Such is the situation in financial services, where the capabilities that have been unlocked by digitization have rather radically changed consumers and preferences — although perhaps in ways that don’t stand out as obvious.

Yet.

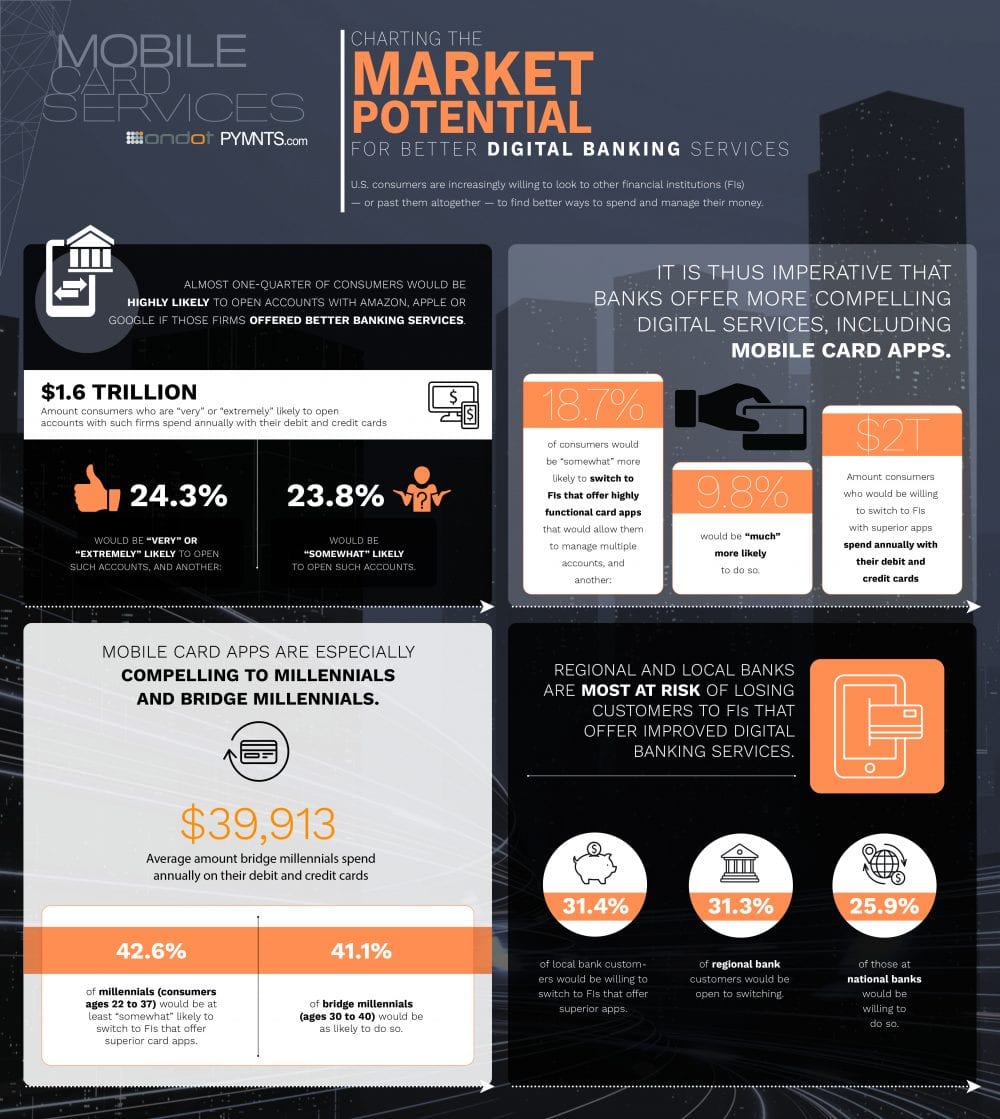

But desire for change among consumers, by the numbers, is there. According to Building A Better App: Banks And The Innovation Imperative, a report co-produced by PYMNTS and Ondot, almost a quarter, or 24.3 percent, of consumers reported they would be highly likely to seek banking services with Amazon, Apple or Google — while another 23.5 percent indicated they would be at least somewhat likely. Meanwhile, 28.5 percent of consumers noted they would switch financial institutions (FIs) for a better financial app, a number that jumps up to 41 percent among bridge millennials.

The pressure is certainly there, Vaduvur Bharghavan (VB), president and CEO of Ondot Systems told Karen Webster — particularly for smaller and local banks, where roughly a third of consumers said they were ready to jump ship to Big Tech. That’s because things that seemed like add-ons when it came to digital banking even five years ago — card controls, instant virtual card issuance, self-service security, mobile deposit capture — are now table stakes.

“In our client base alone, we have helped 4,500-plus institutions launch a full suite of capabilities including location-based controls, transaction types, merchant type spend limits, on and off functionality for cards,” VB noted. “When you present those features as a reality consumers can viscerally touch and feel and see people around them using — demand is going to spike more than it already has because once people know what’s possible and they experience that, it’s automatically a viral effect.”

“In our client base alone, we have helped 4,500-plus institutions launch a full suite of capabilities including location-based controls, transaction types, merchant type spend limits, on and off functionality for cards,” VB noted. “When you present those features as a reality consumers can viscerally touch and feel and see people around them using — demand is going to spike more than it already has because once people know what’s possible and they experience that, it’s automatically a viral effect.”

It’s an effect that leaves customers unwilling to settle for less than they want when there are other places to get it, he said. That doesn’t mean that they will necessarily leave their local providers, small bank or credit union (CU) behind, he said, so much as those providers will lose the opportunity to have that primary financial relationship with them — in favor of the tech firm or big bank that can give them that all-in-one digital experience.

That, he said, is the bad news. The good news, particularly for smaller FIs, is their ability to be nimbler, build more partnerships and roll out to market with advance capability more quickly. But, he noted, the challenge in some cases is in convincing small FIs that this is a change they need to make — not simply an expansion they should slowly consider.

Converting The Doubters

About half the FIs Ondot deals with, VB said, “get it” the minute they walk in the door. They understand why they want to turn their app into a one-stop shop digital financial management hub and are absolutely concerned that Google, Amazon Apple and the like are about to start encroaching on their consumer turf. Their questions aren’t so much about why they should be doing this, and much more about how to get started.

The other half, he said, aren’t uninterested; it’s more that they don’t think it concerns them. Cards — debit or credit — they say, are not really their core business. What is incumbent on Ondot and similar firms, VB said, is making the case very clearly that this is meaningful for everyone. Consumer card spending, according to the Innovation Imperative report, is a $2 trillion a year business the doubters are essentially opting out of — not to mention the very best way to establish that daily connection with their customer base.

“The numbers are telling me that mainstream America and affluent America are moving toward a digital-first solution,” VB said.

And the FIs that will move along with them, he said, will be the ones that survive and thrive.

“We hear a lot, ‘Look, I make my living through loans, and I make my living through deposits. Cards are really auxiliary to my business,’ but to some extent that’s missing the point,” he said. “As digital becomes primary, the primacy of card in the consumer interactions for issuers becomes way more important, and it goes beyond just the direct benefits.”

Finding The Right Advantages

Consumers still trust their banks more than the average Big Tech firm, VB noted, but banks can’t quite rely on that to preserve their own primary consumer financial relationship with customers. The reality is that to some extent consumers are willing to trade off trust for convenience. Consumers have a very exciting, fulfilling relationship with these firms and, most importantly, they are starting to see them as the go-to hubs for digital services and friction-free processes.

That, he noted, is not an insurmountable obstacle — even for small banks. The technology exists to offer consumers the services they very clearly want. Smaller FIs are unburdened by layers of legacy infrastructure that needs to be rebuilt, so with the right tech partnerships, they can create the service hubs consumers want.

Smaller FIs also have something Big Tech doesn’t have: trust. VB noted trust is in fact a great starting point when FIs of all sizes are looking to build stickier, more involved consumer relationships — it’s just not enough to also be an ending point.

“Because we really think at the end of the day it is easier to drive excitement in a trusted relationship than it will be for tech firms to do it the other way around and drive trust in a fun relationship,” he said. “So, I think banks if they get busy fast enough still have the ability to own that financial relationship in the future.