However, as is the case with any powerful, profitable substance (whether tangible or not), data can be dangerous if not used appropriately. That concern, in fact, serves as one of the main barriers that prevents financial institutions (FIs), payment service providers and other businesses from monetizing their customer data. Those companies that fail in their data-monetization efforts run the risk of falling behind on innovation, and losing customers and revenue.

Those were among the main themes of a recent PYMNTS podcast discussion between Karen Webster and Randy Koch, CEO at ARM Insight, a firm that helps FIs and other organizations to monetize their data. The conversation examined the challenges and opportunities associated with crafting those strategies in the highly regulated payments and financial services space.

Poorly Understood

“Data monetization is a huge opportunity, but is really poorly understood by executives,” Koch said, and that’s “specifically in the payments and financial space.” The problem is fear of data monetization gone wrong (more about that in a bit). However, according to Koch, that fear “far outweighs the real risk.”

That risk is missing out on the potential reward of monetizing data in a pragmatic way that doesn’t run afoul of compliance issues — which, Koch told Webster, comes in the form of a margin that can exceed 85 percent.

Data monetization can be complex (though probably not as complex as most people think, he said), and anything that’s not simple is bound to spark worries and anxieties. That holds especially true as more consumers think about the trade-off of free online services, such as email and the data they give to banks and other businesses. Privacy concerns are growing, and regulations and laws are being enacted or proposed to deal with those political realities. Any company seen as recklessly harvesting, storing, manipulating or selling their consumer data — to saying nothing of suffering a data breach — is promised bad PR.

“If you are a CEO, you don’t want headline news,” he said.

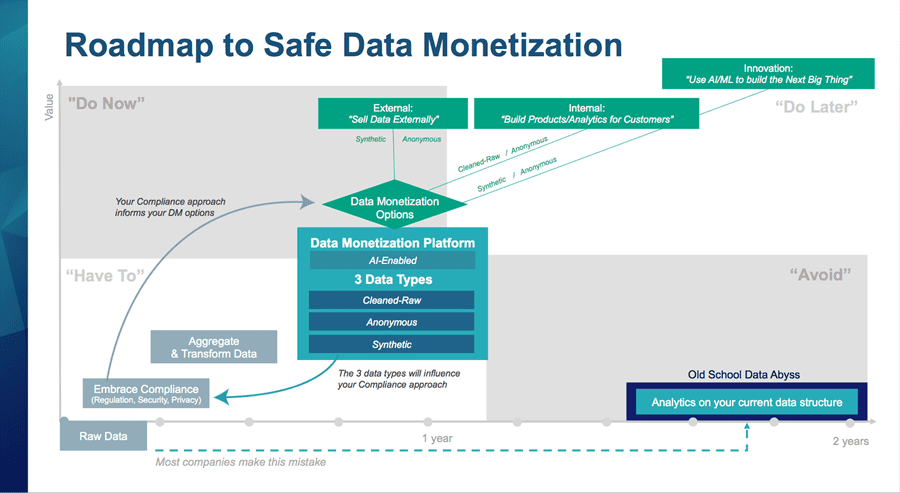

The first step to successful data monetization, Koch explained, is to have a successful data strategy. Early on, that means “embrace the regulations. It doesn’t matter if you like them or you agree with them. You have to embrace them and understand they will change over time.”

Those strategies can run the spectrum. That might be an “external” strategy that simply involves selling data to a third party that does not compete with the FI — say, a fast-food operation that wants to better understand the food-buying habits of younger consumers in the morning. An “internal” data monetization strategy involves “using your own data to create new products or revenue streams with existing customers,” Koch said.

What he called the innovative option employs artificial intelligence (AI) or machine learning “on top of a data set to create truly innovative products. Maybe you want to create the next big AML or fraud prevention product.”

The Three Types Of Data

A data monetization strategy must evaluate those options in the context of the risk and compliance issues inherent in certain data types, which Koch said can be broken down into three buckets:

Raw data contains personally identifiable information (PII), and can, for instance, show where and how a specific person shops at a specific time — and is generally the most valuable type of data, but the one most at risk for theft or misuse.

Anonymous data is the next most-valuable type, and has had PII removed. This type of data is much more general than raw data, and lacks such details as consumers’ specific addresses (anonymous data will have a census block instead, he said) and the accurate, specific time of a purchase (for instance, a cup of coffee bought at a major chain).

Synthetic data — often a starting point for reluctant or nervous executives who are not yet ready to move up the chain to monetize anonymous or raw data — consists of what Koch called “fake data sets that cannot be tracked to the original consumer or FI.” Synthetic data will lack the genders of consumers, and will not offer accurate, specific times of purchases, among other factors.

Yet, it is a way, Koch emphasized, to set the innovative and creative data monetization strategies without fear of data compromise.

Starting Small

In Koch’s experience, most CEOs in the payments and financial services space know “inherently that their data is value, and the risk that comes with it,” but still need help “safely monetizing the data” and conducting the first steps of that process. Many executives tend to start with synthetic data — which, he said, “can be monetized more quickly, even within six months” — before moving on to strategies that involve using higher-risk, higher-reward anonymous and raw data forms.

Doing so, however, typically requires a “conversation” that involves multiple people within the organization — a group that includes compliance experts, the chief data officer, the chief technology officer and other executives. Among the goals of that conversation? To drive home the fact that “data is not the boogeyman if you craft monetization strategies correctly,” Koch said.

Data can be as — or even more — powerful than oil, but there is more to monetizing a lucrative commodity than simply having access to it. In the case of monetization, the data needs to be taken from its silo and “refined,” Koch said, and all those other steps have to be done. However, if the risk can be managed, and the goals set and achieved, he emphasized that the upside of data monetization can indeed be tremendous.