Cross-border payments represent a big opportunity for firms worldwide — more than $120 trillion in payments volume flows each year between business trading partners globally, and $10 trillion of that volume is cross-border trade. But along with that $10 trillion opportunity comes a series of challenges. Paper-based workflows, delays in receiving payments, matching payments to remittance data, fraud and a lack of faster payments alternatives for payors and receivers are just a shortlist of the host of friction points players hoping to navigate the global landscape are facing.

It is a situation that pushed the G-20 last year to ask the Financial Stability Board (FSB) to coordinate the development of a road map on how the global community could enhance cross-border payments, Federal Reserve Chair Jerome Powell noted Thursday (March 18) at a Payments and Market Infrastructures Conference in Basel, Switzerland. As it exists today, the system is safe and dependable but suffers from friction and out-of-date technology that make cross-border transactions both more expensive and complex than they have to be. These shortfalls, he noted, become particularly noticeable in regards to compliance with AML and countering-terrorist-financing requirements over complex and managing payments across time zones.

“As with many aspects of life these days, the COVID-19 pandemic has shined a light on the less efficient areas of our current payment system and accelerated the desire for improvement and digitalization. Even before the pandemic, advancements in the private sector served as a catalyst to get the attention of consumers and to prompt more engagement by the public sector,” Powell said of the growing need for simplification and modernization in the world of CX payments.

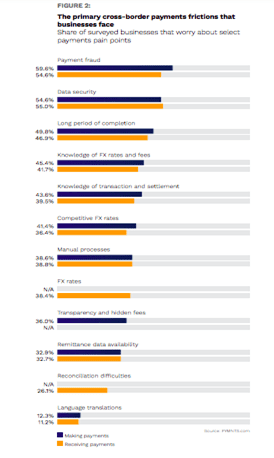

Needs that, according to the PYMNTS recent study with Visa, Innovating Cross-Border Payments: What US and UK Businesses Need to Know, is felt increasing sharply amongst payers and payees worldwide. Leading among those frictions is fear of fraud and theft, with businesses in the U.S. and the U.K. report theft of both funds and payment credentials — though two very different challenges — as key concerns when making and receiving cross-border payments. Smaller businesses most commonly expressed these concerns.

Lack of transparency into the average cross-border payment was also found to exacerbate cross-border frictions for businesses, leading to uncertainty for payment decision-makers who, absent that visibility, are unable to accurately forecast their cash positions.

Lack of transparency into the average cross-border payment was also found to exacerbate cross-border frictions for businesses, leading to uncertainty for payment decision-makers who, absent that visibility, are unable to accurately forecast their cash positions.

The study also revealed that trepidation, on the whole, was generally higher within U.S.businesses than their U.K. counterparts, except for payments theft and fraud. More than half of U.S. and U.K. businesses cite payment theft or fraud as a primary area of concern when it comes to sending and receiving cross-border payments. Fifty-two percent of U.S. businesses and 59 percent of U.K. businesses in the sample report experiencing concerns over payments fraud or theft when receiving payments.

The survey also found that firms are interested in capturing the CX opportunity, provided they can do it safely and they seem to understand that it isn’t an opportunity that can necessarily be captured alone.

Sixty-three percent of all surveyed businesses would be interested in partnering with third-party providers to digitize their cross-border payments processes in the next three years, with the most interested businesses being those with the highest and the lowest annual revenues.

And in his remarks, Powell noted that public entities would have to be part of the equation of getting CX where it needs to be a viable option for more firms.

“The goal of the FSB roadmap is simple — to create an ecosystem for cross-border payments that is faster, cheaper, more transparent and more inclusive. A year into the process, I am encouraged that we are making meaningful progress,” he said. “One of the keys to moving forward will be improving the existing system where we can while also evaluating the potential of and the best uses for emerging technologies.”

Powell called the Federal Reserve’s efforts in pushing faster payments through its FedNow Service, designed to make uninterrupted processing — 24 hours a day, seven days a week, 365 days a year— possible by the year 2023.

Speed, the PYMNTS/Visa survey notes, is important, particularly to medium-sized firms. According to the report, 46 percent of mid-sized businesses prioritize automated payments from invoices to improve their payment receipt speed, while one-third plan to automate their receivables to enable speed of collections and cash application.

And the Fed, Powell pointed out, is willing to lean into new technologies, including experimenting with central bank digital currencies (CBDCs) currently underway by the Board of Governors and in conjunction with MIT at the Federal Reserve Bank of Boston.

The pandemic, he noted, did not create the need for improvement in the FX market, but what it did do is highlight how pressing the need for solutions is — and how much improvement can be built off of them.

“Digitalization of financial services, combined with an improved consumer experience, can help increase financial inclusion, particularly in countries or areas with a large unbanked population,” Powell said.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More