Despite some positive key performance indicators delivered this week, the U.S. retail and economic recovery is still facing serious headwinds.

The positive news came in the form of U.S. retail sales, which exceeded forecasts in June. Retail spending increased 7.5 percent from May, according to Commerce Department data out Thursday. The increase was driven by more business reopenings as well as expanded unemployment benefits. What was not clear was the effect stimulus funds made on retail spend. But the May and June spikes returned retail sales levels to pre-pandemic numbers.

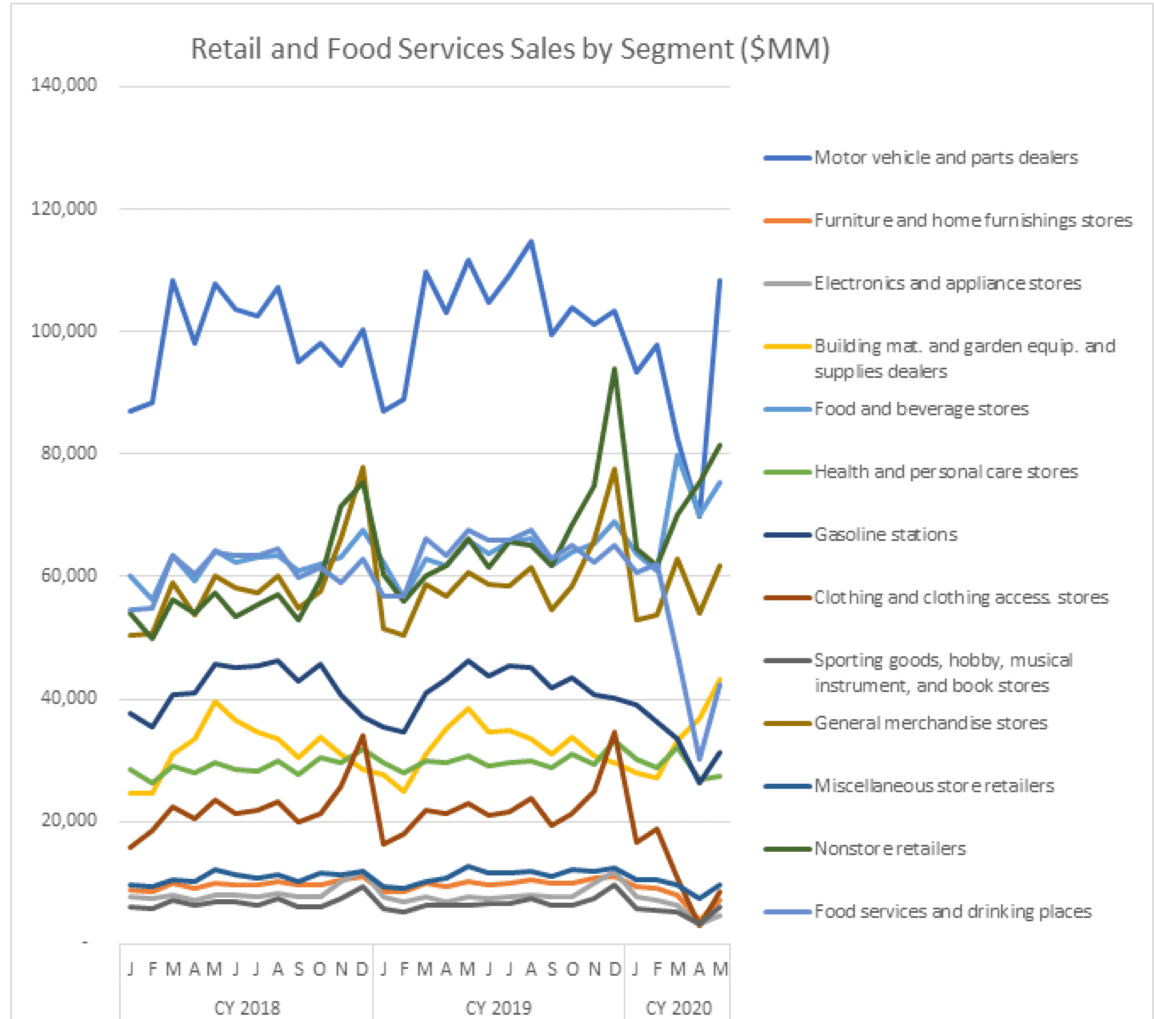

The retail numbers do indeed indicate a recovery. Based on numbers from the Atlanta Federal Reserve through May 31, the graphic below shows healthy increases for several sectors, most notably motor vehicle and parts dealers, food and beverage stores and an uptick in restaurants, which had plunged in previous months. These changes were reinforced by the June data.

But the recovery numbers raise many red flags and cross currents. The first is whether the retail spend numbers can be sustained.

The figures “confirmed the strong snapback in demand as retail sales are now back to their pre-coronavirus levels,” Oxford Economics’ Lydia Boussour and Gregory Daco wrote in a note Thursday, according to Advisor Perspectives. “But while today’s report gives the illusion of a fearless consumer spending lavishly, the reality is more sobering: Consumers are increasingly fearful amid new spikes in COVID-19 cases and a looming fiscal cliff.”

Boussour and Daco confirm the PYMNTS COVID-19 tracker research, which showed customers will return to their previous shopping behaviors when the virus stops spreading and its effects are mitigated.

The health factor is also the key structure in the PYMNTS Digital 3.0 FIT framework that recommends companies take care of consumer safety concerns first before they get to the three pillars of the framework: removing friction from consumer interactions; influencing consumer inertia toward the digital shift; and saving consumer time.

Source: PYMNTS.com and Atlanta Federal Reserve, GDP Now

After the virus, which is raging in several states that have had to revisit earlier lockdown orders, one of the main headwinds to recovery is unemployment. Data from the U.S. Department of Labor on Thursday showed first-time applications for unemployment insurance last week were higher than projected and remain about double the peak in the previous recession, according to Bloomberg. The unemployment rate as of the end of the week stood at 11.1 percent.

Because the rate dropped from 14.3 percent the previous month, some observers said the economy “appears to be on course for a quick recovery,” Fortune report. However, what remains to be seen are anecdotal factors that will be measured in the next report.

The retail sector is shedding jobs at a furious pace. Other companies have taken a look at their workforce and decided they don’t need as many employees as they did during the pre-pandemic boom times. And an unemployment rate north of 10 percent is still a rickety platform to build a recovery on.

Then there’s the issue of the stimulus. The CARES Act upped jobless benefits by $600 a week, authorized one-time stimulus payments, and made loans to 5 million small businesses to help prop up payrolls. The $600 weekly unemployment subsidy is scheduled to end after July 31. If the stimulus did prop up retail spending, and if the next stimulus bill currently under discussion in Washington fails, the results could sink the current uptick.

“This is a horrendous time to have a lapse in benefits,” Wendy Edelberg, senior fellow at the Brookings Institution, told CNBC. “I expect households are living week to week, financially speaking. I’m far more worried what Congress ends up passing will be a lot less supportive than what was initially in the CARES Act.”

The final elephant in the recovery room comes from gross domestic product (GDP) predictions. The Atlanta Federal Reserve showed a 50 percent to 55 percent contraction for May, which is clearly not square with the retail data. Retail contribution to GDP as of the second week of June took a 45.4 percent hit. This means the Atlanta Fed is seeing something along the lines of these headwinds that makes the retail sales jump seem more like a stimulus-fueled happening.

“The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2020 is -34.5 percent on July 16, up from -35.5 percent on July 9,” the Atlanta Fed report stated. “After recent data releases by the U.S. Bureau of Labor Statistics, the U.S. Department of the Treasury’s Bureau of the Fiscal Service, the Federal Reserve Board of Governors, and the U.S. Census Bureau, the nowcasts of second-quarter real personal consumption expenditures growth and second-quarter real government spending growth increased from -34.0 percent and -9.2 percent, respectively, to -32.5 percent and -8.7 percent, respectively, and the nowcast of second-quarter real gross private domestic investment growth decreased from -53.2 percent to -53.9 percent.”