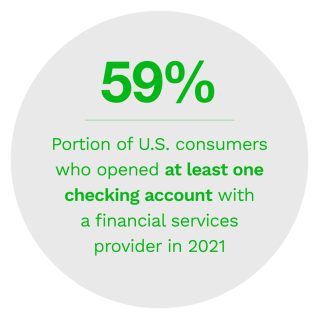

Six in 10 adult consumers in the United States opened at least one new financial account in 2021, meaning a minimum of 152 million such accounts were activated last year. Whether financial institutions know it or not, these accounts compete for consumers’ use and attention.

Providing accounts that allow users to make and receive a wide variety of payments is the key to standing out from the competition, as users require payments flexibility to easily, securely and seamlessly transact in their daily lives. If account issuers cannot grant their account holders a certain level of “money mobility” necessary to transact in their everyday lives, then these issuers risk being pushed to the periphery of the money mobility ecosystem and losing their share of users’ wallets.

The inaugural Money Mobility Playbook, a PYMNTS and Ingo Money collaboration, provides a blueprint for what FinTechs, neobanks and other account issuers must do to deliver on users’ expectations for a maximum amount of money mobility and become central to consumers’ everyday lives.

Key findings from the playbook include:

Key findings from the playbook include:

• Consumers separate their accounts into two categories: primary accounts or periphery accounts. Primary accounts are those used nearly every day, while periphery accounts are used less often. The more money mobility an account provides, the more likely it is to be a primary account.

• Trust drives 59% of consumers’ choice in designating a primary bank. Overall, more consumers choose their banks based on trust than any other factor.

• One-third of consumers would pay a 5% added fee to get paid instantly. Account issuers must be able to receive instant disbursements to provide the instant money-in capabilities consumers want.

These are just a few of the findings that provide insight into how important  money mobility truly is to today’s account holders. The inaugural edition of the Money Mobility Playbook provides additional actionable insights into the steps that account issuers must take to enhance money mobility and earn a larger share of users’ wallets.

money mobility truly is to today’s account holders. The inaugural edition of the Money Mobility Playbook provides additional actionable insights into the steps that account issuers must take to enhance money mobility and earn a larger share of users’ wallets.

To learn more about how money mobility can help FinTechs and neobanks gain a competitive edge, download the playbook.