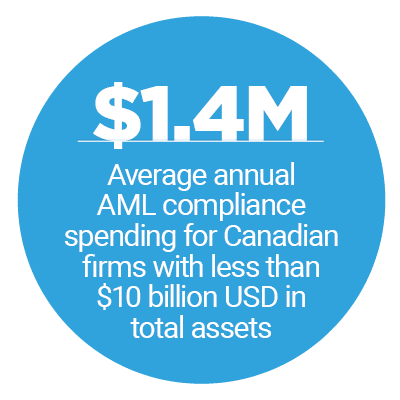

Businesses that fail to comply with anti-money laundering (AML) and know your customer (KYC) regulations risk major regulator fines and irreparable damage to customer relationships when something goes wrong. Companies therefore must either invest in teams of AML specialists or in fraud-fighting technologies.

Not all solutions are easy to adopt, however. Purchasing software can require upfront investments that are beyond the budgets of some smaller firms, while hiring specialist teams could be expensive in the long run, given that employee costs tend to rise more quickly than other budget areas. However, the business costs of not ensuring robust defenses and identity verifications far outweigh these pains.

Not all solutions are easy to adopt, however. Purchasing software can require upfront investments that are beyond the budgets of some smaller firms, while hiring specialist teams could be expensive in the long run, given that employee costs tend to rise more quickly than other budget areas. However, the business costs of not ensuring robust defenses and identity verifications far outweigh these pains.

The “AML/KYC Tracker” examines the latest fraud challenges and efforts to ensure tight security and compliance.

Around the AML/KYC World

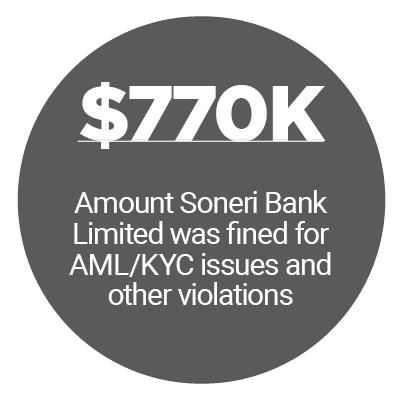

The State Bank of Pakistan (SBP) recently fined four banks for failing to fully comply with KYC obligations and advised several of those financial institutions (FIs) to revise their AML and KYC procedures. Bank Al-Habi, Bank of Punjab, JS Bank Limited and Soneri Bank Limited each paid penalties that ranged from about $180,000 USD to $770,000 USD.

Cannabis delivery platform Eaze Technologies was recently targeted by misconduct allegations as well. A rival company claimed that Eaze had tricked FIs and card companies — which often refuse to get involved with marijuana businesses — into agreeing to process its payments, therefore gaining an unfair advantage over other cannabis companies. The plaintiff — legal marijuana company Herban Industries — asserted in a lawsuit that Eaze directed customer payments through offshore shell companies to disguise marijuana purchases as sales of items such as dog toys. This kind of alleged misbehavior demonstrates why strong know your business (KYB) practices are critical, explained Zac Cohen, general manager of global identification provider Trulioo in a recent PYMNTS interview. Cohen also detailed the difficulties of good KYB practices.

Collaborations can help ease the challenges of compliance for companies seeking to keep their conduct above board. Six Nordic banks are coming together on just such an effort and are working to create standardized KYC processes and a forthcoming platform for collecting and managing customer data. The banks intend to use the platform to provide KYC services to medium-sized and large companies.

Find more on these and all the other latest headlines in the Tracker.

How Mobile Financial Startups Can Bridge the Security Gap

Startups may have great ideas for how to deliver mobile financial services but face challenges in convincing customers to entrust the new entities with their sensitive details. This is especially true given rising rates of mobile fraud attempts that put customers especially on guard.

In this month’s feature story Nicolas Dinh, chief operating officer of a year-old money management and payment app provider STACK explained how startups can keep customers safe and prove their security abilities. Dinh detailed how the work often requires partnering with established payment players and deploying a mixture of key fraud-fighting tools to beat synthetic ID tricks and other types of attacks.

To read the full story, download the Tracker.

To read the full story, download the Tracker.

Deep Dive: How FinTechs, FIs Can Arm Up Against Fraud

AML requirements, anti-terrorist financing rules and other regulations are important tools of governments seeking to stamp down on crime — or at least avoid furnishing it with more financial resources. Governments therefore are increasingly requiring FinTechs to follow similar compliance rules to their FI counterparts.

But compliance with the regulations — however important — can be burdensome to some FinTechs and FIs. Strong AML procedures, for example, require analyzing and detecting meaningful patterns in vast collections of data. This month’s Deep Dive examines the major fraud threats that FIs and FinTechs face, as well as where and how artificial intelligence (AI) software can help ease the strain of AML compliance.

Get the full scoop in the Tracker.

The “AML/KYC Tracker,” a Trulioo collaboration, provides an in-depth examination of current efforts to stop money laundering, fight fraud and improve customer identity authentication in the financial services space.