The conventional wisdom about consumers is the average person doesn’t really care about how payments happen.

Security? Check.

Rewards? Check.

Acceptance? Check.

Type of payment rails on which the transaction travels? Not so much.

But consumers should care, according to instant payment service platform Eco’s CEO, Andy Bromberg. He told Karen Webster that consumers can appreciate payments infrastructure when they understand that the complex backend magic that enables how they can pay also affects how much they are paying.

“Consumers don’t really care what rails payments are going on or the underlying technology and interactions between issuers and acquirers,” Bromberg said. “But they do care about the benefits to them. When they are being offered 5 percent cash back and rewards for saving and spending, maybe they didn’t care before, but all of a sudden, they say, ‘Well great, I care now.’ And that’s powerful.”

It is the power that Eco is attempting to tap into as its digital wallet goes into wide public launch with the rather ambitious goal of taking on checking accounts and debit cards with a single financial product that aims to offer a non-bank alternative better able to robustly meet consumer needs. The firm ended last week announcing an investment round of over $26 million led by a16z Crypto, with participation from Founders Fund, Activant Capital, Coinbase Ventures, Slow Ventures, and more than 100 others.

Bromberg said those funds will go toward building a financial services product designed to do everything a bank, checking account, or credit card can — but do it better and in a way actually designed to serve the consumer.

“The idea really came from a reduction process rather than a generation process and saying, what could we cut from this system?” he said. “And you start to cut and pare down to only what is needed. Then you get to these ideas like a compounding balance, putting everything in one place, simplifying your financial life, and then how to start implementing that.”

Staring With Simplicity

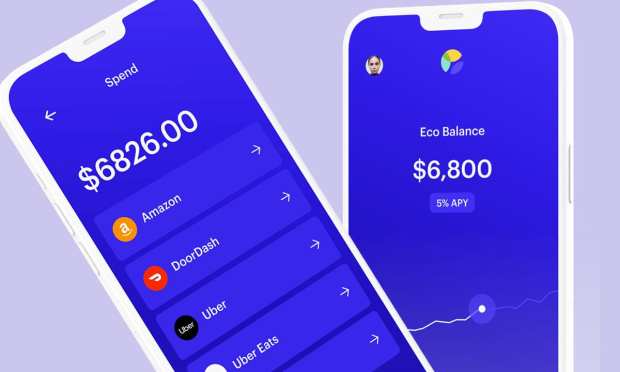

The process of using Eco for consumers is straightforward. The consumer either deposits or sets up direct deposit into their Eco mobile wallet account. The consumer incentive to place funds into that account is the wallet’s unusually high annual percentage yield (APY), which starts at 2 percent and can go all the way up to 5 percent if the customer refers other users to the app.

The Eco wallet is also designed to allow for consumer spending, for which it rides the gift card rails to make it basically spendable at any merchant. When a consumer wants to spend, they can either load the precise amount that they need onto the gift card of their choice or set the cards to auto-refill as necessary.

Bromberg said the second option is more convenient, but only money actually deposited within an Eco account is earning interest, so the consumer can prioritize according to their own needs.

If the model sounds familiar, it probably should, Bromberg said, as it is very similar to the Starbucks model, albeit with the additional bonus of APY on one’s balance.

Moreover, he said, merchants are willing to subsidize the benefits offering on the platform because it allows them to exploit the underrated option of the gift card rail to greater effect and offer a consumer powerful direct transaction experience that just isn’t possible on the standard payment rails when one is interacting with eight different fee takers.

“Merchants, when they sell gift cards wholesale, they’re willing to sell them at a discount because you’re cutting out these intermediaries,” Bromberg said. “And it makes everyone happy. And we just think the more we can get towards direct payments, the better off we’ll be as a society.”

The Road Ahead

The dream of direct payments that cut out interchange fees, Webster said, isn’t a new concept on the payments stage. But getting consumers to make a real change has always been the sticking point that slows down the big pivots.

And Eco, Bromberg said, still has a lot to do in terms of beefing up its offering to be a bigger competitor to the banks out there holding tight to that primary financial relationship with consumers. That means adding bill pay products, mortgage and car payment products, crypto-tools and a host of other upgrades designed to make Eco a truly all-in-one shop for a consumer’s financial management needs.

But, he said, Eco remains optimistic in its competitive chances going forward simply because of the enthusiasm consumers have shown thus far for linking their payroll to directly deposit into Eco accounts.

“We believe pretty firmly that we’re able to take a real shot at people’s primary accounts, and we see our users connect their payroll to these accounts,” he said. “We’ve had a lot of success with getting people to connect their payroll. Right now, it is usually a portion of it because we don’t support bill pay yet. So, they obviously still route their rent or mortgage funds to their bank account.”

But when the company surveyed its users recently, some 87 percent said they would like to participate in the beta test of Eco’s rent and mortgage payment product, a move that would require fully syncing up their payroll, Bromberg said.

Consumers increasingly care about where they can manage their financial services more easily, efficiently and in ways liable to actually benefit them, he said. Eco doesn’t need to be a bank to offer an upgraded version of the services banks do; it may actually do it better because it isn’t one.