Instant payments are having a moment.

Released last week, Zelle’s Q3 results show that its year-over-year payment values rose by 58 percent, while transaction volume increased by 73 percent. During the quarter, $49 billion was sent through the Zelle Network on 196 million transactions.

In the 2019 Disbursement Satisfaction Report, PYMNTS surveyed more than 5,000 U.S. consumers about whether they have received disbursements, the types of institutions from which they received them and how they would like to receive them if they could choose.

Adoption Soars

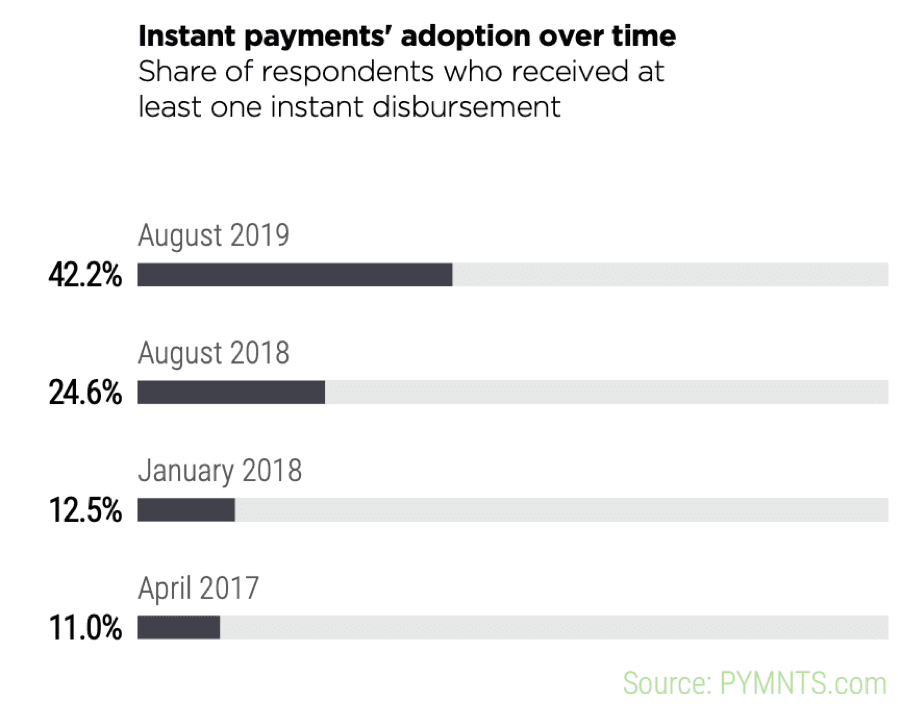

Consumers’ instant payments adoption has increased nearly fourfold over the past three years, with 42 percent reporting they received at least one such payment this year compared to the 11 percent who said the same in 2017.

This adoption is being driven by consumers’ near-universal understanding of instant payments. Eighty-two percent of consumers now know what an instant payment is, up from 60 percent just one year ago. That knowledge comes from exposure, as adult U.S. consumers receive an average of 18 disbursements per year for a total of $4.6 trillion in annual disbursements.

Industry Leaders and Laggards

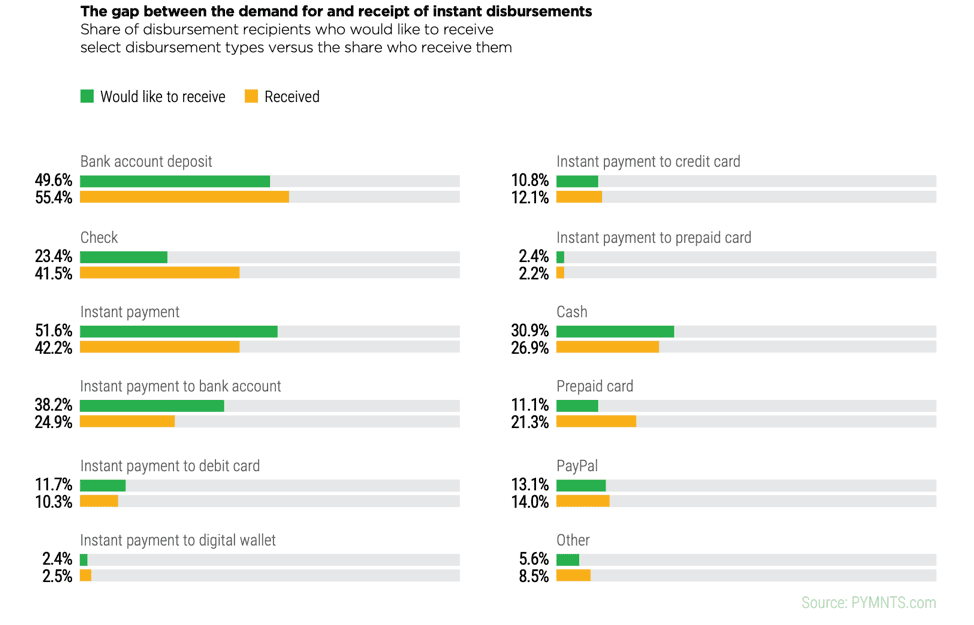

However, there is still a gap between consumer demand for instant payments and payers’ readiness to offer them; 42.2 percent of disbursement recipients were paid via instant payments in 2019, but 51.6 percent say they would prefer to be paid this way.

Specifically, 38.2 percent of consumers want instant payments to a bank account, 11.7 percent want instant payments to a debit card and 10.8 percent want instant payments to a credit card. Only 23.4 percent want to be paid by check.

Both Mastercard and Visa report that disbursements via debit cards to consumer and SMB bank accounts are on the rise. Both card networks are pushing money over their debit rails and instantly into the bank accounts of consumers and SMBs using their debit card aliases.

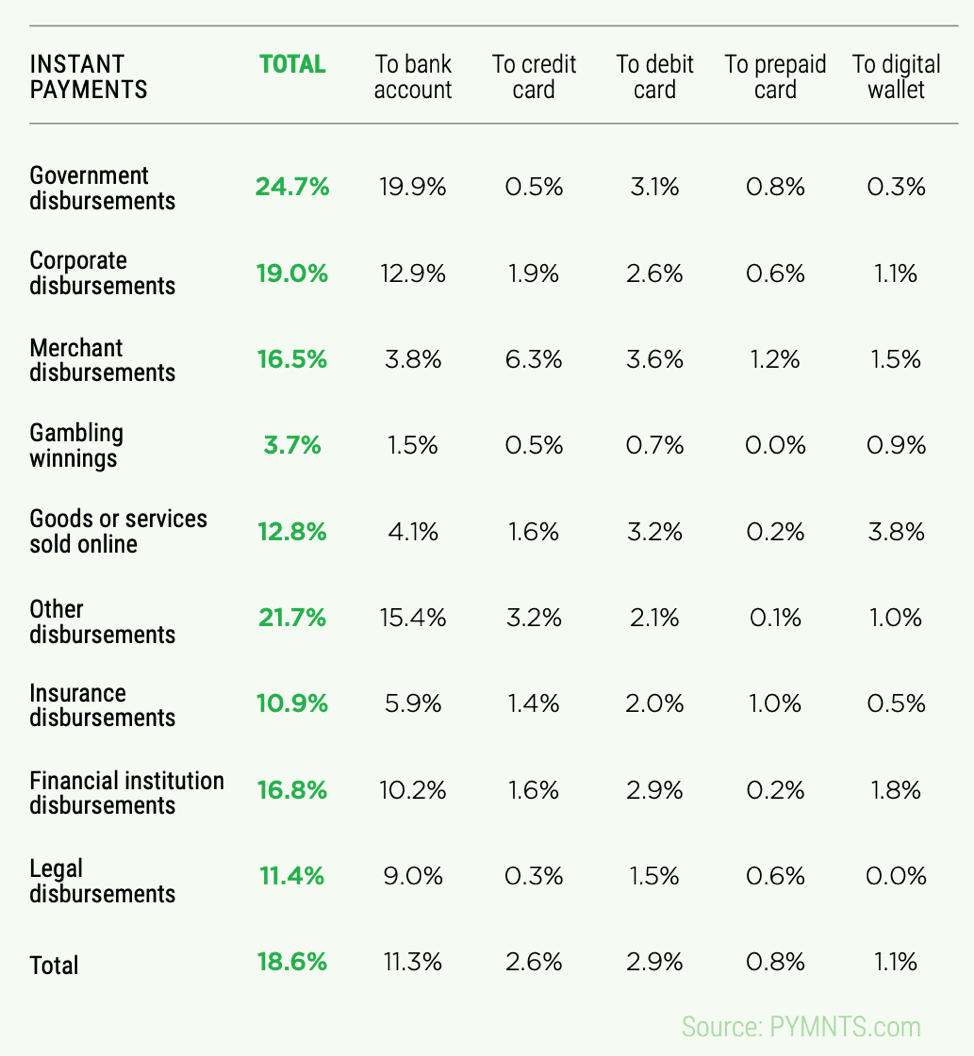

Sluggishness varies by industry, though. Just 11.4 percent of legal disbursements were paid via instant payments in 2019, even though consumers indicated they want to receive such disbursements through instant rails in 25.8 percent of cases.

The government was ahead of the pack, with nearly one-quarter (24.7 percent) offering instant disbursements, while roughly one in five (19 percent) of corporate disbursements are instant.

Government disbursements cover tax refunds, among other payments. Traditionally, even early tax filers must wait months to gain access to their tax refunds. In another demonstration of the move from paper-based processes and further into digital for the tax preparation industry, services like H&R Block are getting creative by offering qualified customers instant refund advance loans.

Even the growing legal gambling sector is getting into the instant disbursements act. As PYMNTS coverage has confirmed, a big area of growth for legal betting in the U.S. in the coming years will almost certainly be the prepaid card aspect.

The insurance industry is especially out of touch with consumer demand. Only 10.9 percent of insurance disbursements were made via instant payment rails, while consumers indicated they would have liked to receive them via instant payments in 30.1 percent of instances.

However, this might be slowly changing. Visa has recently made multiple new partnerships to digitize and accelerate insurance claims payouts.

Recommendations

In a recent interview with PYMNTS, Anupam Sinha, global head of domestic payments and receivables at Citi, explained that this industry shift toward speed must not only respond to changing customer demands, but must also anticipate future needs that even the users – treasurers included – may not yet know they have.

With the U.S. investment in real-time payments – one of the first major payments infrastructure investments the country has made in decades – corporates are increasingly acknowledging the potential in instant payment rails. Though real-time payment services are not entirely new, it is only in the last several years that significant infrastructure investments have been made.

For the payment itself, Sinha said, that means cutting out the friction, promoting standardization and, increasingly, making the payment process so integrated and frictionless that a user hardly even notices it’s happening.

In a recent interview with PYMNTS, Ingo Money CEO Drew Edwards said the direction of the market is clear. As more consumers experience instant payments, the demand will only increase.