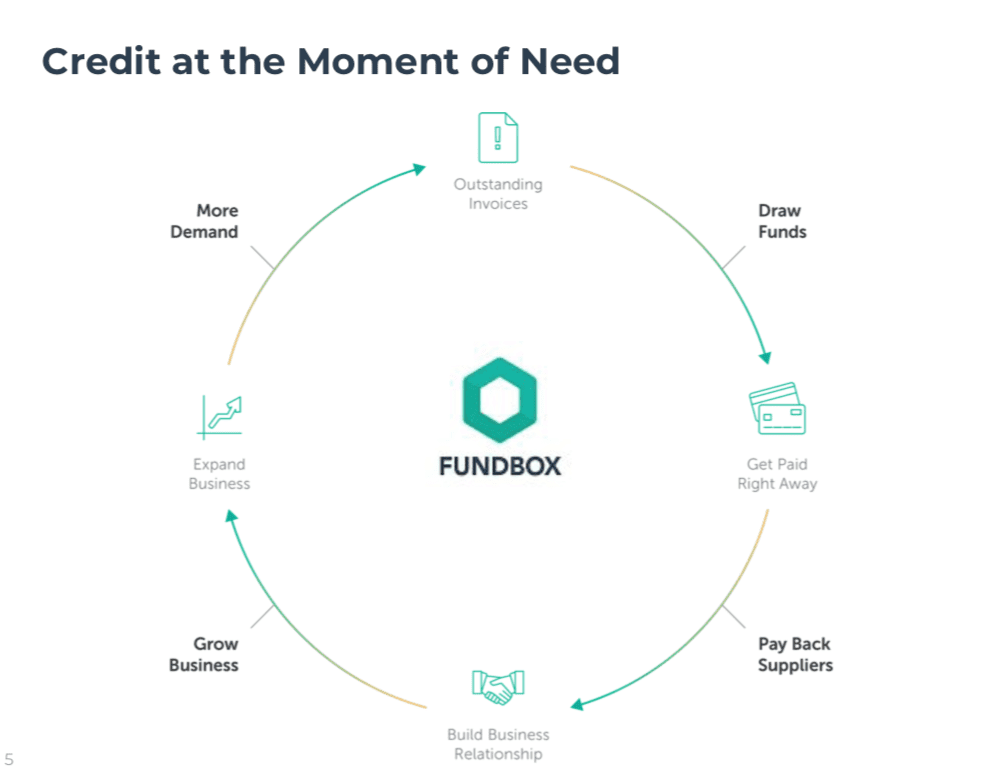

The sellers are paid through Fundbox, and financing is offered to the buyers as a line of credit or on a transaction-by-transaction basis via terms (i.e., to be repaid in 30, 60 or 90 days).

“From a seller’s perspective,” Rymarz explained, Fundbox Pay, through its newest iteration, “is an opportunity for commerce enablement. As a seller, you can increase your average order value by offering terms to your customers. If you can offer net 30, net 60 or net 90 terms to your [customers, you] are going to be able to sell more and get paid today. We almost consider that this is a new channel and not necessarily a new product.”

In terms of mechanics, a $40,000 credit line can be offered to fund a purchase (say, through QuickBooks) as a buyer seeks financing, and can be drawn down and repaid. The SMBs, as Rymarz put it, “[increase] their purchasing power, which allows them to take some risks and grow their business[es].” He stated, too, that businesses can prepay their loans without penalty, a form of incentivized good behavior.

When asked about how the firm monitors risk, he said risk assessment occurs at the onboarding stage. Then, after three months of using Fundbox Pay, a customer is reassessed as the firm uses “a whole new set of models and policies that take over, and we will rescore that customer every month thereafter,” he said, as the company is connected to their back office, accounting system or payment solution.

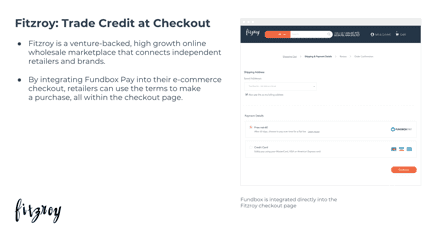

One company embracing Fundbox Pay at checkout is Fitzroy Toys, an online wholesale B2B marketplace focused on smaller businesses that connects toymakers with merchants. In an interview with PYMNTS, Fitzroy Toys stated that Fundbox Pay provides both sides of the retail equation a lifeline to sustain current operations, and a growth line that allows SMBs to gain economies of scale that might not be available without access to credit.

One company embracing Fundbox Pay at checkout is Fitzroy Toys, an online wholesale B2B marketplace focused on smaller businesses that connects toymakers with merchants. In an interview with PYMNTS, Fitzroy Toys stated that Fundbox Pay provides both sides of the retail equation a lifeline to sustain current operations, and a growth line that allows SMBs to gain economies of scale that might not be available without access to credit.

The variety and size of inventory orders for toy retailers mean, too, that Fitzroy Toys is able to offer a flexible range of terms on that credit extended to buyers and sellers. That’s especially important when the average store Fitzroy works with has more than 500 different vendors. With Fundbox Pay at checkout, those retailers coming to the online marketplace are able to purchase inventory on offer across all the vendors — without the back and forth of PDFs or faxes to set up payment terms (thus, of course, cutting down on the paper chase).

“We actually increase lines to customers much more than we decrease,” Rymarz told Webster, adding that “we are looking for intuitive context to empower small businesses and put credit at their point of need.”